Palantir Technologies (PLTR +2.53%) has been one of the greatest stocks you could have bought at the start of the artificial intelligence (AI) boom in 2023. If you invested $10,000 into Palantir at the start of 2023, that sum of money is now worth around $206,000. That's an incredible return in a short time frame, and there's really one product that investors can point to for those results: AIP -- the Artificial Intelligence Platform.

While AIP may not be the most original name out there, its impact has been felt deeply in Palantir's business, driving incredible growth. But after delivering massive gains, is Palantir stock still a buy? Let's take a look.

Image source: The Motley Fool.

AIP is Palantir's generative AI platform

Originally, Palantir was an AI product to help users make sense of vast amounts of information. Originally developed for the defense and intelligence communities, Palantir eventually found use in other branches of government and in commercial applications.

Before 2023 began, Palantir was entering a bit of a business lull and started to see its growth rate dip beneath 20% year over year. Palantir wasn't finding as many clients for its AI platform, but all of that changed when generative AI arrived.

NASDAQ: PLTR

Key Data Points

Palantir offered the AIP platform to help users easily implement AI controls in businesses and develop AI agents to automate tasks on their behalf. This product was wildly successful in attracting new clients to its platform, and the company hasn't looked back.

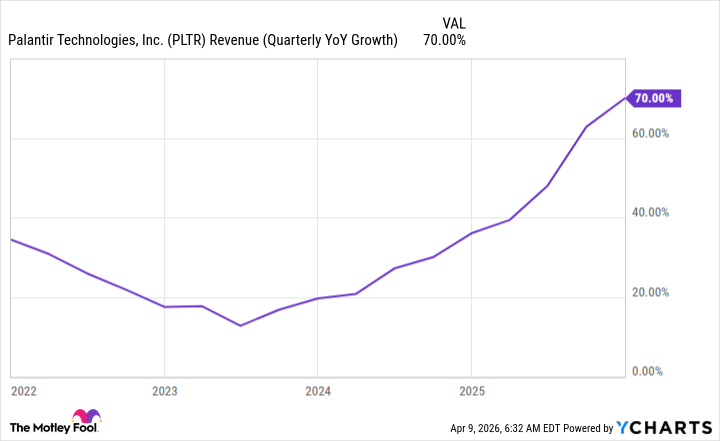

Over the past few years, its growth rate has accelerated, leading to the incredible stock returns discussed above.

PLTR Revenue (Quarterly YoY Growth) data by YCharts

For 2026, Wall Street analysts estimate 62% revenue growth, but Palantir has handily outperformed expectations nearly every year, so don't be surprised if it's even higher. With that kind of growth on the horizon, the stock may seem like a no-brainer buy, but there's one catch: valuation.

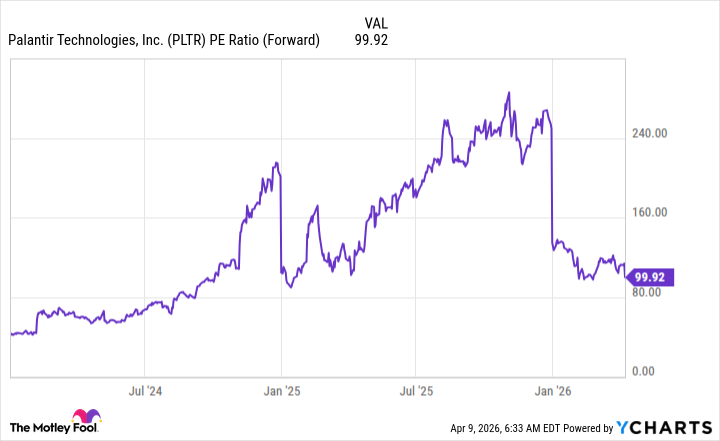

Palantir's stock is overvalued and already has years of strong growth baked in. Although its valuation has come down a fair bit, it still trades for 100 times forward earnings.

PLTR PE Ratio (Forward) data by YCharts

With the forward earnings metric, this year's impressive 62% projected growth is already priced into it. For Palantir to fall to a more reasonable valuation range, say about 33 times forward earnings, it must triple its earnings from the end of this year's level. That's a big task, especially since it needs to rely on revenue growth to do it, because it's already posting impressive 44% profit margins.

As a result, I think investors should probably avoid the stock. There is already too much success priced in, and while I believe the company will continue to thrive, Palantir stock may struggle.