Home Depot (HD +0.56%) is one of the best-performing stocks in history, but more recently, the leading home improvement chain has been struggling.

The last few years have been tough for the housing and home improvement sectors. Interest rates and mortgage rates remain elevated compared with much of the 2010s, and discretionary spending has been hampered by years of high inflation. Meanwhile, the lock-in effect from the pandemic has significantly slowed home sales, curtailing demand for home improvement products, as moving homes typically triggers spending on such supplies.

Against that backdrop, Home Depot reported first-quarter earnings Tuesday morning, and the results were in line with estimates.

Image source. Home Depot.

Home Depot's Q1

Comparable sales rose 0.6% in the quarter and 0.4% in the U.S., and revenue was up 4.8% to $41.77 billion, which was slightly ahead of estimates at $41.51 billion.

On the bottom line, adjusted operating income fell 2.3% to $5.15 billion, and adjusted earnings per share fell from $3.56 to $3.43, as the company noted "greater consumer uncertainty and housing affordability pressure." That was still slightly ahead of the consensus at $3.41.

Looking ahead to the rest of the year, the company reaffirmed its guidance, calling for total sales growth of 2.5% to 4.5%, 15 new stores, and adjusted earnings-per-share growth of flat to 4%, or $14.69-$15.28, which compared to estimates at $15.04.

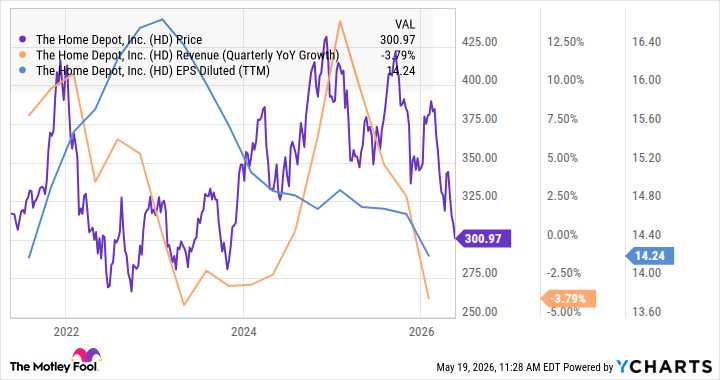

Home Depot has essentially been treading water in a challenging environment for the last several years, and it continued to do so in the quarter.

As you can see from the chart below, the stock has pretty much been flat over the last five years, while earnings per share has fallen, and revenue growth has been nearly flat after backing out the impact of the SRS acquisition, which caused the spike in revenue growth in late 2024.

Is Home Depot a buy?

Home Depot has executed reasonably well in a difficult environment, and the SRS acquisition seems like it is paying off as it is driving growth, and the subsidiary, which is a building materials distributor, is gaining market share.

However, in a cyclical industry, decent execution isn't enough to drive stock growth, especially at a time when the market is enamored with AI.

Additionally, the macro factors seem like they're only going to get more challenging in the near future as gas prices have shot up from the war in Iran, and mortgage rates have risen as well, which should ensure that the housing market remains sluggish.

For a stock that's struggled over the last five years, Home Depot also isn't particularly cheap, trading at a price-to-earnings ratio of 21 with a 3.1% dividend yield. The company has paused share buybacks as well, which were previously an engine of EPS growth.

I think the long-term story is still compelling for Home Depot, but if you're looking to put new money to work, there are better options in the current market. Given the macro headwinds, I think the stock will continue to underperform for the next year or two, if not longer.