Shares of Lucid Group (LCID +1.54%) have plunged 61% over the past six months, leaving many investors wondering whether now is a good time to buy the electric vehicle (EV) stock, hold on and wait for better days, or cut their losses and sell.

I don't think there's a strong case for buying Lucid right now. And while there are some signs of life from the company, I think the case for holding on to your shares depends on whether the automaker improves key financial metrics over the next year.

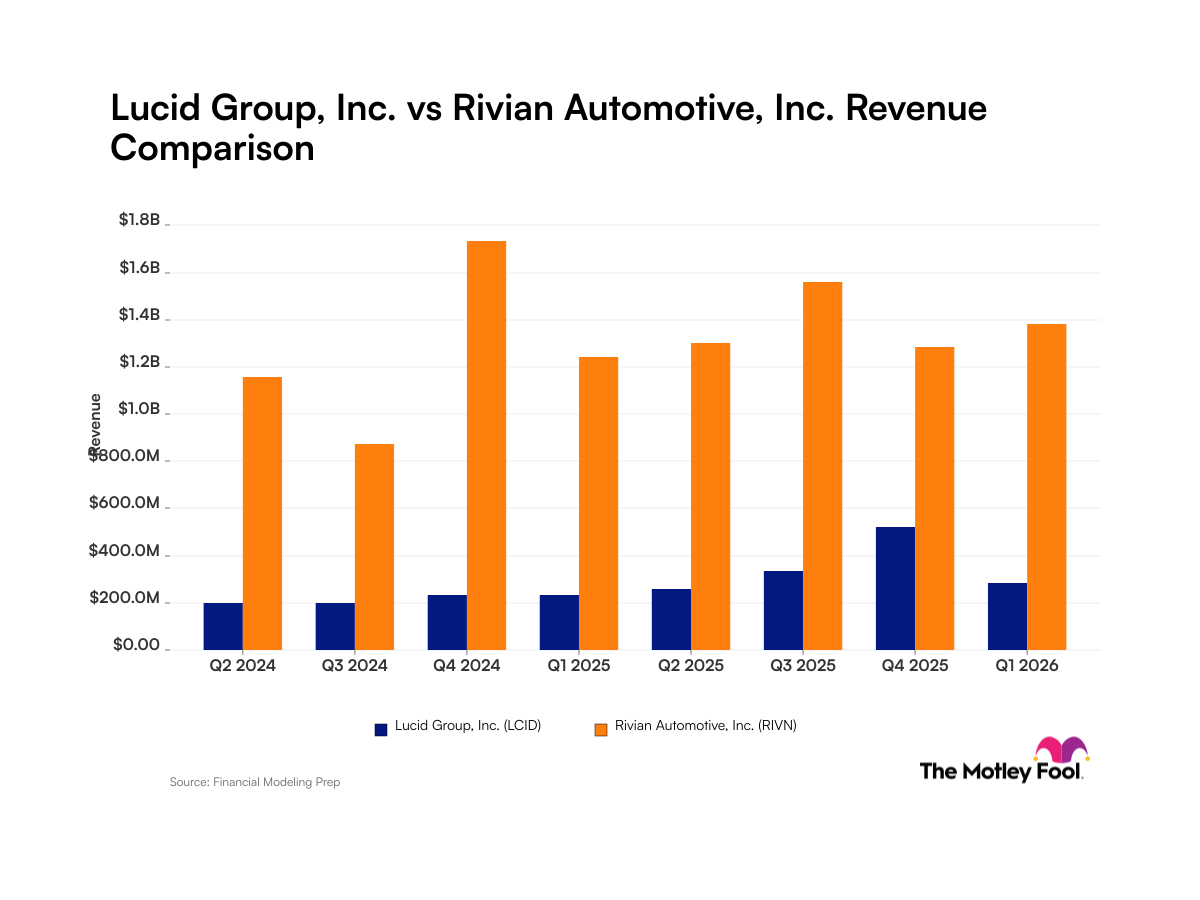

Image source: Lucid.

Lucid shows signs of life

The EV company has made some progress lately, producing 7,874 vehicles in its fourth quarter (ended Dec. 31) -- a 132% increase from the year-ago quarter. Vehicle production growth for all of 2025 was impressive, too, nearly doubling to 17,840. Surging production propelled revenue up 123% to $523 million in the fourth quarter.

And then there's Lucid's delivery figure. It's one thing to manufacture more vehicles and quite another to sell them and get them to customers. The automaker increased its deliveries by 72% in the fourth quarter to 5,345. Although that is still a very small number, the increase clearly shows it is making improvements.

But the company is falling short on important metrics

Unfortunately, the company's recent improvements are still overshadowed by its significant -- and mounting -- losses and a broader slowdown in EV demand.

The fourth-quarter operating loss of nearly $1.1 billion was disappointing and contributed to a total operating loss of $3.5 billion in 2025. Building an EV company is capital intensive, and Lucid expanded its vehicle lineup last year with its Gravity SUV and will soon add two new, midsize vehicles, both of which require lots of capital.

The midsize Cosmos and Earth will be built on the company's new platform and have a starting price of less than $50,000 -- significantly less than its other vehicles -- and production is expected to start late this year. The goal for the Earth is to attract more customers at a lower price point and increase production efficiency by sharing parts across multiple vehicle models.

NASDAQ: LCID

Key Data Points

But the cars will be launched at a particularly difficult time in the EV market, with many potential customers opting for cheaper gasoline-powered vehicles. EV sales declined by 2% in the U.S. last year and could be on even shakier ground this year, as the chances of a recession have increased and consumers worry about inflation.

The verdict: Time is running out to hold Lucid

If I owned shares of Lucid, I would probably hold them a little longer if I didn't need the money invested elsewhere -- not for much longer, however. I'm a long-term optimist about the EV market, but I think the transition will take many years longer than initially expected.

The EV maker is not out of the woods, and its success is nowhere near guaranteed. I believe the next year will be very important for the company as it tries to prove it can continue to expand production for new models and reduce its losses.

I wouldn't buy Lucid now, and I think it has a tough road ahead. If you have a small position now, holding on to it for a little longer could make sense. But cutting your losses at this point wouldn't be an unwise move, either.