The U.S. is home to 10 companies worth $1 trillion or more, but only four have graduated into the $3 trillion club as of this writing:

- Nvidia: $4.8 trillion

- Alphabet: $4.6 trillion

- Apple: $4.1 trillion

- Microsoft: $3.1 trillion

I think Meta Platforms (META +2.27%) could join them as soon as next year. The company is about to transform the user experience on its Facebook and Instagram social networks with artificial intelligence (AI), and the result could be much higher engagement and significantly more advertising revenue.

Meta has a market capitalization of $1.55 trillion as I write this. So if the company does become a member of the $3 trillion club, investors who buy its stock today could almost double their money.

Image source: The Motley Fool.

Social media is about to enter a new era

Over 3.5 billion people use at least one of Meta's social media apps every single day. Since that number is quickly approaching half the population of the entire world, it's becoming harder and harder for the company to acquire new users, which poses a risk to its advertising business. But Meta can also generate growth by making each existing user more valuable. It can achieve that by keeping them online longer, so they see more ads.

Meta has embedded AI into its recommendation algorithms for the last few years; it learns what type of content each user likes to see, and feeds them more of it. This drove an uptick in engagement throughout 2025, particularly for the Reels video content format, which is especially popular with users right now. However, Meta's CEO Mark Zuckerberg is ready to take this strategy a step further.

During the first-quarter conference call with investors on April 29, he outlined a new vision to convert Facebook and Instagram from apps for social connection and entertainment into something else entirely. He said Meta's latest AI models will be able to specifically understand what each piece of content on its platforms is about and will also achieve a deeper understanding of every user's goals -- whether they are trying to learn how to cook or want more information about global events.

This information will allow Meta to curate a highly personalized experience unlike anything the social media industry has seen, involving the company creating specific content to help each user accomplish their goals. In simpler terms, rather than offering mindless entertainment, Facebook and Instagram will serve as useful hubs that people visit to improve their lives. This might be the key to significantly higher engagement over the long term.

NASDAQ: META

Key Data Points

Meta's revenue and earnings growth accelerated in the first quarter

Meta generated $56.3 billion in revenue during the first quarter of 2026. That was a year-over-year increase of 33%, and an acceleration from the 24% growth the company delivered in the fourth quarter of 2025 (three months earlier).

Moreover, Meta's first-quarter earnings soared by 61% to $10.44 per share, a significantly faster growth rate than the 11% it delivered in the fourth quarter. The company had a one-off tax benefit that contributed $3.13 in earnings during the first quarter, but growth would still have accelerated even without it.

These results suggest that Meta's AI-driven strategy to boost user engagement is working, but putting it into motion certainly isn't cheap. That brings me to a key number Wall Street was watching closely in Meta's first-quarter report: capital expenditures (capex), which is the money the company spends on AI data center infrastructure, chips, and other components.

Meta's capex hit a record of $72.2 billion in 2025, and management expects it will explode to as much as $145 billion during 2026. This spending will impact the company's earnings power as the infrastructure is depreciated (for accounting purposes) over time, but it could also fuel a massive uptick in revenue and earnings if the early results are anything to go by.

Meta has a mathematical path to the $3 trillion club

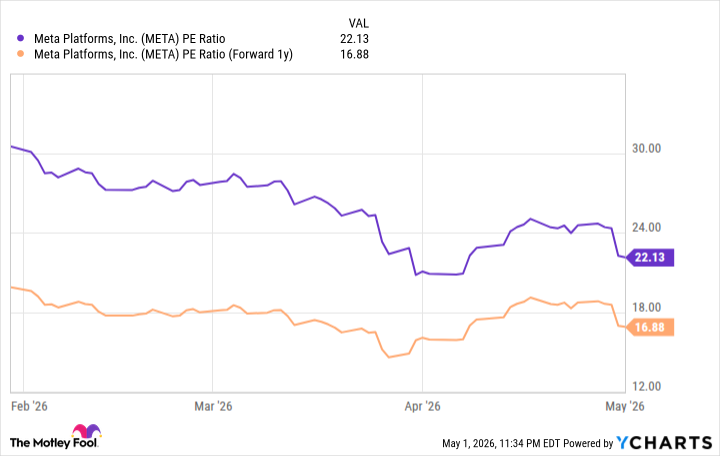

Based on Meta's trailing 12-month earnings of $27.51 per share, its stock is trading at a price-to-earnings (P/E) ratio of 22.1. That's a steep discount to the Nasdaq-100 index, which currently trades at a P/E ratio of 33.9, suggesting that Meta is extremely undervalued compared to its big-tech peers.

Plus, Wall Street believes Meta will grow its earnings to $34.60 per share in 2027 (according to Yahoo! Finance), giving its stock a forward P/E ratio of just 16.9.

Data by YCharts.

That means Meta Platforms stock would have to double by the end of next year just to trade in line with the P/E ratio of the Nasdaq-100, which would catapult its market capitalization to $3.1 trillion. This outcome isn't out of the question, considering that Meta's P/E was above 30 on more than one occasion over the last 12 months -- so a journey into the ultra-exclusive $3 trillion club could be right around the corner.