Artificial intelligence (AI) stocks may have run into a rough patch of late, driven by external factors such as the Iran war, investor concerns about an AI bubble, and the rising odds of a U.S. recession. However, a closer look at AI-driven demand for hardware and software suggests the weakness may not persist for long.

While enterprises adopting AI have been witnessing higher productivity, leading to a strong surge in demand for AI software offerings, companies selling AI hardware have been experiencing robust demand that exceeds their ability to supply. The market researchers at Gartner, for instance, estimate that 40% of enterprise applications will be integrated with AI agents this year, up from just 5% in August 2025.

This is great news for a company such as Palantir Technologies (PLTR 1.96%), an AI software specialist that helps enterprises build AI agents, along with other AI tools. On the other hand, heavy spending on AI data center infrastructure is poised to remain a tailwind for Intel (INTC +2.19%). This semiconductor stock clocked outstanding gains last year and remains in fine form so far in 2026.

Let's look at the reasons why these AI stocks could have a solid year and deliver impressive gains to investors.

Image source: Intel.

Intel: A favorable demand-supply environment should pave the way for better-than-expected growth

Intel stock has already soared by 67% in 2026 despite some bouts of volatility along the way. The company has been impressing investors lately thanks to its progress in AI data centers, where demand for its custom processors and server central processing units (CPUs) has been picking up. In fact, Intel has been struggling to meet demand from data centers for its chips.

NASDAQ: INTC

Key Data Points

The demand for server CPUs deployed in data centers is reportedly exceeding demand, fueled by agentic AI and inference applications. This explains why hyperscalers are reportedly seeking long-term agreements with Intel to secure their supplies of server CPUs. So, there is a good chance that Intel will capitalize by raising its prices.

Market research firm Omdia estimates that the shortage of server CPUs could lead to a 11% to 15% price increase. Given that Intel is working to improve production yields and expects to bring additional production capacity online throughout the year, it is well positioned to capitalize on healthy server CPU demand.

Meanwhile, the company's growing traction in custom AI processors, known as application-specific integrated circuits (ASICs), should be another critical tailwind for it this year. Intel reported a 50% year-over-year increase in its custom AI processor business in Q4. The business has already achieved an annualized run rate of $1 billion in revenue, and it can grow further as demand for ASICs to handle AI workloads continues to grow.

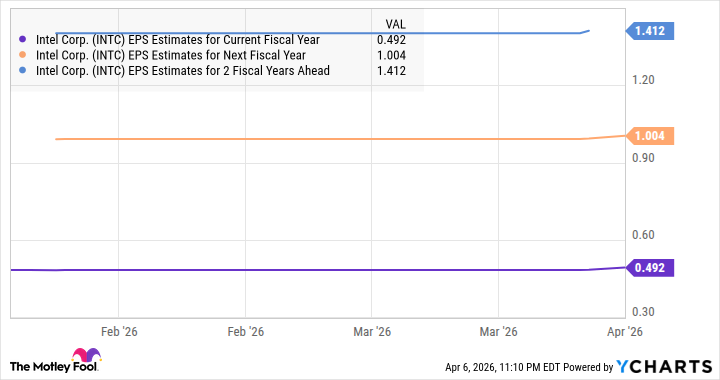

So, don't be surprised if Intel's earnings growth in 2026 exceeds the 15% jump to $0.48 per share that analysts are, on average, expecting. Even better, the chipmaker's earnings are anticipated to increase at healthy rates over the next couple of years as well.

INTC EPS Estimates for Current Fiscal Year data by YCharts.

As such, there is a solid chance that Intel stock will head higher not just in 2026, but also in the long run.

Palantir: Helping customers put AI into action

The productivity gains that AI is helping adopters achieve are the primary reasons for the massive investments in this technology, and Palantir is emerging as a go-to name for enterprises and governments looking to leverage AI to their advantage.

NASDAQ: PLTR

Key Data Points

Customers using Palantir's Artificial Intelligence Platform (AIP) have reported significant cost savings from automating processes, reducing redundancies, and shortening the deployment times of generative AI solutions. General Mills, for instance, points out that it is saving $40,000 a day by using Palantir's generative AI software platform.

This makes it clear why Palantir's customer base is expanding quickly, and the company is gaining more business from existing customers. While its customer count increased by 34% year over year in the fourth quarter of 2025, its net dollar retention rate stood at an impressive 139%. (Net dollar retention is calculated by dividing a company's trailing-12-month revenue from established customers at the end of a period by the trailing-12-month revenue from that same group of customers a year earlier.)

Importantly, Palantir's net dollar retention rate increased by 19 percentage points year over year in Q4. This clearly suggests that its established customers are continuing to spend more money on its offerings over time. As a result, Palantir signed a record $4.3 billion in new contracts in its latest reported quarter, an increase of 138% year over year. That was well above the 70% jump in its revenue to $1.4 billion.

Of course, Palantir stock would need to step on the gas to end 2026 higher, since it has lost almost 27% so far this year. The company's valuation remains a sticking point, as it has a forward earnings multiple of 107 and a sales multiple of 81. But then, it could justify those multiples by outpacing consensus growth expectations in the coming quarters. If it does so, that could be enough to help the stock regain its mojo and fly higher as the year progresses.