As 2025 draws to a close, the S&P 500 is on pace to notch a double-digit gain for the third consecutive year. Even so, savvy investors recognize that macroeconomic indicators suggest a sharp correction could be in store for 2026.

Unemployment in the U.S. is 4.6%, its highest level since September 2021. Meanwhile, as artificial intelligence (AI) continues to be the biggest contributor to the ongoing bull market, some investors are beginning to fear that a bubble is forming.

Given the broader economic uncertainty, investors may be wondering how they can make the most of their cash right now. Below, I'll explain why business development companies (BDCs) could be a savvy play for dividend investors, and reveal one ultra-high-yield opportunity in the BDC landscape that I like.

Are BDCs a good investment right now?

When start-ups are seeking to raise funds for the first time, they often turn to venture capital (VC) firms. In exchange for their capital, VC investors receive equity (ownership) in their new portfolio company. Over time, founders are inclined to turn to other sources of capital beyond VC money in an effort to minimize further dilution.

This is where BDCs come in. Broadly speaking, BDCs make loans to small and mid-sized businesses that are looking to complement the equity (cash) they've raised with some debt on the balance sheet. BDCs are structured in a way that requires them to pay out 90% of taxable income to shareholders. This is one reason that dividend investors prefer to hold onto BDCs.

Given the Fed's tightening monetary policy -- with the potential for future interest rate reductions on the horizon -- BDCs may not appear to be a wise investment choice right now. The reason I say that is that if interest rates continue falling, the spreads BDCs earn on their loans will shrink. This could lead to smaller profits and potentially stalled dividend payments.

While this makes sense in theory, the reality is much more nuanced. According to a recent report from Houlihan Lokey, the BDC market was sluggish during the first half of 2025, largely due to uncertainty surrounding President Donald Trump's tariffs and the geopolitical tensions in Europe and the Middle East.

However, deal flow has begun to accelerate over the last several months. In particular, technology and software businesses have become attractive opportunities for BDCs as these companies raise debt financing following an unprecedented surge in capital inflows for AI and infrastructure opportunities.

According to Houlihan's data, net interest spreads are indeed tightening. The caveat is that this is due to increased competition, rather than Fed-related activity. In my eyes, tightening spreads could be offset by higher origination volume -- which appears to be the case right now.

Taking this one step further, another mitigant to compressing spreads is that some companies may choose to prepay their loans as IPO and M&A activity rebounds in an AI-driven market. The key here is to identify which BDCs are particularly exposed to the ongoing AI and infrastructure supercycle.

Image source: Getty Images.

Why Hercules Capital stands out from the pack

When it comes to BDCs focused on the technology sector, Hercules Capital (HTGC 0.32%) is my top pick. Hercules currently boasts a dividend yield of 10.2%.

NYSE: HTGC

Key Data Points

The majority of Hercules' portfolio focuses on technology and life sciences businesses. As AI infrastructure spending continues to accelerate, borrowers are going to need access to more working capital and acquisition financing.

In a way, Hercules could be seen as a pick-and-shovel financier to the companies hoping to disrupt big tech's influence on the AI landscape. Some of Hercules' more notable transactions over the last year include backing AI and cybersecurity start-ups such as Harness, Shield AI, Semperis, Chainalysis, and Armis -- the latter of which was recently acquired by ServiceNow for $7.7 billion in cash.

Overall, only 1.2% of Hercules' portfolio is placed on non-accrual status, meaning that principal and interest or other fees will likely not be collected in full. With such a strong portfolio performance, it's not a surprise that Hercules' current net interest income of $0.49 per share provides over 120% coverage of its base distribution.

The bottom line: Hercules has proven long-term resilience

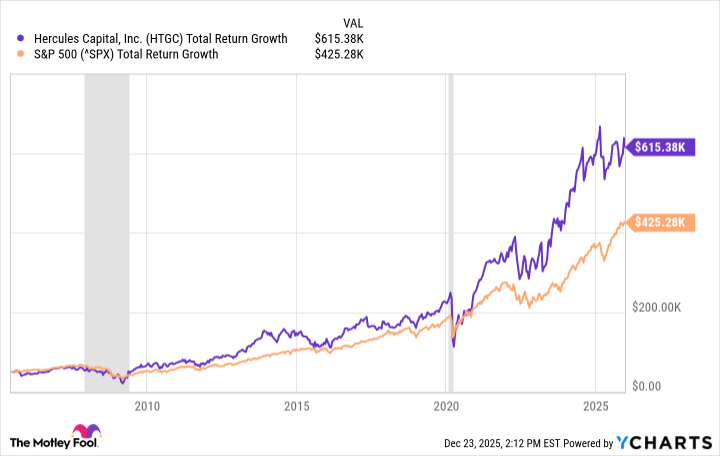

The chart below depicts the growth of a $50,000 investment in Hercules compared to the S&P 500 over the past 20 years. Even during times of economic slowdown -- recessions are illustrated by the gray bars -- Hercules has proven to be a resilient stock.

HTGC Total Return Level data by YCharts.

Moreover, an investment in Hercules has generated a total return that's nearly 45% higher compared to the broader market over the last two decades.

To me, despite intense competitive dynamics and some degree of uncertainty permeating throughout the macro environment, Hercules represents a safe and secure dividend stock for investors with a long-term horizon. Against this backdrop, I see Hercules stock as a no-brainer right now, and as a great way to earn passive income in the new year and beyond.