Warren Buffett cemented his status as one of the greatest investors of all time while helping the conglomerate he built, Berkshire Hathaway, post exceptional returns over the long run. However, Buffett had plenty of help along the way, even beyond his longtime friend and partner, Charlie Munger. For instance, he entrusted a portion of his company's portfolio to some lieutenants, Todd Combs and Ted Weschler. One of them was responsible for engineering Berkshire Hathaway's investment in Apple (AAPL +2.70%), a stock that became one of Buffett's favorites.

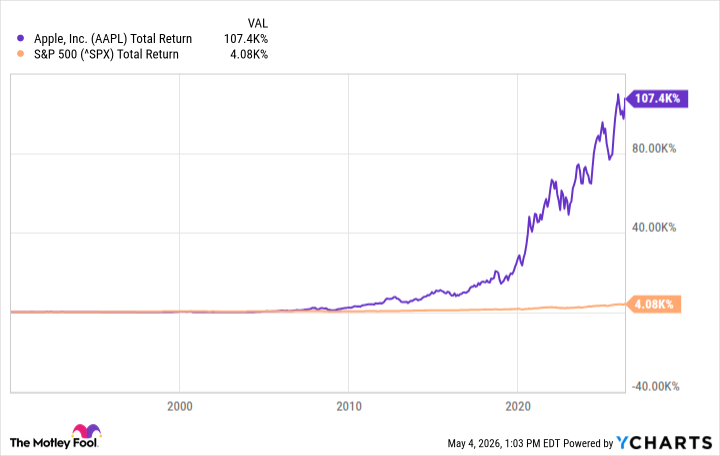

The man once said that Apple is one of the best businesses in the world. The iPhone maker's shares are up significantly since Berkshire Hathaway first invested in it in 2016; and since 1990, Apple has crushed broader equities, with the stock up 107,400%.

AAPL Total Return Level data by YCharts

Yet, there is plenty of upside left. Let me explain.

Outstanding financial results

Apple has had plenty of naysayers in recent years. Some have claimed that excitement over new iPhone releases is dead -- or at least, not nearly as high as it was before. Others have pointed to the company's reliance on China for manufacturing, which caused problems when the U.S. imposed steep tariffs on Chinese imports. There are also fears that Apple will continue to face accusations that it holds a monopoly, with regulators seeking to punish the company severely. And then some claim that Apple has not kept pace with similarly sized peers in the artificial intelligence (AI) market. Despite all that, Apple has delivered solid financial results in recent quarters.

Image source: The Motley Fool.

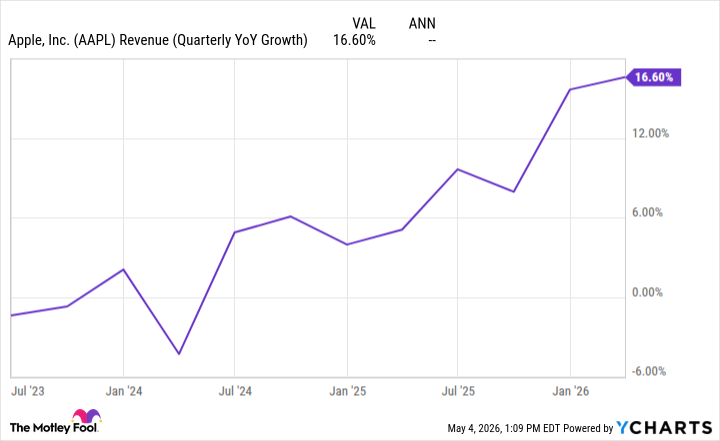

In its latest update for the second quarter of fiscal year 2026, ending on March 28, Apple's sales grew almost 17% year over year to $111.2 billion. That's the fastest top-line growth rate the company has posted in over three years, and it is the second quarter in a row that it sets a new multi-year high on that front.

AAPL Revenue (Quarterly YoY Growth) data by YCharts

On the bottom line, Apple's earnings per share climbed by 22% year over year to $2.01. The company's largest segment -- the iPhone -- did much of the heavy lifting, with sales of Apple's signature device totaling about $57 billion, up almost 22% from the prior-year quarter. Apple's latest iPhone, the 17, is clearly seeing immense success, partly thanks to the company's integration of AI capabilities into the device. And it's not just the iPhone: Apple is using AI to boost the capabilities of other devices. These efforts may be paying off.

The future is still bright

Apple's hardware business could remain strong over the foreseeable future. Here are two reasons why. First, the company is still finding ways to improve its products. Apple plans to release a more personalized Siri, powered by AI, later this year. A more powerful digital assistant could potentially boost demand for the company's devices, leading to higher sales. Second, Apple is increasingly competing in new niches to attract new customers and expand its installed base. For instance, the company introduced its cheapest laptop ever earlier this year.

NASDAQ: AAPL

Key Data Points

Apple is also rumored to be working on a Fold version of the iPhone, a twist on smartphones that has proven highly popular for some tech leaders. Of course, Apple's hardware business is only one part of the company's long-term strategy. The company's high-margin services segment will only get better with a stronger installed base. Apple now has more than 2.5 billion active devices.

In its Q2 2026, services revenue reached an all-time high, growing 16% year over year to about $31 billion. There is a massive long-term opportunity here as Apple's ecosystem of services grows, and this segment helps the company expand its margins and profits. True, Apple does face some risks, and the stock isn't cheap: it trades at 32.8x forward earnings, as of writing.

The average forward price-to-earnings for information technology stocks is 23.5. Even so, Apple has shown that it can perform well despite its challenges, and given the company's wide moat and attractive growth avenues, it is worth a premium. Apple's shares are still worth buying.