Advanced Micro Devices (AMD -1.21%) posted strong revenue growth to close out 2025 and issued solid 2026 guidance, but the stock fell as investors were expecting more after the stock had doubled over the past year heading into the fourth-quarter report's release. Meanwhile, investors decided not to give the company credit for an unexpected boost in China revenue that it saw in Q4, which may not repeat.

China provides upside

Sales of $390 million worth of graphics processing units (GPUs) to China helped boost AMD's Q4 results. However, the company didn't forecast further sales to the country, outside of $100 million in revenue in Q1, with management calling the situation "dynamic."

Image source: Getty Images.

This helped AMD's data center revenue climb 39% year over year in the quarter to $5.4 billion. Growth was led by both record central processing units (CPUs) sales and accelerating GPU deployments. It said that eight of the 10 largest artificial intelligence (AI) companies are now using its GPUs for their AI workloads.

Client and gaming segment, revenue, meanwhile, jumped 37% to $3.9 billion. Within the segment, client revenue rose 34% to $3.1 billion as it continues to take market share in the PC space, while gaming revenue surged 50% to $843 million. However, the company does expect the semi-custom revenue that helped power its 2025 gaming segment results to fall meaningfully in 2026. AMD's smaller embedded segment, meanwhile, saw revenue edge up 3% to $950 million. The company expects the segment to grow in 2026.

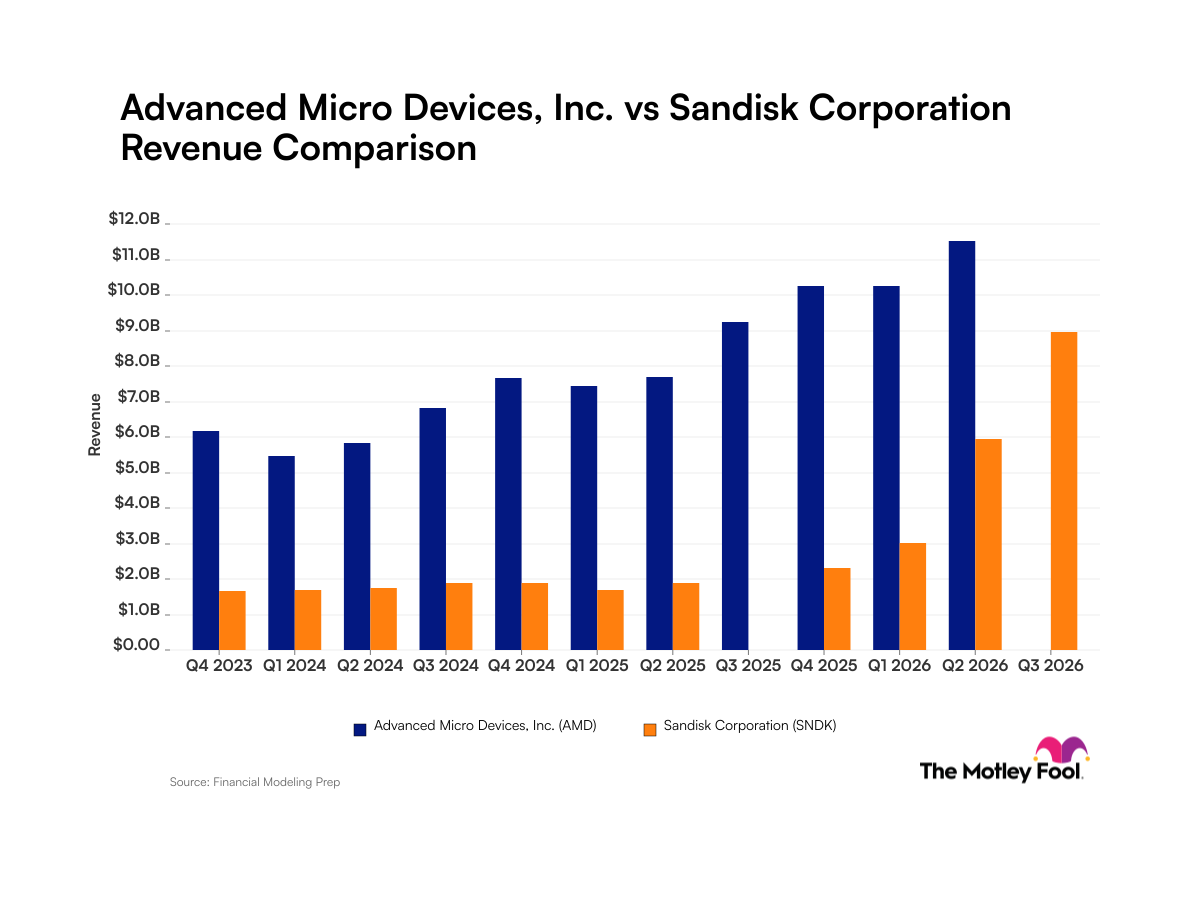

Overall, AMD's Q4 revenue climbed by 34% year over year to $10.27 billion. Gross margin came in at 54%, up 300 basis points from a year ago, helped by the reversal of a write-down on its MI308 chips for China. Adjusted earnings per share rose 40% to $1.53, ahead of the $1.32 consensus.

Looking ahead, AMD guided for Q1 revenue to grow by 32% year over year to $9.8 billion, plus or minus $300 million.

NASDAQ: AMD

Key Data Points

Should investors buy the dip?

While AMD was a victim of high expectations, the company still performed well and appears on track for a strong 2026, especially with it expected to start delivering GPUs to OpenAI in the second half of the year. Meanwhile, it remains the dominant data center CPU provider.

Looking at valuation, AMD stock trades at a forward price-to-earnings (P/E) ratio of 32 times 2026 analyst estimates, but it has a forward price/earnings-to-growth (PEG) ratio of only 0.2 (with under 1 times being considered undervalued). That makes this a stock worth grabbing on this price dip, given its solid long-term outlook as AI infrastructure spending continues to ramp up.