Although the energy sector has been the best-performing sector so far this year (based on S&P 500 company performances), the tech sector has made an impressive rebound after a rocky start. The tech sector is the S&P 500's second-best-performing sector through May 25.

Although the sector as a whole is thriving, not all tech companies have been on that same path. But if you're looking to add a couple of tech stocks to your portfolio, the following two are great options. One is a staple that stands to gain significantly from the current artificial intelligence (AI) boom, and the other is an undervalued "Magnificent Seven" stock with significant upside.

Image source: The Motley Fool.

1. Taiwan Semiconductor Manufacturing

Taiwan Semiconductor Manufacturing (TSM +5.29%) -- also known as TSMC -- is the world's largest semiconductor (chip) foundry, manufacturing custom chips for everything from smartphones to computers to data centers. Its unmatched scale and efficiency have made it the go-to for most major tech companies looking to bring their chip designs to life.

As of the fourth quarter of 2025, TSMC had a 70% market share in the global semiconductor foundry market. When you zoom in further, its market share in advanced AI chips is nearly a monopoly. That's why TSMC has been able to flex its pricing power, because it knows companies don't have a viable alternative.

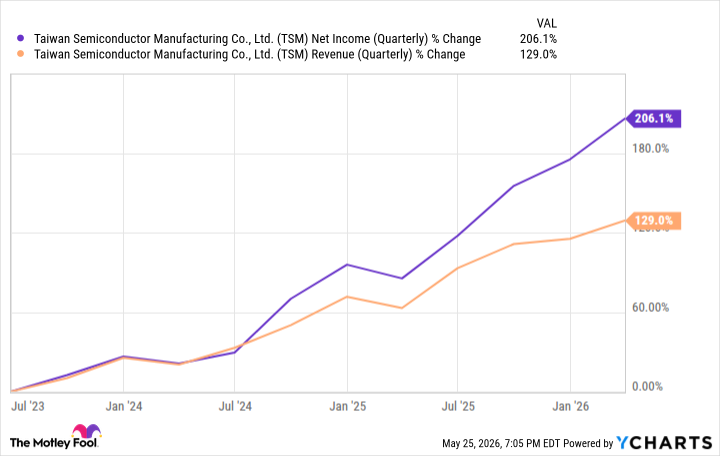

Both TSMC's profits and its net income have been growing impressively, but the premium pricing it commands is partly why its net income has been growing noticeably faster than its revenue. In the first quarter of 2026, TSMC's revenue increased 40.6% year over year to $35.9 billion, and its net income increased 50.5% to $18.1 billion.

TSM Net Income (Quarterly) data by YCharts

As major tech companies rush to build out data centers and expand their AI infrastructure, TSMC is poised to be a major beneficiary. Many companies will design chips, but most will rely on TSMC to produce them.

Even beyond current and projected AI demand, TSMC is one of the most valuable companies to the tech world, and its competitive moat is among the strongest in any tech industry.

NYSE: TSM

Key Data Points

2. Meta Platforms

Meta Platforms (META +2.27%) isn't off to a great start this year, down over 6% year to date (as of May 25). However, the current slump has the stock nearing undervalued territory. At the time of writing, Meta is trading at around 18.9 times its projected earnings over the next 12 months. That makes it by far the cheapest of the Mag 7 stocks, the next cheapest being Nvidia at 24.1.

Its price-to-earnings ratio alone doesn't make Meta an automatic buy, but it definitely helps and gives it more upside than downside. That's a great value for a company that has a growing core business and that's growing revenue 33% year over year, net income 61% (though some tax benefits helped), and operating income by 30%.

NASDAQ: META

Key Data Points

Advertising is undoubtedly Meta's bread and butter (over 97% of its Q1 revenue), so it's encouraging to see it continue to grow in this area. Ad impressions were up, average price per ad increased, and people are spending more time watching Reels and Facebook videos.

It isn't Meta's main businesses that investors have necessarily been worried about, though. It is its capital expenditure (capex) plans, with the expectation that capex will be between $125 billion and $145 billion this year (up from the previous $115 billion to $135 billion range). But it isn't necessarily the number that matters; it's Meta's plan -- or seeming lack thereof -- that has brought hesitation.

The return on capex Meta receives won't be seen immediately, but with its low valuation and thriving core business, there's a margin of safety baked into Meta's stock.