If you're an income investor, you most likely will be looking for high-dividend stocks. However, dividend investing also requires patience. And the reason for that is fairly simple: Most high-quality dividend payers are very stable and mature companies whose stocks are almost always trading at fair valuations with little-to-no prospect of becoming undervalued. In other words, these are generally boring stocks to own.

Dedicated income investors, however, will realize that the secret of dividend investing lies in remaining invested over a long period of time -- preferably decades. They understand the power of compounding returns of a steady cash flow stream that can be reinvested back. Which is why patience is a prerequisite.

Notice that the emphasis is on "steady" rather than just high yields that may or may not be sustainable. And even if you're relying on the dividends as an income source now -- as opposed to reinvesting them back into buying more shares -- you'd rather be looking to invest in companies that are steady dividend payers.

When it comes to investing in dividend-paying oil stocks, here's what I'd be looking for:

Financial resilience/balance sheet strength: The oil business is highly capital intensive. Sunk costs are high in this industry. Whether it's drilling a well, buying a new rig, or upgrading a refinery, the initial investment is quite large before returns can flow in.

Naturally, companies need to have a solid balance sheet and some deep pockets. It goes without saying that companies that make initial investments with copious amounts of debt may be skating on thin ice.

A case in point: Seadrill (SDRL +0.00%) suspended its huge dividend (yielding 9.2%) in November 2014 as oil prices began declining. The company's debt-to-equity ratio is a staggering 121%. I see a yellow flag when the ratio exceeds 65%, and a red flag if it exceeds 100%.

Competitive advantage: The dividend payer must be a household name in its own industry. Its business model cannot be replicated easily. Such companies have an economic moat that will sustain them in any bear market. They will be the least affected among peers when oil prices fall; instead, strong fundamentals drive their share prices.

A steady dividend payer with a minimum yield of 3%: While a 30-year dividend-paying history isn't necessary, these companies must be reliable dividend payers. Their dividends must be steady and exhibit consistent growth. In order to achieve that, management must be disciplined in allocation of capital, and also oversee growth at a prudent pace. Additionally, I'd put the cap on dividend yield at no less than 3%.

Keeping these points in mind, here are seven dividend stocks in oil that could go a long way earning you solid returns -- either in your retirement portfolio, or as a current income stream.

ConocoPhillips (COP -0.86%): Currently yielding a solid 4.7%, the world's largest independent exploration and production, or E&P, company continues to impress with its fundamentals, as well as its dividend-paying track record. The Houston-based company has been paying dividends for at least 10 years (according to available data).

Its average annual dividend growth rate for the last 10 years is an impressive 9.2%. Yet its payout ratio for 2014 was only 48%. The secret behind such a compelling dividend is a diverse, low-decline asset base around the globe.

Helmerich & Payne (HP +0.42%): North America's leading onshore drilling contractor yields a solid 3.8%. However, what's more compelling is its 10-year dividend growth rate, which stands at an awesome 30.5% per annum. Yet its payout ratio was a modest 35% for 2014.

The company has a conservatively managed balance sheet with strong liquidity ratios. The current shale oil boom in the United States is the biggest driver for this driller, and it should continue to be so in the foreseeable future.

Source: Helmerich & Payne, Investor Presentation.

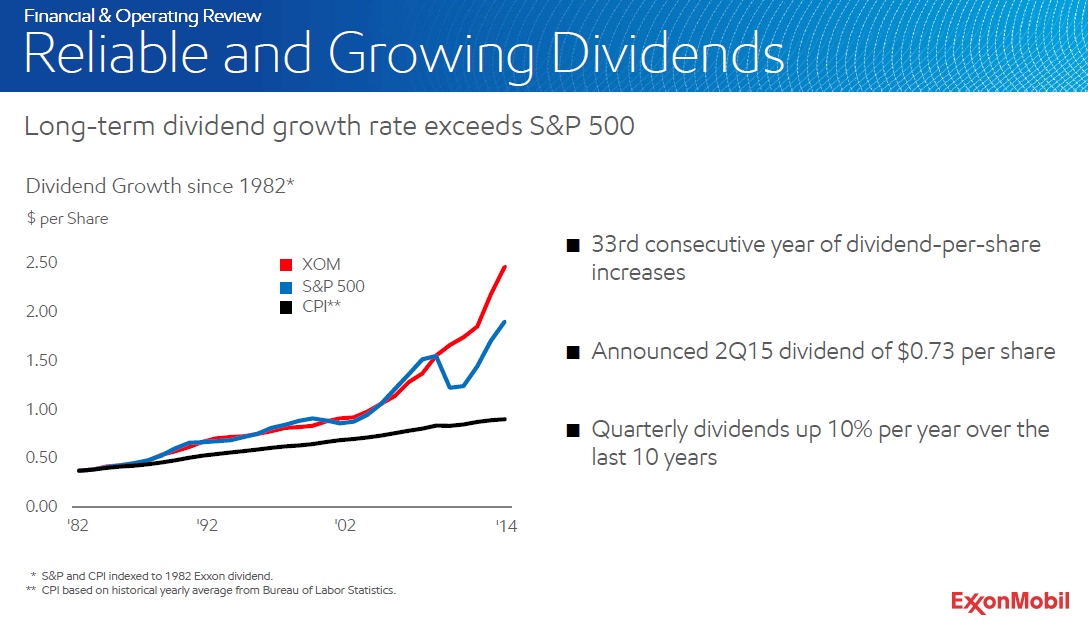

ExxonMobil (XOM -0.28%): Not much introduction needs to be given to the world's largest publicly held integrated oil company. With diverse assets across the globe, whether they be offshore reserves or on land, it's all about steady growth. Exxon follows the old-school principle of hedging volatile commodity prices with a refining and marketing division of its own.

Exxon currently yields 3.4%, and has grown its dividend by an average 9% per annum for the last 10 years. Its debt to equity stands at a modest 11%, while its payout ratio for 2014 was a healthy 33%. The company has been paying steadily growing dividends since 1982.

Source: ExxonMobil, Shareholders' Meeting.

Chevron (CVX -1.13%): Another contemporary of Exxon, this integrated oil company currently yields a solid 4.3%. Its dividend grew an average 9.2% during the last 10 years, and had a payout ratio of just 38% in 2014. Chevron has quite a few projects coming online by 2017 -- notably the Wheatstone and Gorgon LNG projects off Australia. These should mitigate any fears of whether the company is facing any kind of cash flow crunch.

National Oilwell Varco (NOV +2.28%): The equipment services provider has been paying a dividend since 2009 that has grown a whopping 75% per annum. Currently yielding a healthy 3.7%, the company is one of the world's largest independent suppliers for drilling equipment. With a debt to equity of 22% and a payout ratio of 35%, the company maintains a conservative balance sheet.

Occidental Petroleum (OXY -0.62%): One of the largest independent E&Ps in North America, Occidental is a surprise inclusion to my list. Trimming itself to size by spinning off its California resources has been a master stroke. Right now, the company is focusing on its oil-rich Permian properties, and is a class above the rest of the oil producers in that region.

Currently yielding 3.8% on its dividends, the company has also been steadily increasing its dividends during the last 10 years by an average 16% per annum. Management maintains fiscal discipline: The company's payout ratio is 39%, while debt to equity remains at 18%.

Murphy Oil Corporation (MUR -1.29%): Following its spinoff of retailer Murphy USA in 2013, Murphy Oil is focusing solely on E&P activities. Its operations in the Eagle Ford, coupled with offshore Malaysia and the Gulf of Mexico, should drive shareholder value.

Currently yielding 3.3%, Murphy has been increasing its dividend by 12% annually during the last 10 years. It's debt to equity stands at a reasonable 32%.

Source: Murphy Oil Corp, Investor Presentation.

Foolish takeaway

For these companies, returning cash to shareholders is a priority. Moreover, they maintain a tight fiscal discipline and prudent growth rates without raising too much debt. The reason why I'm wary of debt is that, once interest rates start moving north, highly leveraged companies might find the going tough, especially those that perennially rely on debt markets to fund growth.