Artificial intelligence (AI) stocks may have been under pressure lately due to concerns about a potential bubble, but there is no denying that this technology is gaining widespread adoption across various sectors.

From robots in factories to automated ad campaigns to supply chain management to healthcare, AI is touching several industries in a positive way. That's why big tech giants, neocloud companies, and AI specialists such as OpenAI have been spending big on developing infrastructure to meet the growing demand for AI applications.

Foundry giant Taiwan Semiconductor Manufacturing (TSM +0.22%), popularly known as TSMC, gives investors a sure way to capitalize on the proliferation of AI. Let's look at the reasons why this may be the only AI stock you may need to buy for 2026.

Image source: TSMC.

TSMC is set to keep winning from AI infrastructure spending

Investment bank UBS expects global capital spending on AI infrastructure to hit $571 billion in 2026, up from its earlier prediction of $500 billion. That would be a 34% jump from this year's AI capital expenditure (capex). A good chunk of this money is set to go toward semiconductors. McKinsey points out that 60% of AI capex is usually allocated to "technology developers and designers, which produce chips and computing hardware for data centers."

NYSE: TSM

Key Data Points

TSMC is the go-to manufacturer of the chips and computing hardware that go into AI data centers by virtue of being the world's largest semiconductor foundry. Market research firm Counterpoint Research points out that TSMC's share of the global foundry market stood at an impressive 71% at the end of the second quarter of 2025. That's an increase of 6 percentage points from the year-ago period.

More importantly, TSMC dominates this market, as second-place Samsung has a share of just 8%. TSMC's leading position in the foundry market can be attributed to its outstanding customer base, all of which are using the Taiwan-based company's fabrication plants to get their AI chips manufactured.

TSMC's 3-nanometer (nm) and 5nm fabrication facilities are fully sold out for 2026, driven by demand from the likes of Apple, Nvidia, Qualcomm, and MediaTek. TSMC's use rate -- a measure of production capacity -- is expected to hit 100% in the first half of 2026. That's likely to result in price hikes, since the company's dominant position in this market gives it solid pricing power.

Reports indicate that TSMC could increase the price of its 3nm and 5nm chips by 5% to 10% next year. Additionally, the company is expected to charge an additional 15% to 20% for its advanced packing services, which are used for manufacturing AI chips. This should allow TSMC to report a potential bump in its earnings growth next year.

This foundry giant could make investors significantly richer in 2026

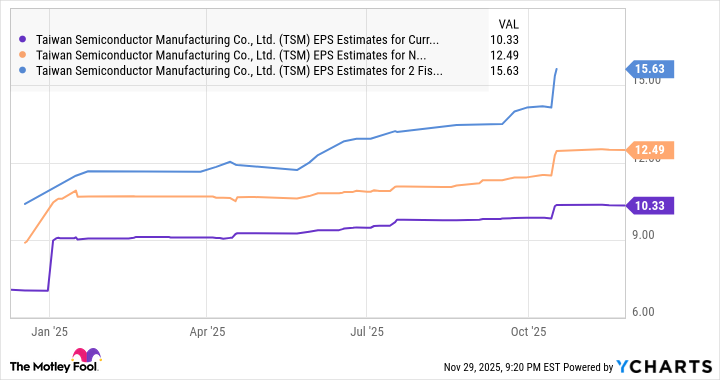

Analysts are expecting TSMC to show 47% earnings growth in 2025 to $10.33 per share. However, they expect a slowdown in 2026, believing it could deliver only 21% growth.

TSM EPS Estimates for Current Fiscal Year data by YCharts

Of course, they are expecting its growth to accelerate in 2027, but the points discussed above indicate that TSMC could end up with much faster growth next year. Assuming TSMC manages to register even a 40% growth in earnings next year, its bottom line could hit $14.46 per share in 2026. Multiplying that by the tech-laden Nasdaq-100 index's earnings multiple of 33.4 points toward a stock price of $483 after a year.

That implies potential gains of 65% from current levels. With TSMC trading at 30 times earnings, a discount to the Nasdaq-100, it looks like a no-brainer buy considering the important role it plays in the AI chip market, which is poised for another year of terrific growth in 2026.