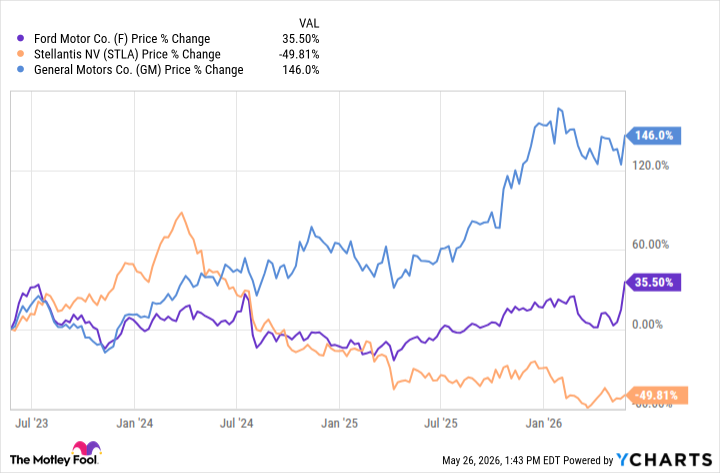

While Ford Motor Company, General Motors, and Stellantis (STLA 1.94%) all have Detroit roots and are the closest of competitors, their stocks have traded wildly differently in recent years.

Until just recently, Ford has been stuck in neutral, battling quality concerns, recalls, and warranty costs, while GM has surged higher on cost discipline and heavy share buybacks. Stellantis has spiraled lower after years of market share losses in its core North America profit engine and massive electric-vehicle-related charges. Savvy investors see opportunity in Stellantis, as it may have the most upside after shedding so much value. For Stellantis to gain traction with its turnaround and reward investors, these three things need to happen.

Solve the affordability crisis

The pressure on consumers to pay more and more for each vehicle is reaching crisis levels. Not only have new vehicle prices surged to around $50,000, but insurance rates have also seen a big spike in recent years, and repair costs are on the rise. There is significant demand for more affordable vehicles, and Stellantis needs to quickly regain lost market share -- it's a perfect strategic fit.

The good news is that Stellantis is preparing to attack the affordability problem head-on by launching nine vehicles priced under $40,000 by 2030 in North America, and even better is that two of those vehicles will be below $30,000. The new product blitz will give consumers a number of affordable options, and potentially lure consumers from other brands, which is typically expensive in the automotive industry.

Image source: Stellantis.

Improve empty capacity

Automakers have a finite amount of production capacity, limiting them to the number of vehicles they can produce regionally and globally. While Toyota Motor is currently running near max capacity in the U.S., Stellantis finds itself at the opposite end with unfilled production capacity, which erodes margins quickly.

As more affordable vehicles launch, it will help improve volume -- Stellantis aims to grow volume by 35% in North America -- and help fill unused capacity, improving margins along the way. Stellantis is aiming to increase production enough to improve capacity utilization in the U.S. to 80% by the end of this decade. These factors should help Stellantis boost its adjusted operating income margin in North America to between 8% and 10%, with revenue also jumping 25%.

NYSE: STLA

Key Data Points

Combine forces

Stellantis is also taking steps to aggressively expand its global partnerships to help drive the automaker forward in several areas. The automaker's key alliances are with tech giants, mobility platforms, and even Chinese automakers.

One key partnership is Stellantis' holding in the Leapmotor International joint venture, which has been at 51% since 2023. That ownership gives Stellantis exclusive rights for the sale and manufacturing of its products outside greater China. This partnership could lead to a number of developments, including the possibility of Stellantis building electric vehicles (EVs) in Canada with Leapmotor. Largely, this partnership will enable Stellantis to grow its sales, learn from the advanced EV prowess of its Chinese counterpart, and share capital expenses.

This is but one of very many partnerships Stellantis is currently involved in, or working to create -- there's a lot of opportunity.

What it all means

These three factors are all intertwined within a larger Stellantis plan unveiled on May 21. The $70 billion five-year plan is geared toward a complete overhaul and turnaround for the beleaguered automaker. Roughly 70% of that global investment will be focused on key brands Jeep, Ram, Peugeot, Fiat, and the Pro One commercial division.

Investors should be optimistic that the automaker has the right objectives in place; it just comes down to execution. Stellantis finally has an identity, with the majority of its investments focused on key brands while the remaining of the 14-brand list becomes more regionalized. As the automaker unleashes a long list of affordable vehicles, improves capacity utilization, and leans on key partnerships for expertise and cost sharing, there should be a viable path forward for Stellantis and investors brave enough to hop on for the long haul.