If it weren't for one small, eensy-weensy, tiny detail, PayPal Holdings Inc. (PYPL -0.85%) would be basking in the glow of another wonderful quarter. After all, when the online payment platform reported its fourth-quarter earnings in late January, the numbers all looked great. Net revenue grew to $3.74 billion, a 26% increase year over year, while non-GAAP earnings per share rose to $0.55, a 30% increase year over year. The strong top- and bottom-line growth during the quarter was driven by a 15% increase in active customer accounts to 227 million and a 25% increase in the number of payment transactions to 2.2 billion.

Yet none of the analysts' questions in the conference call following the earnings release centered on increasing customer engagement levels, revenue growth, or a rise in earnings. Not one analyst asked a question about Venmo, the popular social payments app that saw total payment volume spike to $10.4 billion, a whopping 86% increase year over year. Analysts didn't even ask how Venmo's nationwide rollout as a method of payment at merchants was progressing. No, analysts didn't ask questions about any of these things.

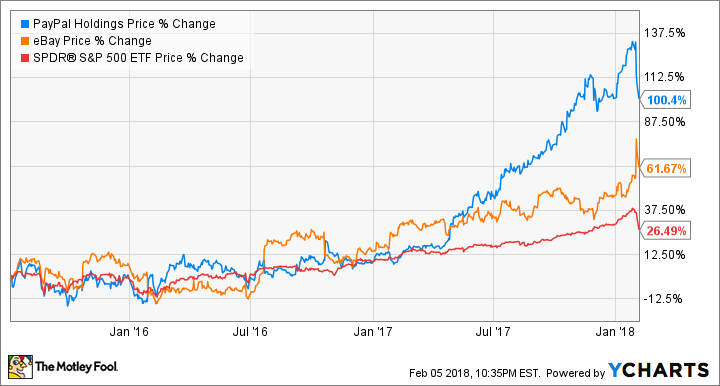

Should PayPal investors be worried eBay will not be renewing its payment processing deal with PayPal? Image source: PayPal Holdings Inc.

Rather, every single question centered on the announcement that eBay Inc. (EBAY -3.58%) will be terminating its relationship with PayPal at the conclusion of their separation agreement in the summer of 2020. Since analysts took PayPal's entire Q&A session and most of eBay's to ask about how this arrangement would affect the businesses, I thought it might be prudent to review everything we know about the existing deal and how each company is now guiding for its future.

The separation papers

In the summer of 2015, eBay spun off PayPal after a fruitful 13-year relationship as a combined entity. Those who argued for the separation can take a bow. Since the two companies went their separate ways two and a half years ago, both have trounced the market: PayPal is up 100%, eBay 62%, and the S&P 500 index about 26%.

When the two companies parted, certain steps were taken to ensure business could continue as usual for eBay and that PayPal would have time to get on its feet while learning how to survive in the wild. Hence, both companies signed a five-year operating agreement. The deal designated PayPal as the payment platform on which all transactions across eBay's marketplace would be processed. This doesn't mean PayPal would be the payment method chosen for every single transaction, but that the company would handle the back-office processing of payments, as it does for Uber and Airbnb. The agreement also allowed for PayPal to be a method of payment for consumers purchasing products on eBay during the same time period.

This agreement is still intact, and nothing changes for either company until the existing agreement expires in July 2020. In fact, PayPal and eBay extended their consumer-facing brand agreement for three years, which essentially means PayPal will be allowed to serve as a payment button on eBay's site through July 2023.

Bad news first

Payment volume associated with eBay represented 13% of total payment volume this quarter. While PayPal management didn't give any color during the conference call on how much revenue or income that represented, CFO John Rainey let this slip at the Deutsche Bank Technology Conference last fall: "In 2016, our overall payment volume that was on eBay was ... 17% of our overall payment volume, 22% was revenue, all right? If you look at the rate of decline in those numbers, they have been declining at a commensurate rate of about 300 to 400 basis points per year."

While eBay payment volume is significantly decreasing as an overall percentage of payment volume, it is still a significant amount of business to be losing.

The silver lining

While 13% of payment volume is coming from eBay, that number is steadily decreasing. CEO Dan Schulman said in the conference call that if eBay's business declines on a similar rate as it has for the past two and a half years, eBay transactions will be considerably less by the time the deal actually expires. He added:

So today, eBay ... is about 13% of our TPV, our total process volume -- transaction process volume, and that's down about 900 basis points in the last 2.5 years. So let's just assume that exactly the same thing happens over the next 2.5 years, and that we have no acquisitions or such, which, by the way, as you know, we are acquisitive, we're aggressive on that. ... But assuming no acquisition, eBay becomes approximately, at the end of the operating agreement, about 4% of our TPV. That's assuming, again, the same amount, first 2.5 years with the second 2.5 years, and maybe less than 10% of our revenues.

While a significant hit, that's also far from a doomsday scenario. But wait: The news gets better for PayPal shareholders. By keeping the consumer-facing branded method of payment on eBay, PayPal is keeping the most profitable and important piece of the pie. As Schulman said, it is "far and away the most profitable element of the relationship" and "the most important to our mutual customers." The unbranded, backend processing is largely a commoditized business, with high costs and low margins. For instance, Rainey said the eBay processing business generates a disproportionate amount of losses and calls to PayPal's customer service center.

eBay comprises less and less of PayPal's payment volume every year. Image source: eBay Inc.

PayPal also firmly states that this loss was always booked into its medium-term guidance and that the company believes it can still hit all the growth targets it has given in the past. After a pointed question from an analyst, management even clarified that it could hit its targets without severe cost-cutting measures or an inordinate amount of share buybacks.

Finally, when the separation deal expires, PayPal will be allowed to pursue other deals that it's currently prohibited from pursuing. The separation deal expressly prohibited PayPal from working with specific eBay competitors. While no companies were named, Schulman described these other companies as "the largest and fastest-growing marketplaces in the world." That is largely assumed to mean PayPal is currently forbidden from working with Amazon.com, which would explain the curious omission of PayPal as a method of payment on Amazon's site.

The Foolish takeaway

No matter how you spin it, this is not good news for PayPal. While I don't know how long these storm clouds will hang over PayPal's countenance, the stock has already fallen about 11% from its highs and could easily fall more. Going into its earnings, PayPal's stock was practically priced for perfection, with a P/E ratio of about 48; it's still steep but has fallen below 40, in part because of the market's dramatic pullback in recent days.

In some respects, it reminds me of when the American Express Company lost the co-brand credit card business of Costco Wholesale in 2016. American Express shareholders were left wandering in the wilderness, for what seemed like an eternity, after the company lost over a third of its market cap at its bottom.

However, the good news is that, like American Express, PayPal's long-term thesis is still intact. After all, I don't recall too many analysts pounding the table and recommending PayPal based on its existing business with eBay. No, PayPal is riding huge tailwinds as one of the obvious winners of e-commerce and mobile commerce. That hasn't changed. PayPal announced it would be losing a decent chunk of business in two and a half years, but it didn't change the story. Storm clouds are overhead, but the sun is peeking through on the distant horizon. While I don't know how painful it will get for shareholders in the interim, I believe patience will ultimately be rewarded.