If you've heard of value investing or Warren Buffett, there's a good possibility you've also heard of Benjamin Graham. He was a writer, teacher, and investor who rose to prominence in the mid-20th century.

His principles, described in two groundbreaking books, established the practice of value investing. Learning about Graham's background and the key tenets of his investment approach can provide investors with useful insights that can help fortify their own investing strategies.

Primary roles

Graduating from Columbia University in 1914, Benjamin Graham started his professional career as an assistant bond salesman at the Wall Street firm Newburger, Henderson & Loeb. In the ensuing years, Graham began developing his research-based investment approach. As he moved up the ranks, he gained a reputation for choosing safe yet profitable assets for his employer.

In 1926, Graham co-founded investment fund Graham-Newman Corp. Two years later, his reported annual income was $600,000, about $10 million today.

After several years of impressive success, Graham felt motivated to share the investing wisdom he had learned in his short time in finance. While he wanted to impart what he had learned in a book, he felt compelled to have some teaching experience under his belt. He applied to be a lecturer at Columbia University in 1928, marking the start of a 28-year career in academia.

Investment style

Graham's investment style was defensive. In his writings, he promotes capital preservation as a priority, with growth being almost secondary. This approach is likely a product of his era. He experienced two of the worst stock market crashes in history in 1907 and 1929.

Preferring stocks that today's investors would describe as high-quality, Graham liked balance sheets with good liquidity, tangible assets, and modest debt levels. He preferred big, mature companies over smaller, nimbler ones. He also favored stable earnings and consistent dividends.

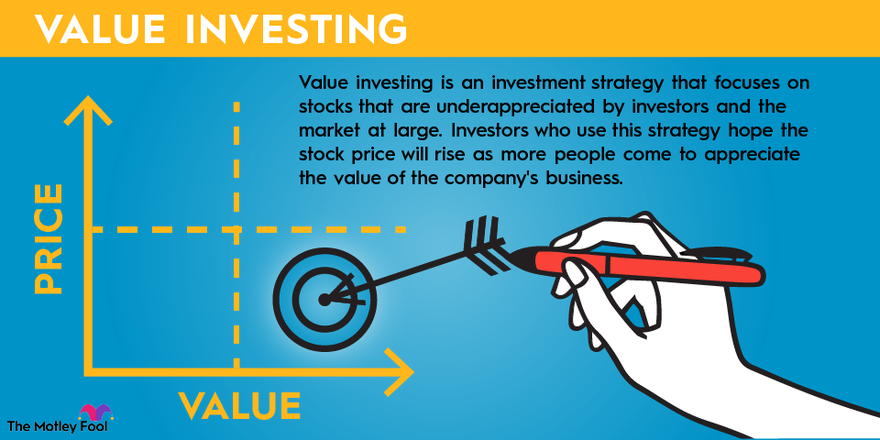

Quality didn't make a good investment on its own, however. Graham specifically sought out quality at a good price. To evaluate a stock's price, he looked at the price-to-earnings (P/E) and price-to-book-value (P/B) ratios.

Offering different strategies for different types of investors, Graham believed that investors short on experience or time should stick to high-quality, established stocks, while more experienced investors should focus on large, financially strong companies that pay dividends and come at a reasonable price.

Career highlights

Achieving early success at Newburger, Henderson & Loeb, Graham was soon made a partner in 1920. But prior to his promotion, Graham demonstrated an enthusiasm for sharing his investing wisdom and insights through writing.

During World War I, Graham submitted an article entitled "Bargains in Bonds" to the Magazine of Wall Street (now known as The Wall Street Journal). The publication appreciated his perspective, and Graham continued to provide frequent contributions to the magazine. Later, Graham authored several books:

- The Intelligent Investor Rev Ed: The Definitive Book on Value Investing, by Benjamin Graham and Jason Zweig

- Security Analysis: Sixth Edition, Foreword by Warren Buffett, by Benjamin Graham and David Dodd

- The Interpretation of Financial Statements, by Benjamin Graham and Spencer B. Meredith

Graham-Newman Corporation remained in business until the 1950s, recovering from the losses incurred during the Great Depression and generating sizable returns for its clients. The company's star investment was a 50% interest in Geico Insurance, purchased in 1948 for about $736,000 -- the same Geico that is today wholly owned by Buffett's Berkshire Hathaway (BRK.A -0.72%) (BRK.B 0.03%).

Philosophy & legacy

One of the most lauded investors of all time, Graham is specifically recognized as one of the greatest value investors. So much so that he has earned monikers like the "Father of Value Investing" and the "Dean of Wall Street."

He distrusted market valuations and growth projections. He preferred to value a stock himself based on the company's tangible assets, debt levels, earnings, and dividends. He would then limit his purchases to stocks that were priced near or (ideally) below his valuation. Investors can use this approach to select assets that are less likely to create big losses.

His books outlining his investment philosophies are still widely read today. Graham was also a mentor to Warren Buffett.

Graham's most recognized rules of investing are to protect yourself from losses and distrust market prices. Loss protection measures include investing with a margin of safety and diversifying across and within asset classes.

Graham's margin of safety concept is closely related to his distrust of market prices. The margin of safety is the difference between the stock's price and what your analysis indicates it's worth.

Awards, honors, and recognition

While Graham didn't receive formal awards or honors, the lack of trophies belies the fact that his status among investors is legendary.

One way his contribution to the investing world is celebrated is through the CFA Institute's Financial Analysts Journal, which created the Graham and Dodd Awards of Excellence in 1960 to honor Graham, along with David Dodd. Dodd, a professor who worked with Graham at the Columbia Business School, co-authored Security Analysis with Graham. The awards are given in recognition of excellence in research and financial writing.

An investment operation is one which, upon thorough analysis, promises safety of principal and a satisfactory return. Operations not meeting these requirements are speculative.

Related investing topics

Personal notes

A self-made man, Graham and his family moved from London to the United States in the 1890s and fell into poverty in the early 1900s. Graham worked odd jobs as a child and secured a scholarship to pay for his tuition when he attended Columbia University.

Graham was married three times -- to Hazel Mazur, Carol Wood, and Estelle Messing. All three unions failed, though Graham and his third wife never officially divorced. He had six children.

About the Author