SEP IRA eligibility rules

If you work for a company that offers a SEP IRA, your employer must make the same contribution, as a percentage of salary, to your SEP IRA and the SEP IRAs of every other eligible employee. You are eligible to receive SEP IRA contributions from your employer, provided you meet the following criteria:

- You're at least 21 years of age.

- You meet the 3-of-5 rule, which means you've worked for the company for any amount of time -- even just seasonally for a couple of months -- during at least three of the past five years.

If you do not meet these requirements, your employer can still choose to contribute to a SEP IRA on your behalf, provided that the employer's less-restrictive policies are applied equally to all employees and also to the employer.

Employers can contribute to SEP IRAs for employees younger than age 21, who do not satisfy the 3-of-5 rule, or who earn less than the threshold dollar amounts. The only requirement is that the same eligibility rules apply to everyone equally.

An employer cannot adopt eligibility rules that are more restrictive than the criteria above, even if the rules are applied equally to every person in the organization.

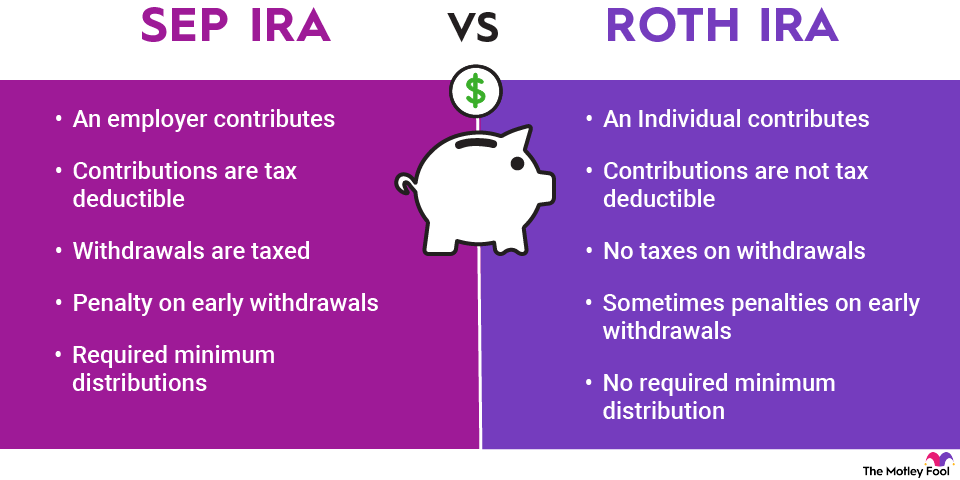

SEP IRA withdrawal and distribution rules

Most SEP IRAs are tax-deferred accounts, meaning that -- as with a traditional IRA -- contributions are made with pre-tax dollars and withdrawals are taxed as ordinary income. If you withdraw money from your SEP IRA before you reach age 59 1/2, you are likely obligated to pay a 10% penalty on the amount withdrawn.

If you leave your employer for any reason, you can roll your SEP IRA into another tax-advantaged retirement savings account, such as a traditional IRA, a 401(k), or a 403(b). While it's also possible to roll the money into a Roth IRA, moving the funds from a SEP IRA holding pre-tax dollars to one that accepts only post-tax contributions requires you to pay income tax on the transferred money in the year the rollover occurs.

However, it is worth noting that the SECURE Act 2.0, which was passed at the end of December 2022, created a Roth SEP IRA effective in 2023. A Roth SEP IRA allows you to contribute with after-tax dollars and defer your tax savings until retirement, just as a Roth 401(k) and Roth IRA offer.

Regardless of whether you have a traditional or Roth account, you cannot borrow money from your SEP IRA. And you must accept annual required minimum distributions (RMDs) once you reach age 73 unless you have a Roth account.

If you are eligible to contribute directly to a SEP IRA, which you can do only if you are the employer or are self-employed, then you can claim the contributions as tax deductions. If you're not the employer or self-employed, then you cannot deduct the contributions to your SEP IRA from your taxable income.

Having a SEP IRA doesn't affect your eligibility to fund a Roth IRA or a traditional IRA. Even if you are fortunate enough to have an employer-funded SEP IRA, it's still important to independently save for your own retirement. Owning both a SEP IRA and another account you fund on your own is a surefire strategy to maximize your retirement savings.

Related Retirement Topics