It didn't take long for the stock market to heat up in 2026. Barely one month into the year, several major events, particularly on the geopolitical front, have already whipsawed markets.

However, amid the excitement, another dynamic has been playing out: rotation. Over the past six months or so, investors have really begun to question artificial intelligence stocks, like those in the "Magnificent Seven," due to concerns about valuation, significant investment in AI-related infrastructure, and whether AI technology has reached the point of diminishing returns.

Meanwhile, investors have been pounding the table on a historically boring sector that has underperformed the broader market for nearly two decades.

NYSEMKT: KRE

Key Data Points

Is this sector finally about to rebound?

If you have long invested in bank stocks and had to endure years of underperformance, isn't this a sight for sore eyes?

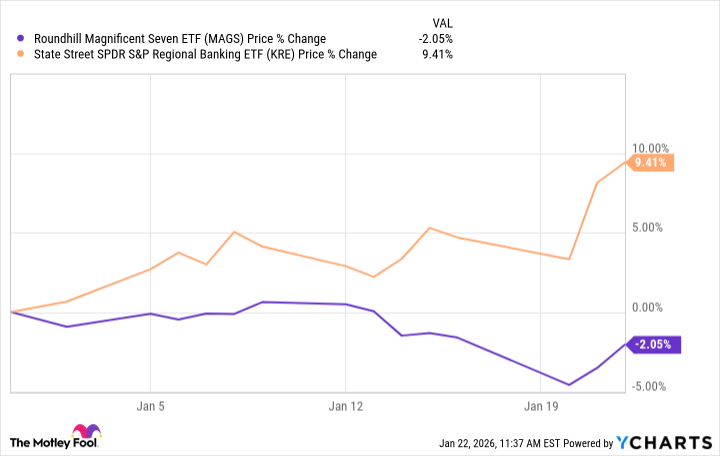

The banking sector, as seen through the State Street SPDR S&P Regional Banking ETF (KRE 3.32%), has gotten off to a phenomenal start to the year and is well ahead of the Roundhill Magnificent Seven ETF (MAGS +1.06%) as investors funnel out of AI and into banks and small-cap stocks.

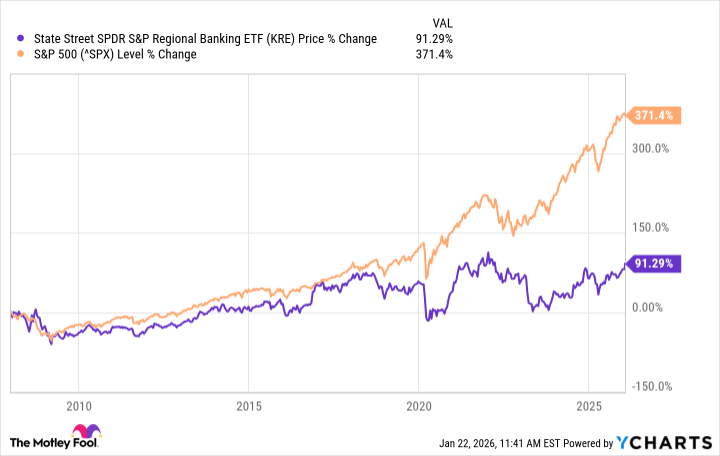

Banks have underperformed widely since the Great Recession, an event they seemingly couldn't escape from a reputational perspective. Other scandals over the years, such as Wells Fargo's phony accounts scandal and the Silicon Valley banking crisis, have also rocked the sector. Even with this recent rally, the broader market has still widely outperformed bank stocks since the Great Recession.

But the banking sector seems to have real momentum right now. Banks are no longer a major political issue; in fact, they seem far from the limelight these days. President Donald Trump's administration has not only opened the door to a massive wave of mergers and acquisitions but could also impose lower regulatory capital requirements, which would promote more lending and capital distributions to shareholders.

Other dynamics may also be at play. While the Federal Reserve has lowered interest rates, longer-term bond yields have not fallen as much, steepening the yield curve. A steep yield curve occurs when yields on longer-dated bonds are higher than those of shorter-duration bonds.

The bond market is still concerned about inflation, and there also seems to be some belief that the administration will try to run the economy hot by aiming for a higher rate of gross domestic product than inflation to dig out of the mountain of debt the U.S. government now bears. In this scenario, bond yields may remain higher for longer, likely resulting in a steeper yield curve.

This is typically when generalists really come in and buy the sector because banks traditionally borrow money at the short end of the yield curve and lend it out at the long end.

Will the rotation continue?

It's always difficult to predict the future, especially in the near-term, less than a year out. But I don't see any reason this trend can't continue, given some of the tailwinds mentioned above. There also haven't been any material signs of stress in bank credit, and in general, the sector is now much less leveraged and in much better shape than during the Great Recession. Banks may also further improve their operations through automation and AI.

Obviously, the sudden emergence of a recession could change things. Market conditions can also change rapidly, and AI may quickly find its mojo again, reverting attention to the sector.

For investors interested in the bank sector, I would look less at some of the larger bank stocks right now, which have made big gains and trade at some pretty high valuations. They can go higher under the right scenarios, but I think there are better opportunities in the small- to mid-cap space, where consolidation is likely to continue, and where many names have simply been forgotten.