While Wall Street obsesses over graphics processing units (GPUs), Marvell Technology (MRVL +3.98%) quietly powers the networking backbone that makes large-scale AI possible. Its under-the-radar role within AI data centers, combined with a $2 billion strategic boost from Nvidia and a privileged position in the next wave of hyperscaler capital expenditure (capex) budgets, position Marvel for outsize gains that could eclipse the company's better-known peers.

NASDAQ: MRVL

Key Data Points

Understanding Marvell's overlooked role in AI infrastructure

Marvell designs high-speed Ethernet switches that move data at ultra-high speeds and low latency rates across clusters of server racks. Its product line also includes network interface cards and data processing units (DPUs) that off-load encryption and load-balancing tasks from central processing units (CPUs).

One of the biggest reasons Marvell's technology is overlooked is that it's not directly used for training generative models. Instead, the company's hardware ensures that every watt and byte inside an AI cluster is used efficiently. This is important because a single faulty switch or congested link can idle an entire rack of GPUs -- ultimately costing developers both time and wasted capital.

Image source: Getty Images.

Nvidia's investment is a discounted tailwind

A recent catalyst arrived for Marvell following Nvidia's $2 billion strategic investment and partnership. The collaboration aims to leverage Marvell's data center networking and custom silicon divisions to accelerate the next generation of Ethernet switches and DPUs specifically optimized for Nvidia's AI platforms.

This relationship provides Marvell with immediate chip design wins inside the ecosystems that AI hyperscalers are already buying by the tens of billions. Over the next year, investors should be on the lookout for higher growth in the company's networking ASICs and volume DPU shipments as the partnership with Nvidia ramps up.

In my eyes, the broader market has not yet fully priced the multiyear growth trajectory from Nvidia -- or the secular themes accelerating investment in AI infrastructure -- into Marvell's valuation. This lag creates a compelling asymmetric buying opportunity: The upside could be enormous amid the AI infrastructure supercycle, yet the stock price has not fully caught up.

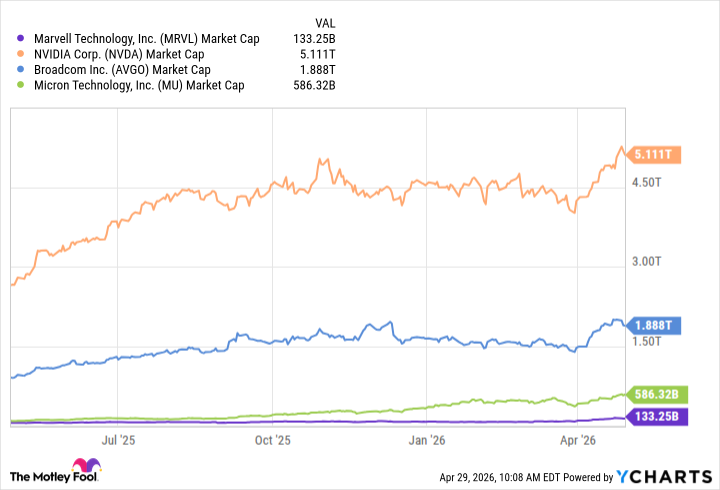

Why Marvell stock could outperform its chip peers

This year alone, the big five hyperscalers are expected to pour $720 billion into AI capex. The smartest investors understand that the spending mix with AI infrastructure budgets is beginning to shift.

While training remains Nvidia's domain, inference demands more power-efficient silicon that can be deployed at huge scale for a lower cost. Marvell's low-power inference engines and custom silicon architecture are ideal for this phase of AI development since they offer big tech a way to better control costs without sacrificing model performance.

Compare these dynamics to the competition. Nvidia's $5 trillion valuation already reflects huge growth for years to come. Any misstep in execution will trigger sharp pullbacks. Broadcom has witnessed success across networking equipment and custom ASICs, but the company also depends heavily on slower-growing software revenue that could dilute its AI upside. And Micron benefits from memory demand at the moment but ultimately remains tied to a notoriously cyclical DRAM industry.

MRVL Market Cap data by YCharts.

In contrast, Marvell combines several AI tailwinds -- networking, inference specialization, and now Nvidia's endorsement -- inside a smaller market capitalization. The company's earnings have more room to surprise to the upside, giving its valuation multiples more room to expand. In a landscape where the crowd already owns the obvious names, the stock remains a sleeper that is poised to deliver more robust returns.