Intel stock has turned in a stellar performance on the market over the past year, rising by an incredible 488% as of this writing, as demand for the company's chips has started to improve due to their deployment in artificial intelligence (AI) data centers.

Intel missed the AI chip boom initially, as its central processing units (CPUs) weren't suited for training large language models (LLMs) that required a lot of computational horsepower. Nvidia ran away with the AI chip market thanks to its graphics cards, which can perform massive parallel calculations, making them ideal for training AI models.

But as AI compute moves from the training to the inference phase to unlock the technology's productivity gains, demand for energy-efficient CPUs and custom AI processors has begun to rise. That's because the inference phase doesn't require as much computing power as training AI models. As a result, Intel is now witnessing healthy demand for its CPUs and application-specific integrated circuits (ASICs).

However, the phenomenal rally in Intel stock means that investors will have to pay a whopping 904 times earnings to buy it right now. But they can buy shares of Qualcomm (QCOM 3.20%) at a significantly cheaper valuation, and doing so could turn out to be a smart move as this sleeping chip giant seems like a better play on AI inference than Intel.

Let's look at the reasons why.

Image source: The Motley Fool.

Qualcomm can win big from several AI inference applications

The smartphone business has historically been Qualcomm's bread and butter. However, the tilt toward AI inference has opened a whole new opportunity for the company. Qualcomm started making progress in AI chips last year with its inference-focused AI200 and AI250 rack-scale data center solutions, noting that Saudi Arabian AI company Humain will deploy these solutions to power 200 megawatts (MW) of AI data centers.

NASDAQ: QCOM

Key Data Points

Though the deployment is on the smaller side, Qualcomm management struck a positive note on the April earnings call about the future of its AI chip business. CEO Cristiano Amon remarked:

In data center, the Alpha Wave integration is off to a great start and we are pursuing multiple opportunities with large hyperscalers, cloud service providers, sovereign AI projects, and other global partners. Building on that momentum, we are also entering the custom silicon space, beginning our ramp with a leading hyperscaler and we expect initial shipments in December.

In addition, development of our leading data center CPU and high performance AI inference accelerators is progressing well. We look forward to sharing more details and customer wins at Investor Day in June.

It now appears that TikTok owner ByteDance could be among those major customers looking to deploy Qualcomm's AI inference accelerators in its data centers. As reported by Bloomberg, ByteDance is on track to buy "millions" of Qualcomm's custom AI processors, becoming one of its first major customers.

Bloomberg adds that ByteDance is procuring Qualcomm's chips to power its agentic AI software. Given that Amon pointed out that it is "pursuing multiple opportunities" in the AI chip space, don't be surprised to see the company's AI customer base swell further.

Importantly, Qualcomm's AI chip opportunity isn't limited to just data centers. The company has also been pursuing the edge AI hardware market. Edge AI devices are those that can process AI workloads locally instead of relying on cloud computing. Smartphones, personal computers (PCs), autonomous cars, drones, and robots are examples of edge devices.

Qualcomm has been pushing the envelope in product development to capitalize on the fast-growing edge AI market. According to one estimate, the edge AI market could clock a compound annual growth rate (CAGR) of 37% through 2030. In fact, Qualcomm's automotive business suggests it is already making the most of the addressable opportunity in this space.

The chip designer recently announced that it is expanding its relationship with automotive giant Stellantis to deploy its Snapdragon Digital Chassis solutions to support automated driving and other features. Qualcomm's automotive revenue increased 38% year over year in the second quarter of fiscal 2026 (which ended on March 29) to $1.33 billion. The company was sitting on a $45 billion design win pipeline in the automotive business in March this year, indicating that this business could take off nicely in the future as AI adoption in the automotive space increases.

The valuation makes the stock a no-brainer buy

Qualcomm stock has surged by a whopping 62% over the past month. Still, it can be bought at just 25 times trailing earnings. The forward earnings multiple of 22 is quite affordable, and the sales multiple of 5.7 suggests investors are getting a great deal on this AI stock right now.

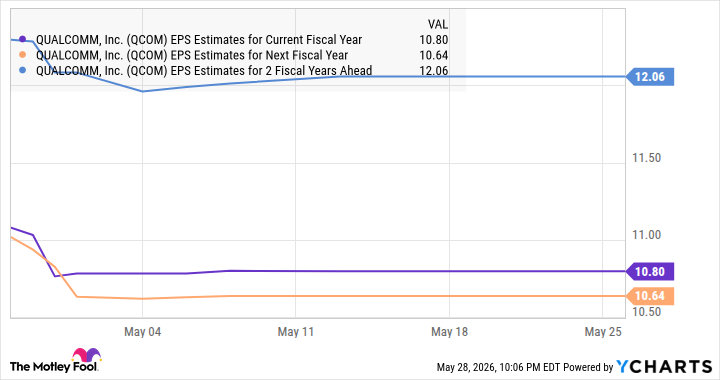

Of course, Qualcomm's top and bottom lines are anticipated to drop in the current fiscal year. However, the addition of AI customers and the healthy growth of the company's automotive business should enable it to return to growth. This is probably why analysts are expecting Qualcomm's earnings growth to accelerate in a couple of years.

Data by YCharts

However, don't be surprised to see this semiconductor stock delivering stronger-than-expected earnings growth as its AI chip business ramps up. That could lead the market to reward Qualcomm with a higher valuation, potentially paving the way for more upside over the long run.