In the world of technology investing, few companies have commanded the level of cultural and financial dominance that Apple (AAPL -1.53%) achieved during the first two decades of the 21st century. From the iPod to the iPhone, it delivered an impressive run of must-have devices that redefined entire hardware categories.

Yet once the smartphone market matured and rival products became competitive, Apple's hypergrowth phase gave way to a more measured expansion supported by services, ecosystem lock-in, and share repurchases.

Today, I think Nvidia (NVDA -2.86%) may be following a similar script. After years of explosive gains driven by the rise of artificial intelligence (AI), is the graphics-chip leader starting to resemble a maturing Apple?

The parallels between them are striking -- product dominance followed by valuation compression and continuous stock buybacks. While the market increasingly prices Nvidia as a steady AI infrastructure business, the breadth of its untapped opportunities beyond data centers suggests it remains far from the post-innovation plateau that Apple reached after the Steve Jobs era.

Image source: Nvidia.

Apple's transition from product innovator to financial engineer

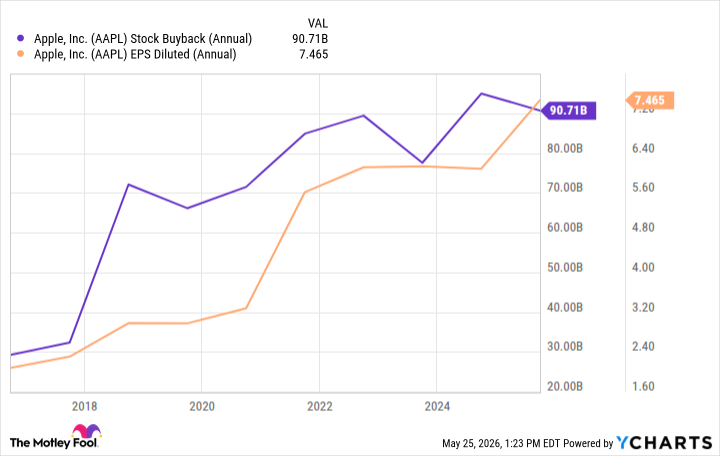

From the early 2000s through the mid-2010s, Apple was defined by its hardware products. But as the smartphone market grew saturated and replacement cycles lengthened, Apple's growth slowed. Rather than allowing revenues to stagnate, Apple intensified its efforts in the services arena -- bolstering App Store, iCloud, and Apple Pay -- which helped deepen its ecosystem moat.

Recurring revenue from services provided a level of stability even as the company's hardware growth moderated. Yet beneath the surface, a fundamental shift was making its way through Apple in the post-Jobs era. Hardware innovations became much more rare -- AirPods being a notable exception.

As new product launches slowed, Apple turned to an aggressive stock-buyback program. By systematically reducing its share count, the company essentially engineered robust earnings-per-share (EPS) growth even though headline revenue growth was modest.

AAPL Stock Buyback (Annual) data by YCharts.

Are the first cracks beginning to show for Nvidia?

Between 2022 and 2025, Nvidia's GPUs became the indispensable pick-and-shovel hardware for training and inferencing AI workloads. The company's data center revenue exploded, its gross margin expanded, and the stock delivered generational returns for those who bought early and held on.

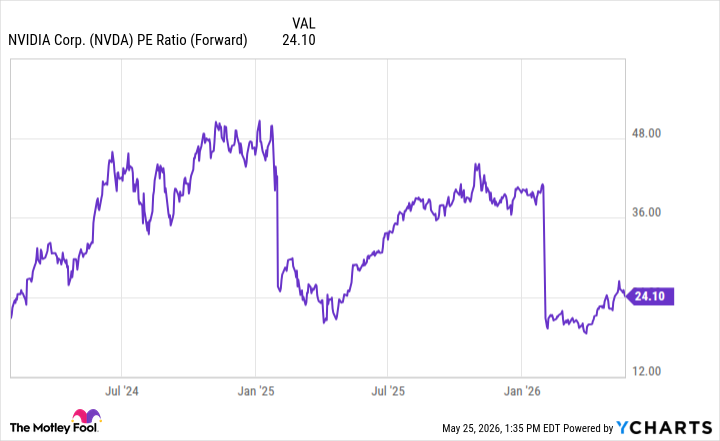

Yet for almost a year now, the upward trajectory of Nvidia stock has been more muted compared to other AI chip stocks. The explosive valuation expansion witnessed during the early phases of the AI boom has started to compress, even as the company continues delivering outstanding quarterly results.

After years of treating Nvidia as a hypergrowth beneficiary of the AI supercycle, many investors now appear to be framing the company as a maturing infrastructure business -- dominant in its core market, but increasingly hemmed in by the law of large numbers.

NVDA PE Ratio (Forward) data by YCharts.

Like Apple, Nvidia has also employed a series of share repurchases. I think the company's latest $80 billion buyback authorization is a clear signal that management believes shares are undervalued.

Is Nvidia more than just a data center business?

Nvidia sits at the intersection of several secular waves that are yet to crest. The company's CPU ambitions with Intel, its new networking partnership with Nokia, and its strategic collaborations with equipment providers such as Lumentum and Coherent represent several new addressable markets.

Meanwhile, the rise of neoclouds, an emerging runway in the autonomous driving space, and forays into robotics and space exploration further expand the company's opportunities.

None of these initiatives is meaningfully moving the financial needle for Nvidia today. The company's results are still overwhelmingly driven by data center GPU sales -- which, might I add, are accelerating again.

NASDAQ: NVDA

Key Data Points

I think Nvidia's current valuation profile discounts these new tailwinds. By treating it as a maturing AI play -- much as Apple was perceived as a maturing consumer tech platform -- investors may be overlooking all of the optionality embedded in the company's diversified roadmap.

While stock buybacks provide short-term support to earnings per share, they are not Nvidia's primary story. The main theme here is optionality on a scale that Apple simply never enjoyed after its hardware peak. For these reasons, I do not think Nvidia is turning into the next Apple. The company is still very much a pillar of the AI computing era, with numerous growth vectors that extend well beyond any single product category.