The market hit a turning point on April 1. At the time, it was at relative lows thanks to concerns over the Iran war and what artificial intelligence (AI) spending would look like. Both of those fears are still prevalent, but they aren't controlling the market, as actual quarterly results have sparked new AI investment fervor. Broadcom (AVGO +2.03%) was one of the bigger beneficiaries of this, and is up nearly 40% since April began.

That's a huge rally in about a month and a half, and it may have investors wondering if Broadcom is still a buy after this major run-up. So, what should you do with the stock?

Image source: The Motley Fool.

Investors should be focused on 2027

Broadcom is known for several different offerings, but the most influential right now is its custom AI chips. Broadcom has partnered with several AI hyperscalers to design a custom AI chip that can deliver superior cost advantages over GPU-based training and inference. AI hyperscalers are looking to maximize their spending in any way possible, and this is one way to do it.

NASDAQ: AVGO

Key Data Points

The most prevalent custom AI chip Broadcom is involved with is Google's Tensor Processing Unit (TPU). TPUs are available via Google Cloud, but are also starting to be sold to external clients. There are several AI hyperscalers that are launching custom AI chips this year and next year, so that should result in Broadcom's market presence expanding.

The opportunity for these chips is massive, and Broadcom's CEO believes this business unit will generate over $100 billion in revenue during 2027. For reference, the business unit these chips are a part of now generated $8.4 billion in revenue during the first quarter, and there were other products in that division that contributed to that total as well. Wall Street analysts project Broadcom's revenue will rise from $63.9 billion at the end of its fiscal 2025 (which ended in November) to $158 billion by the end of fiscal 2027. That's a major jump, and makes me want to look at how the stock is valued from a forward earnings standpoint.

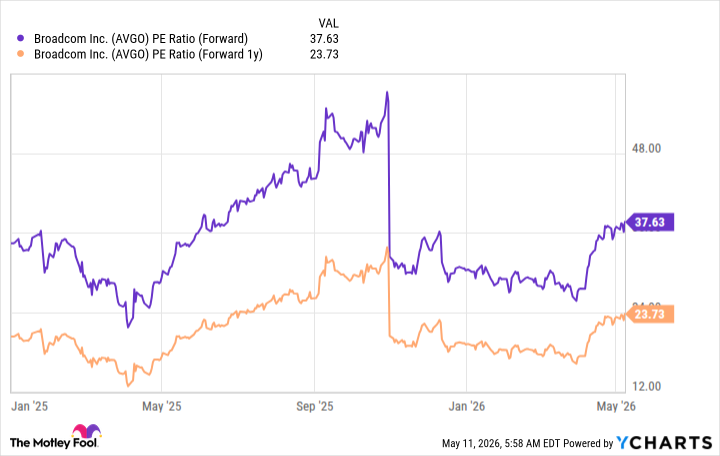

AVGO PE Ratio (Forward) data by YCharts

Broadcom shares now trade for 38 times 2026 estimates and 24 times 2027 estimates. Those aren't cheap valuations, and Broadcom will need to outperform expectations in order to really drive strong returns. However, I think that's entirely possible, especially with AI hyperscalers needing to build more computer power but running out of capital resources.

Broadcom's upside is certainly less than it was a month ago, but I think it's still enough to warrant buying and owning shares now.