ASML Holding (ASML +2.15%) stock has been on a red-hot run on the market over the past year, rising an impressive 75% as compared to the 47% gains clocked by the PHLX Semiconductor Sector index during this period.

The good news is that ASML is likely to sustain its momentum going forward as well. After all, the Dutch semiconductor bellwether plays a critical role in the global chip industry with its extreme ultraviolet (EUV) lithography machines, which help its customers manufacture advanced chips capable of delivering strong computing performance with high power efficiency.

The chips manufactured with ASML's machines are now in high demand, primarily driven by their use in artificial intelligence (AI) applications. Importantly, that demand is here to stay, according to investment bank Morgan Stanley, potentially paving the way for more upside in ASML stock.

Let's see why Morgan Stanley believes that ASML's stock market rally is likely to continue.

Image source: ASML.

Strong chip demand should boost ASML's equipment orders

Morgan Stanley points out that the increase in semiconductor manufacturing capacity by chipmakers and foundries to meet the booming demand for AI chips could send ASML stock up by 70%. The investment bank's bull case is driven by continued investment in foundry and memory manufacturing capacity, markets where demand exceeds supply.

NASDAQ: ASML

Key Data Points

Analysts at Morgan Stanley predict that ASML's earnings per share could nearly double by 2027 as compared to last year. It is easy to see why the investment bank is so upbeat about ASML's prospects. After all, semiconductor foundry giant Taiwan Semiconductor Manufacturing (TSM +0.44%) has just announced that it will be ramping up its capital spending by 32% in 2026 to $54 billion based on the midpoint of its guidance range.

The Taiwan-based giant is going to allocate 70% to 80% of its 2026 capital expenditure (capex) this year toward shoring up the production of chips based on advanced process nodes, which are chips that are 7-nanometer (nm) or lower in size. ASML is the only company that manufactures the EUV machines capable of producing such advanced chips

Similarly, there is a severe shortage of memory chips, driven by healthy demand for high-bandwidth memory (HBM) used in AI data center accelerators. This is compelling memory manufacturers like Micron Technology to build more facilities. Micron is planning to spend $20 billion in capex in the current fiscal year, a 45% increase over last year.

Morgan Stanley points out that the ramp-up in spending by the likes of Micron, TSMC, and others will play a central role in driving demand for ASML's equipment. It is worth noting that the industry association SEMI is projecting a robust 69% increase in advanced chipmaking capacity through 2028. Producing these advanced chips could substantially boost demand for ASML's EUV machines, which is why there is a good chance the company will indeed hit Morgan Stanley's earnings forecast.

Why Morgan Stanley's 70% upside estimate can turn into reality

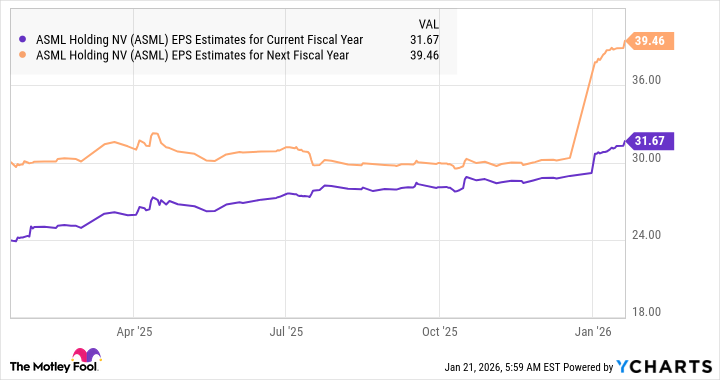

According to consensus estimates, ASML finished 2025 with an estimated 24.78 euros per share in earnings, which translates into $29.01 per share at the current exchange rate. Analysts are anticipating a smaller jump in ASML's earnings this year following last year's 29% increase. However, its bottom-line growth is anticipated to accelerate in 2027, as evident from the following chart.

ASML EPS Estimates for Current Fiscal Year data by YCharts.

The earnings figures in the chart above are in U.S. dollar terms. However, Morgan Stanley's estimate of 46 euros per share in earnings in 2027 suggests that ASML's bottom line could be much higher than consensus expectations next year. The investment bank's forecast suggests that ASML's 2027 earnings could be $53.85 per share (using the current exchange rate).

If the stock is trading in line with the U.S. technology sector's average earnings multiple of 44.7 at that time, its stock price could hit $2,407. That's a potential jump of 81% from current levels, indicating that ASML remains a top semiconductor stock to buy as it has the potential to deliver substantial upside even after the impressive gains it has clocked in the past year.