Spending on artificial intelligence (AI) infrastructure is poised to remain robust in the coming years, with McKinsey estimating a whopping $7 trillion will be spent on data centers by 2030 to build enough computing power to support workloads in the cloud.

There are several ways you can take advantage of the massive AI infrastructure opportunity during this decade. From Nvidia to Broadcom to Micron Technology, investors are spoilt for choice to capitalize on booming AI spending on data centers. However, now is a good time to take a closer look at Advanced Micro Devices (AMD 3.46%), an emerging force in the AI chip market that seems like a terrific buy this month.

Image source: AMD

AMD's latest pullback is a buying opportunity

AMD released its fourth-quarter 2025 results on Feb. 3. Surprisingly, AMD stock fell a whopping 17% the following day despite the company's better-than-expected results and guidance.

NASDAQ: AMD

Key Data Points

This seems like a great opportunity for investors to buy AMD stock on the cheap to take advantage of the massive AI infrastructure opportunity. After all, AMD is forecasting a 32% year-over-year increase in revenue in the current quarter, along with a non-GAAP (generally accepted accounting principles) gross margin of 55%, an increase of one point from the prior year.

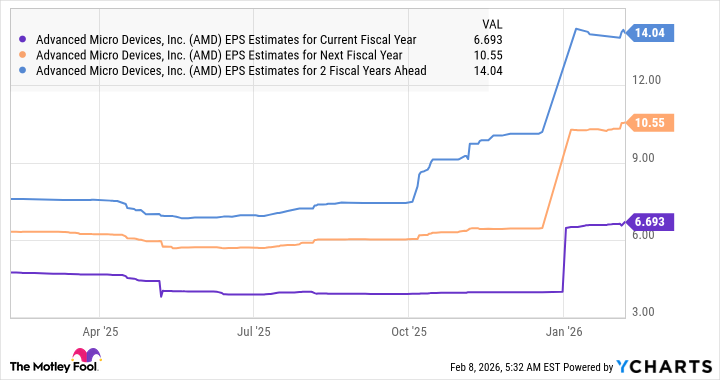

The chip designer's adjusted earnings increased by 26% in 2025 to $4.17 per share. So, the Q1 guidance indicates that it is on track to clock a bigger earnings jump in 2026, driven by healthy growth in revenue and an uptick in the margin. Not surprisingly, analysts are bullish regarding AMD's earnings growth for the next three years.

AMD EPS Estimates for Current Fiscal Year data by YCharts

Importantly, the company can sustain this terrific momentum beyond 2028. That's because it stands to gain from AI adoption on multiple fronts -- data centers, personal computers (PCs), and embedded processors deployed in networking, storage, industrial, automotive, and other applications. What's more, AMD designs not just graphics cards but also central processing units (CPUs) that go into these applications.

AMD sees its data center addressable opportunity growing from $200 billion last year to a whopping $1 trillion in 2030. As a result, the company anticipates its revenue to grow at an annual rate of more than 35% through 2030, while earnings per share could jump to more than $20 during this time frame.

The stock could be a multibagger by the end of the decade

AMD is trading at just over $200 per share following its latest slide. It trades at a price/earnings-to-growth ratio (PEG ratio) of 0.65, according to Yahoo! Finance, which means it's undervalued with respect to the annual earnings growth it can deliver over the next five years.

We have already seen that analysts are expecting impressive growth in AMD's bottom line through 2028. Even if it clocks a slower earnings growth rate of 20% in 2029 and 2030, its bottom line could indeed hit $20 per share by the end of the decade (in line with the company's expectations).

Multiplying the projected earnings in 2030 by the tech-laden Nasdaq-100 index's forward earnings multiple of 26 suggests this semiconductor stock could jump past $500. So, AMD stock can become a multibagger, which is why investors should consider buying it following its steep decline.