In the world of artificial intelligence (AI) infrastructure, few names are sparking debate as much as Poet Technologies (POET +4.34%). The semiconductor company sits at the intersection of light-based computing and the hunger from data centers for faster, cooler data movement.

So far in 2026, Poet's stock has benefited from enthusiasm among growth investors rotating away from big tech. However, its shares recently cratered due to some managerial setbacks.

Poet's volatile price action has left investors wondering if the dip represents a bargain entry point into a company that's going to deliver tomorrow's game-changing technology, or a risky gamble on an unproven player.

Image source: Getty Images.

Photonics could be an engine powering AI's next leap

Photonics uses light to transmit and process information. The goal is to replace sluggish electrons traveling through copper wires with photons moving through optical channels at light speed while consuming less power. As AI models expand in size, servers need to shuttle higher volumes of data between chips, racks, and facilities, and they need to do so in ways that avoid the hardware melting under heat or choking on latency.

Traditional electrical interconnects have physical limits, but photonics promises a scalable hatch featuring higher speeds, lower energy consumption, and easier cooling mechanisms. Poet's Optical Interposer platform functions as a bridge at the wafer level -- fusing photonic and electronic components meant to eliminate manual alignment, reduce costs, and enable high-volume production of optical engines tailored for AI accelerators.

Image source: Poet Technologies investor relations.

Is Poet Technologies profitable?

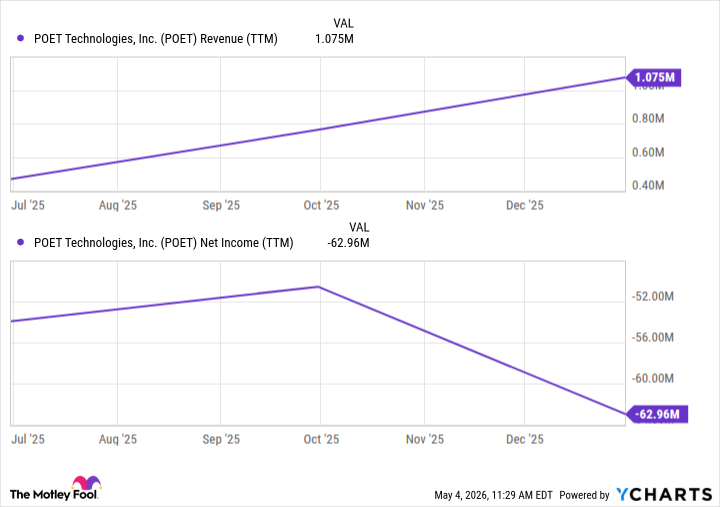

At the moment, Poet is a tiny outfit in financial terms -- generating revenue in the low hundreds of thousands of dollars per quarter while posting net losses in the tens of millions of dollars. The company is far from profitable and carries the classic profile of an early-stage innovator: enormous spending today in hopes of explosive growth tomorrow.

POET Revenue (TTM) data by YCharts.

Hype meets reality in Poet's latest price action

Poet is not a meme stock conjured from thin air. Companies building optical interconnects and exploring photonics have been fetching some interest in the AI community for a little while now. Nevertheless, Poet's commercial traction remains nascent, making it more of an ambitious technology bet than a sure thing.

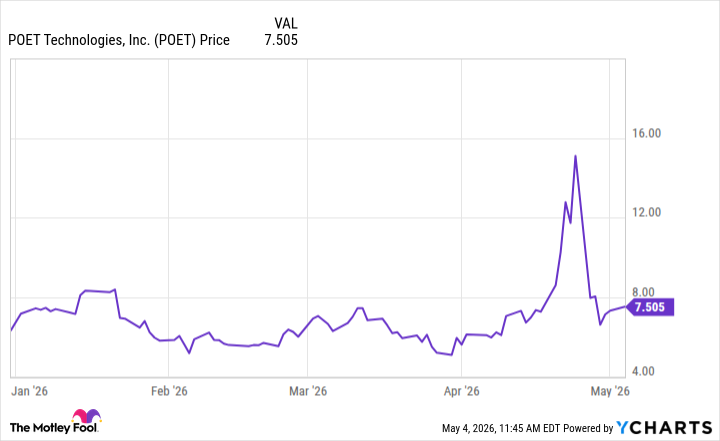

Poet stock recently soared in response to whispers of meaningful traction and apparent order confirmations tied to a high-profile customer. The stock's abrupt reversal came after a publicized detail about an order from Celestial AI -- a subsidiary of Marvell Technology -- triggered a confidentiality dispute. The order commitment was swiftly rescinded, and Poet's stock plunged by more than 50% in a matter of days.

NASDAQ: POET

Key Data Points

This episode exposed how the classic growing pains of overeager communication from management can collide with proper corporate protocols. It's a harsh reminder that early revenue pipelines can evaporate overnight.

The current dip in Poet stock might look like a tempting opportunity based on chart patterns. And while the thesis for the technology holds long-term merit in a photonics-hungry AI world, near-term execution risks, limited revenue, and governance stumbles make Poet a highly speculative stock pick.

For patient investors who have bought into the idea that light will emerge victorious in the interconnect war, Poet's current price may offer an attractive entry. For most investors, however, buying Poet shares will likely feel like catching a falling knife -- at least until the company achieves its next shipment milestone. While the dip is real, whether this is the right time to take advantage depends on your personal risk tolerance for a volatile ride toward an uncertain payoff.