Amazon (AMZN 0.98%) stock has turned into a bit of a bust so far in 2026. The stock is up only around 7% year to date, trailing the S&P 500 (^GSPC +0.89%). However, that wasn't true a few weeks ago, when Amazon reached new all-time highs. Now, it's about down 10% from that peak.

Is this the ultimate buying opportunity for Amazon stock, or should interested investors remain patient?

Image source: The Motley Fool.

E-commerce and cloud infrastructure

The thesis for Amazon really should be looked at as a tale of two business units. First, there is the most obvious: its e-commerce business. This division operates around the globe, enabling customers to order goods online and have them delivered quickly to their doorsteps. While this is the part of Amazon that most people interact with, it's the least exciting from an investment standpoint.

What's far more exciting is Amazon Web Services (AWS). Though smaller on a revenue basis, the cloud computing division actually produces the majority of Amazon's profits -- 59% in Q1. It's also growing far faster: Its revenue rose 28% in Q1 (the best in nearly four years), compared to 19% international commerce growth and 12% North American commerce growth.

AWS is leaning heavily into the artificial intelligence build-out, and is spending the most of any AI hyperscaler this year: $200 billion. CEO Andy Jassy informed investors that it has a lot of clients already lined up for the computing power it's adding, and noted that the faster AWS grows, the more money it must spend to keep up with demand.

NASDAQ: AMZN

Key Data Points

Jassy believes AWS is in a multiyear growth cycle. As new computing power comes online, it will drive huge revenue and profit growth, delivering a monster return on investment that dwarfs the initial costs. If Amazon can deliver on that premise over the next few years, then the stock should prove a profitable holding.

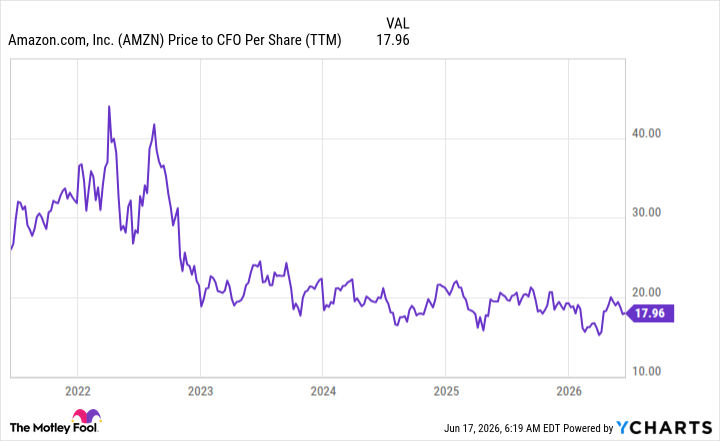

One of the best ways to value a company is to use its operating cash flow, which does not include one-time effects like capital expenditures or gains or losses on investments. By this metric, Amazon is trading at a historically attractive level.

AMZN Price to CFO Per Share (TTM) data by YCharts.

Compared to some of its big tech peers, it also looks quite cheap. Apple trades for 32 times operating cash flow, while Alphabet trades at 26. Microsoft, which operates its own cloud business, is right around Amazon's level at 17 times operating cash flow.

I think that makes Amazon a solid buy today, and now is the perfect opportunity to buy the dip and hold onto it for several years as the revenues from the AI build-out roll in.