Need some new growth names for your portfolio? Fintech isn't exactly a new concept anymore. But the steady convergence of technology and money continues to create tremendous potential.

With that as the backdrop, here are three of the very best investment opportunities within the fintech sector right now.

SoFi Technologies

You're probably familiar with the premise of online banking. In fact, anyone reading this likely does a fair amount of online banking. What you may not realize is just how in love Americans are with banking online.

A recently completed survey by the American Bankers Association puts things in perspective. As of October, 54% of U.S. bank customers primarily use a mobile banking app to manage their accounts, while another 22% prefer using a conventional computer. At the other end of the spectrum, only 9% of a bank's customers step into a branch for service, and phone calls are the choice of only 4%. Unsurprisingly, younger customers are more likely to manage their bank accounts online. As these people age, of course, the crowd becomes even more comfortable with this option.

Most banks offer some sort of digital banking service, though none of them seem to do it quite as well as SoFi Technologies (SOFI 1.73%), which was built to be an online-only bank. And since early 2019 -- when it was still mostly a student-loan refinancing service -- its customer count has grown every single quarter, from 704,000 then to more than 12.6 million now.

Image source: Getty Images.

That's impressive, to be sure, yet it still doesn't scratch the surface of SoFi's potential. It's only a fraction of the U.S.'s increasingly digitally native 260 million adults, and most of SoFi's existing customers have less than two kinds of accounts or products with the online bank.

PayPal

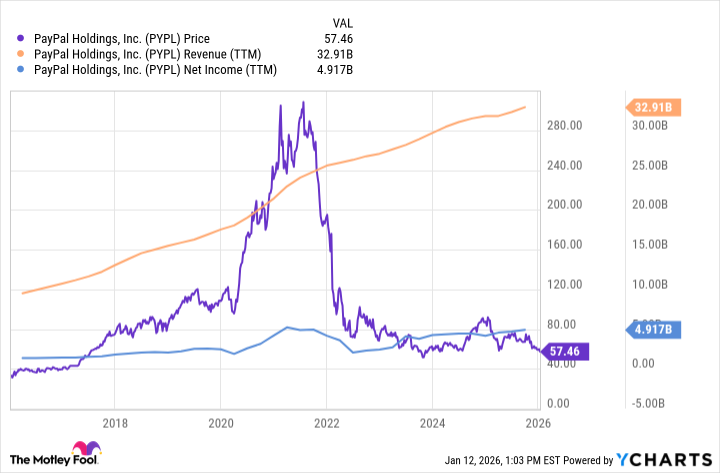

It's been an interesting and even somewhat confusing past few years for PayPal (PYPL +1.90%) and its shareholders.

Based on nothing more than the stock's poor performance since its 2021 peak, it would be easy to presume the popular online-payment service never bounced back from the wind-down of the COVID-19 pandemic (which of course was a boon for its business). That's just not the case, however. PayPal is on pace for another year of record-breaking revenue at $33.3 billion. Moreover, it's close to matching its previous profit peak, which it reached in 2021, in fiscal 2025.

What gives? The market appears to keep pricing in bad news that never actually materializes. Whether that's the advent of cryptocurrency as an alternative to fiat currency payments, stepped-up competition from banks and credit card outfits, or the continued growth of direct rivals like Block, Zelle, or Stripe, the crowd is clearly afraid of something that's yet to happen. PayPal's share of the global online payment business is just as strong as it's ever been, at just a little under half.

The thing is, if it hasn't happened yet, it's not apt to happen in a big way now. The analyst community says the company is en route to a string of new record-breaking years all the way through 2028, when it's forecast to turn $41 billion in revenue into $5.8 billion of net income. The investing crowd should certainly be able to see, accept, and price in this growth sooner than later.

And the potential upside for the stock once that ball gets rolling is enormous. The shares are currently valued at less than 10 times this year's projected per-share profit of $5.79 and 24% below analysts' average price target of $73.94.

Upstart

Finally, add Upstart (UPST 1.38%) to your list of top fintech stocks to buy right now.

It's not exactly a household name. There's a good chance, however, you've benefited from its service.

Upstart is a new kind of credit scoring business, using an artificial intelligence algorithm to determine a would-be borrower's creditworthiness. Whereas longer-established players like Equifax and TransUnion do a reasonably good job with the technological tools at their disposal, Upstart is the sort of solution you'd create if you were building a new credit rater from scratch -- which is exactly what former Google executive Dave Girouard, computer scientist Paul Gu, and finance-trained entrepreneur Anna Counselman did back in 2012. The end result is a platform that allows for 43% more loan approvals with no additional defaults. More than 90% of its approvals are fully automated, too, making it a cost-effective option for everyone involved in the lending process. That's why more than 100 banks, credit unions, and other lenders are regular users of its service.

Now, the stock's taken shareholders on a rather wild ride since its 2020 public offering, soaring during the pandemic before tumbling in 2022, where it's been hot and cold ever since. But that means the platform is working as designed. About the middle of last year the algorithm "sensed" economic headwinds were starting to blow, for instance, leading to fewer loan approvals than anticipated, which dragged the stock lower.

NASDAQ: UPST

Key Data Points

This is how the platform is supposed to work: by protecting lenders in times of uncertainty.

The stock's 2025 struggle also doesn't appear to reflect the fact that through the first three quarters of last year, the total number of loans that Upstart processed more than doubled, while total loan conversions have improved from 15.3% a year ago to 21.2% now. Look for more of this sort of growth, too. Then look for the market to start pricing in the fact that Upstart's business is at a turning point.