Since its debut on the public markets in 2021, Lucid (LCID 1.63%) has emerged as one of the most popular electric vehicle (EV) manufacturers. That popularity has earned its stock a prominent place on the radars of EV and growth investors alike.

The primary reason Lucid stock has drawn such considerable attention is because of the similarity investors recognize between it and another well-known EV company, Tesla (TSLA 15.31%). Like Tesla, after Lucid's stock became available to the public, the company revealed its plan to hit the road with a luxury model and then expand its product line to include more affordable models.

Stock

In a 2021 investor presentation, for example, the company articulated its vision: "Lucid plans to start with high end cars, build the brand synonymous with luxury, and then manufacture progressively more affordable vehicles in higher volumes."

While the road it has traveled over the past few years has had some bumps, Lucid has recorded several accomplishments that suggest to investors that the company is well positioned to benefit from the growing enthusiasm for EVs.

For one, Lucid has garnered considerable critical acclaim, winning steady praise and awards that include:

- MotorTrend 2022 Car of the Year

- U.S. News & World Report's 2023 Best Luxury Electric Car

- A spot on the Car and Driver 10 Best List for 2024

Investors are keenly attuned to news such as this. After all, if Lucid is racking up accolades from critics, it's reasonable to infer that it will electrify consumers' enthusiasm.

Lucid opened the first auto manufacturing plant in 2023 in Saudi Arabia, where the company plans to expand the facility to achieve an annual production capacity of more than 150,000 vehicles. Lucid aims to produce its midsize vehicle at the Saudi Arabia facility in 2026.

How to buy

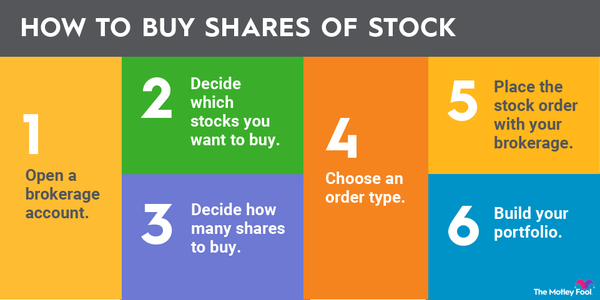

How to buy Lucid stock

The company trades on the Nasdaq exchange under the stock ticker LCID. Whether you're an experienced investor who has logged many miles of experience or buying shares of Lucid would be the first time you park a stock in your portfolio, you'll need to make some simple moves to count yourself as a Lucid shareholder.

Step 1: Open a brokerage account

The prospect of owning Lucid stock may rev your engine, but first things first: You must have a brokerage account. There are many options, but inexperienced investors may want to consider Fidelity, which offers $0 commission for online stock trades.

Step 2: Figure out your budget

Buying stock is a great step toward building personal wealth; however, it shouldn't come at the cost of imperiling your financial well-being. Review your finances and determine how much money you can comfortably invest while still covering your monthly expenses and contributing to savings.

Step 3: Do your research

After you identify a potential stock pick -- Lucid or something different -- it's critical to start digging in deeper and learning more about the company. Once you assess the company's strengths, weaknesses, opportunities, and threats (SWOT), you'll certainly want to consider the stock's valuation.

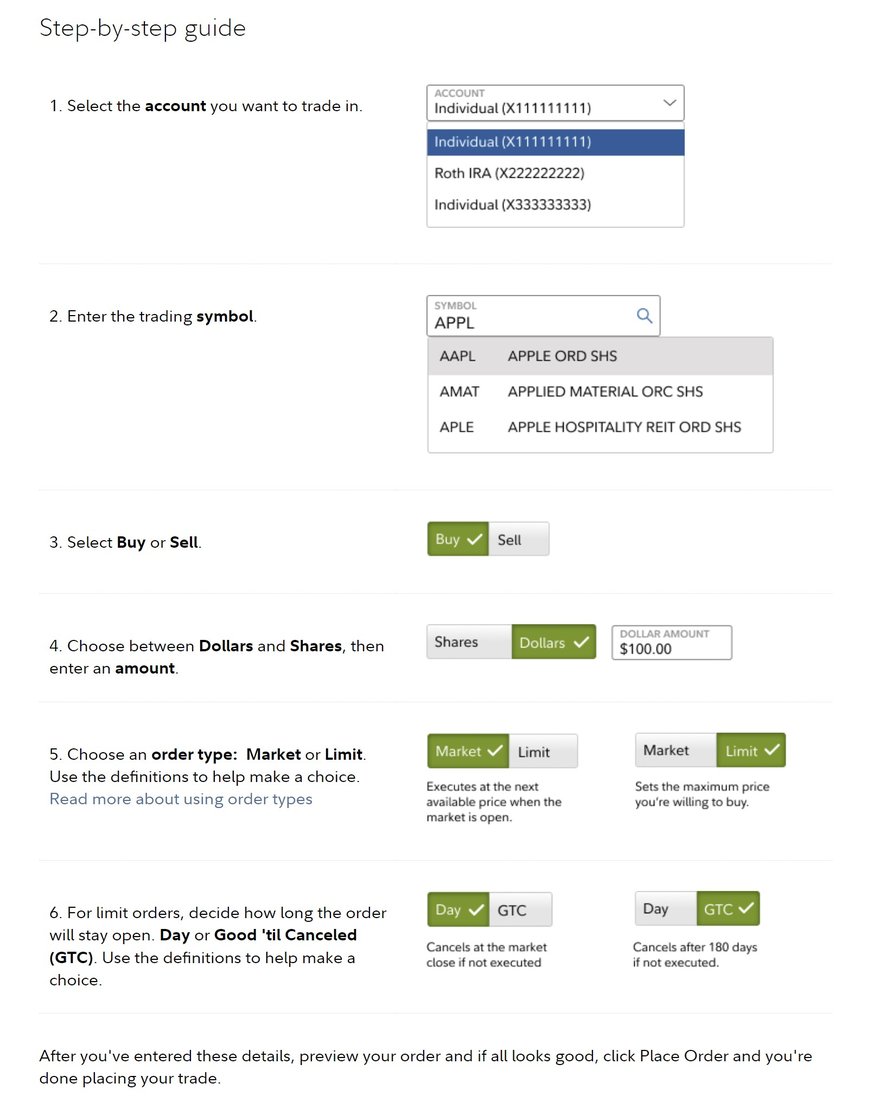

Step 4: Place an order

Having completed your research, it's time to join the ranks of Lucid shareholders. Once you enter the stock's ticker (LCID for Lucid) and choose to buy the stock (instead of sell), you must decide whether you want to place a market order or a limit order. Next, you'll have to determine the size of your purchase -- whether you will buy a fractional share, a single share, or hundreds of shares.

Should I invest?

Should I invest in Lucid?

Surely, EV investors have likely come across Lucid's name at some point over the past few years -- even if they haven't seen the company's vehicles on any highways or byways. Whether it's a smart idea to hitch a ride with this EV upstart, however, is a different story.

First and foremost, people who are averse to volatility will want to avoid Lucid. From the time of its merger with special purpose acquisition company (SPAC) Churchill Capital Corp IV in 2021 to early 2024, shares of Lucid have traded as high as $58 and as low as about $2.50. Bulls are optimistic that the stock can recapture its former glory, but there's certainly no guarantee that it will, let alone whether it will remain that high instead of promptly plunging again.

Similarly, those with a lower tolerance for risk will want to avoid parking Lucid in their portfolios. Although Lucid has earned critical acclaim, there's no certainty that the enthusiasm will translate to investors on a large enough scale that it enables the company to sustain operations.

For those comfortable with a more speculative investment, Lucid may be a growth stock that's a good fit. Bulls are keen on the company's plan to expand its product line beyond its flagship offering. In addition to starting production of the Lucid Gravity, a luxury SUV, in late 2024, the company expects to start production of its midsize vehicle in 2026.

Profitability

Is Lucid profitable?

With two full years of operations under its belt as a publicly traded company, Lucid has failed to generate any semblance of a profit. In 2023, for example, Lucid posted a gross loss of $1.34 billion, steeper than the gross loss of $1.04 billion it reported in 2022.

Management stated in its annual report that the losses were "primarily due to the increases in the manufacture and sale of the Lucid Air vehicles in 2023 and inventory and firm purchase commitments write-downs." Although management had an explanation for the widening loss, it likely came up short of mitigating the frustration of investors who wanted to see the company moving toward breakeven on a gross profit basis.

While Lucid hasn't provided a 2024 forecast that addresses profitability, it's reasonable to expect the company's bottom line to remain in the red. Lucid forecasts the production of 9,000 vehicles in 2024, only about 7% more than the 8,428 vehicles it produced in 2023. Production volumes will likely have to increase considerably before investors can expect Lucid to achieve profitability.

Dividends

Does Lucid pay a dividend?

At this time, Lucid doesn't pay a dividend, and it's highly unlikely the company will start to reward investors with a dividend anytime soon. Instead of distributing cash to shareholders, Lucid is focused on allocating capital toward expanding its production facilities in Arizona and Saudi Arabia. In 2024, for example, Lucid projects capital expenditures of $1.5 billion.

ETF options

ETFs with exposure to Lucid

Lest investors think that buying Lucid stock is the only way to gain exposure to the luxury EV manufacturer, investing in an exchange-traded fund (ETF) that includes Lucid among its holdings is another viable option.

Exchange-Traded Fund (ETF)

The iShares Self-Driving EV and Tech ETF (IDRV 2.4%), for example, is an EV ETF that focuses on companies that stand to prosper from growth in the EV industry. Lucid represents 2.63% of the fund's holdings. The ETF has a moderate 0.46% expense ratio and makes semiannual distributions.

The First Trust NASDAQ Clean Edge Green Energy Index Fund (QCLN 3.81%) is another EV-focused ETF that will pique the interest of investors looking for Lucid exposure. This fund includes a variety of clean energy stocks, such as lithium, battery, and solar stocks. Of the fund's 56 holdings, Lucid is the 11th-largest position, representing a 3.13% weighting.

Stock splits

Will Lucid stock split?

While several stocks split in 2023, and various stocks seem like strong candidates to split their stocks in 2024, Lucid almost definitely won't be one of them. Companies often choose to split their stocks when the share prices climb to a price that may prevent investors from buying individual shares. With Lucid stock failing to rise over $5 in early 2024, it seems there's no incentive for Lucid to split its stock now or in the foreseeable future.

Related investing topics

The bottom line on Lucid

While the exuberance surrounding EV stocks has ebbed over the past few years, Lucid has become an industry leader, continuously earning rave reviews from critics. Like any upstart company, though, Lucid has faced challenges.

Cutting production guidance twice in 2023, Lucid disappointed many of its previous advocates. That caused some of the stock's early fans to steer the stock back out of their portfolios. But the potholes Lucid has encountered don't mean the road to success is gone for good. Potential investors must weigh the pros and cons carefully before deciding whether buying Lucid shares is right for them.

FAQ

Investing in Lucid FAQ

Is Lucid a good stock to invest in?

Because investors' risk tolerances, investing goals, and financial situations vary, there's no single answer to whether Lucid is a good investment. Valid arguments can be made for bull and bear cases for Lucid stock. Individual investors must do their due diligence to decide whether Lucid is the right stock.

How can I purchase Lucid stock?

For investors who own brokerage accounts, it's easy to purchase shares of Lucid. People looking to mitigate risk may find that gaining exposure to Lucid through an ETF is a better option.

Is Lucid a publicly traded company?

Yes, Lucid became a publicly traded company after merging with Churchill Capital Corp IV in 2021.

What is Lucid Motors' stock ticker?

Lucid trades on the Nasdaq under the stock symbol LCID.