Knight-Swift Transportation (KNX +1.07%) is the largest full truckload carrier in the U.S., and it's always going to be at the center of the never-ending debate over where trucking companies are in the cycle. This week, the bears are winning the debate, with the stock declining by 11.4% through Friday morning, partly driven by a Citi analyst downgrading the stock to neutral from buy, even as the price target was raised to $90 from $72.

The cycle is turning

Demand and pricing power in the trucking industry tend to be highly cyclical, with alternating periods of boom and bust. As ever, this leads investors to try to anticipate when inflection points will occur. The recent Citi downgrade reflects the idea that there's already "elevated optimism" in the stock, as the market has priced in a more positive trucking environment in 2026.

NYSE: KNX

Key Data Points

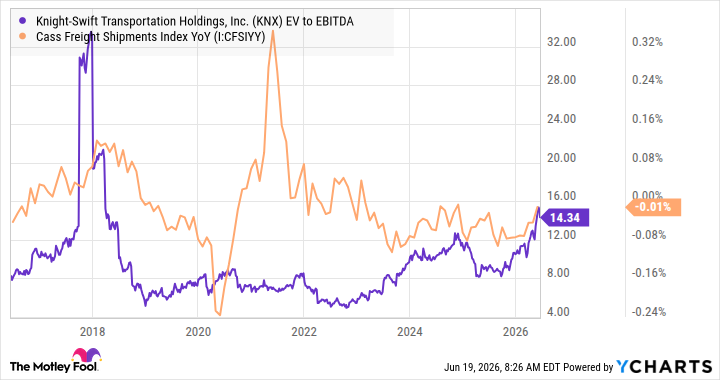

Probably the best dataset to follow on trucking comes from Cass Information Systems, specifically its for-hire freight shipment data across North America. The Cass Freight Index (Shipments) has declined year over year every month since the start of 2023, but has been in positive territory month over month since February of this year. As such, the market is pricing in a return to year-over-year growth.

Image source: Getty Images.

Valuations still matter

A quick look at Knight-Swift's enterprise value (market cap plus net debt) to earnings before interest, taxation, depreciation, and amortization (EBITDA) valuations suggests the analyst might have a point.

KNX EV to EBITDA data by YCharts

Ultimately, the debate will be settled by the strength of the trucking market recovery, but right now Knight-Swift looks priced for a strong recovery. If it doesn't occur, then the current valuation may look a little stretched.