Shares of customer relationship management software specialist Salesforce (CRM 0.28%) just can't seem to catch a break. The stock has shed more than 30% in 2026 as of this writing. And over the past 12 months, shares are down about 36%.

These declines come despite the company posting a record fiscal fourth quarter in late February that arguably should have given the stock a meaningful lift.

So what's going on?

I think it has everything to do with artificial intelligence (AI) -- and I think the weight on the stock may be more significant than some investors think.

Image source: Getty Images.

A business that still looks healthy

By the performance of Salesforce's business, you wouldn't guess that its stock would be suffering.

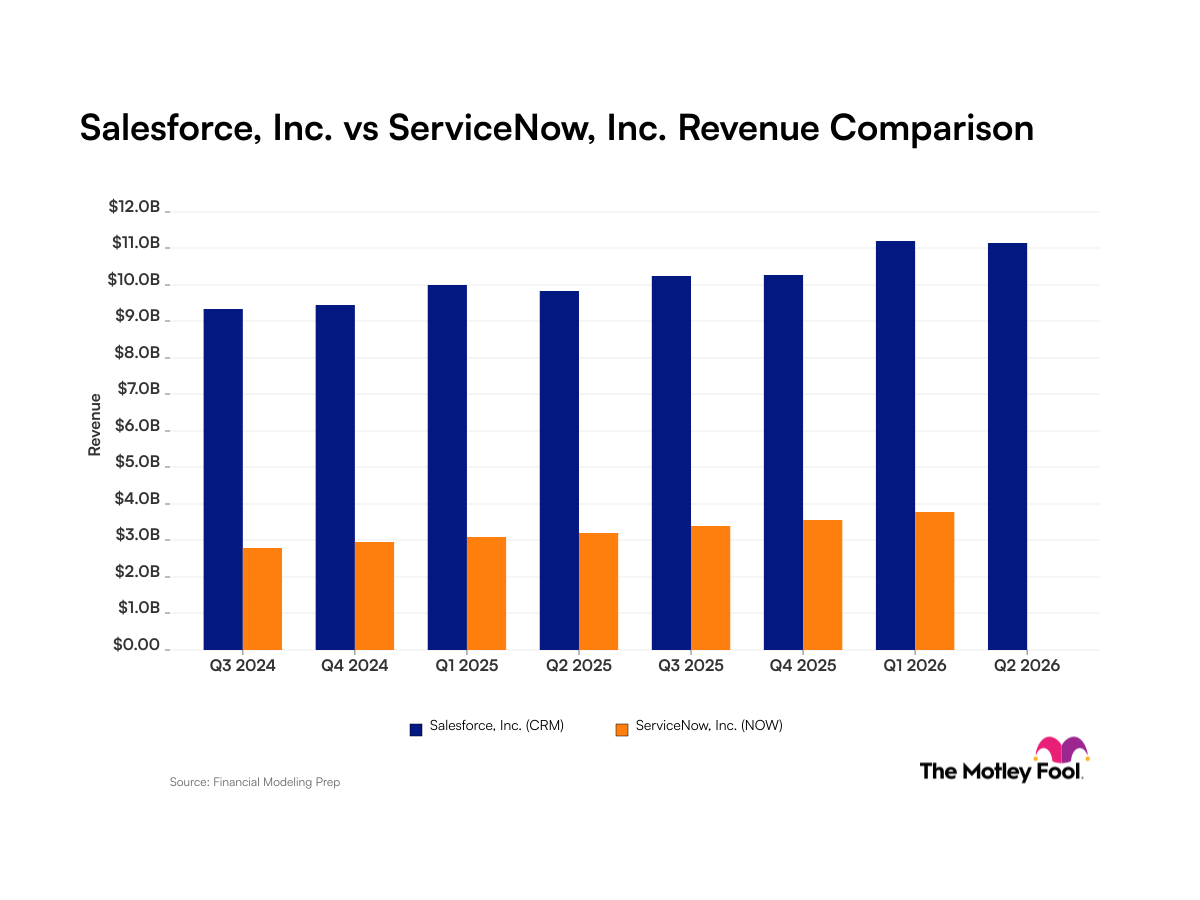

Salesforce's fiscal 2026 fourth quarter, which ended Jan. 31, 2026, was strong.

Revenue for the period rose 12% year over year to $11.2 billion. And free cash flow for the full fiscal year climbed 16% to $14.4 billion.

Further, the company's contracted future revenue looked encouraging, too. Current remaining performance obligations grew 16% year over year to $35.1 billion, while total remaining performance obligations reached $72.4 billion.

And the company is firing on all cylinders with AI offerings.

Agentforce, the agentic AI platform that launched in late 2024, saw its annual recurring revenue reach $800 million in the period -- up 169% year over year. And when combined with the company's Data 360 offering, Salesforce's AI-related annual recurring revenue topped $2.9 billion -- a more than 200% jump. Further, Salesforce has now closed 29,000 Agentforce deals since launch.

"Agentic AI is a tailwind for our business, and we're well on our way to $63 billion in revenue in FY30," said Salesforce CEO Marc Benioff in the company's fiscal fourth-quarter earnings release.

Additionally, management is matching that growth with shareholder returns.

Salesforce returned $14.3 billion to shareholders during fiscal 2026. And in February, the company authorized a new $50 billion share repurchase program -- its largest ever. And, in March, Salesforce commenced a $25 billion accelerated share repurchase under that authorization.

NYSE: CRM

Key Data Points

An overhang that may not lift soon

So, what's going on with the stock? I believe there's a worry that AI may erode the software-as-a-service model itself. Salesforce, like many of its peers, has long monetized through per-seat licensing; if AI agents really do replace meaningful chunks of repetitive knowledge work, customers may need fewer seats over time -- or push vendors toward consumption- and outcome-based pricing.

This concern triggered the so-called "SaaSpocalypse" in February, when Anthropic's launch of new agent-based tools for its Claude model touched off a brutal sell-off in software stocks. Highlighting this overarching fear, the iShares Expanded Tech-Software Sector ETF (IGV +1.92%) is down sharply this year.

Of course, Salesforce's response to this potential AI threat has been aggressive.

Late last year, the company rolled out an "Agentic Enterprise License Agreement" that bundles agent capacity into seat-based contracts. And late last year, it closed the acquisition of data-management specialist Informatica, expanding its data management capabilities. Further, in late March, Salesforce unveiled the biggest overhaul of Slack since the 2021 acquisition, introducing more than 30 new AI capabilities for Slackbot and announcing that every new Salesforce customer would get Slack provisioned automatically starting this summer.

These moves should help.

But here's the problem: Even if Salesforce ultimately emerges from this transition in a strong position, skepticism surrounding AI's potential impact on software companies could persist for years. AI capabilities, after all, only seem to keep improving -- and the worry that customers eventually rationalize their software stacks isn't going away simply because Agentforce is growing fast today or because Salesforce is finding other ways to benefit from AI.

The stock's price-to-earnings ratio is at just 14, which is hardly demanding for a company generating this much free cash flow and committing to such a large buyback. But cheap stocks can stay cheap when the market is grappling with a structural concern. Until there is clearer evidence that AI is a net tailwind for the overall business, I would rather watch from the sidelines.