While superinvestor Warren Buffett is known for having said his "preferred holding period is forever," that's not always a reasonable expectation for individual investors. At some point, you may sell even your best stocks to pay bills in retirement, put a kid through college, or just reward yourself for decades of patient investing success.

But dividend stocks can actually make for perfect "hold forever" investments, especially if they pay a higher yield and have given you years and years of dividend growth. If you own enough of the right ones for long enough, you may never have to sell a share, deriving enough income from the payout to more than meet your financial needs.

We asked three Motley Fool contributors who know a thing or two about high-yield stocks to help identify three that have the prospects to be "hold forever" investments, and they came back with Caretrust REIT Inc (CTRE +2.13%), Brookfield Renewable Partners LP (BEP +0.15%), and General Motors Company (GM +2.44%). Not only do they all meet the "high-yield" watermark, with yields ranging from 4% to 6.3% at recent prices, but they're also incredibly well-run businesses with strong balance sheets and strong competitive advantages.

Image source: Getty Images.

Two characteristics make this a "hold forever" dividend stock

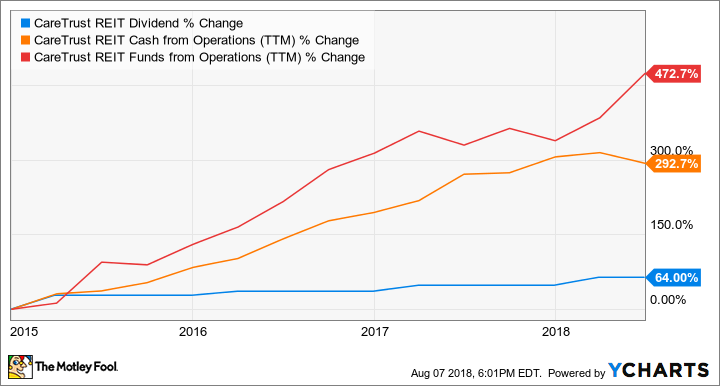

Jason Hall (Caretrust REIT): There are two "must-have" characteristics dividend investors should require in their hold-forever stocks: excellent capital allocation, and a clear plan to capture dependable cash flows. Real estate investment trust Caretrust REIT checks both of those boxes.

Caretrust's focus on senior housing is supported by a major trend. There will be 80 million Americans over 65, with about half of them 80 or older, in just over a decade. That's double 2010 levels, and there will need to be far more healthcare and housing properties to support this increased number of seniors, even as improvements in healthcare allow more to live independently for longer.

Since Caretrust went public in 2014, management has done a wonderful job of allocating capital to growth, primarily through acquisitions. Since late 2014, cash flows and funds from operations have skyrocketed, allowing for big growth in the dividend:

CTRE Dividend data by YCharts

Management deserves ample credit for generating solid per-share growth, and recent developments indicate this trend should continue over the long term. In recent quarters, Caretrust's acquisitions have slowed as the company has focused on improving operations and waiting out a period of higher prices on the M&A front. CEO Greg Stapley has made it clear that while his preference is to make acquisitions, he will wait out an overheated market "when necessary, and hold on for good assets, fair pricing, and, especially, the right operators."

This combination of long-term opportunity and incredible discipline should continue to pay off for decades to come, and a 4.6% yield makes it much easier to wait out the periods when growth slows.

The top renewable energy dividend play

Travis Hoium (Brookfield Renewable Partners): There's no such thing as a no-risk dividend stock, but Brookfield Renewable Partners is about as close as it gets. The company owns 16,300 megawatts of renewable-energy assets around the world that generate and sell electricity to utilities, often in long-term contracts. Eighty-two percent of the company's portfolio is hydroelectric power plants, but it's adding wind and solar now that those energy sources are competitive with traditional sources of power.

What I like about Brookfield Renewable Partners is that the company doesn't rely on selling stock to fund growth projects, like most yieldcos. The company aims to pay out 70% of funds from operations to shareholders in the form of a dividend, keeping the rest to acquire growth projects. This allows management to target 5% to 9% in annual dividend growth.

BEP Dividend data by YCharts

Riding the renewable-energy wave is going to be good for a lot of companies, but Brookfield Renewable Partners is set up to succeed even if the market turns against renewables (which we've seen a time or two). Management can patiently wait to acquire undervalued assets with excess cash from the business, rather than relying on the volatile stock market to help fund growth. And with a 6.3% dividend yield and growth expected for the foreseeable future, this is a high-yield stock to hold forever.

Business is good

Daniel Miller (General Motors): Business is good for General Motors, as it is for much of the automotive industry, with a fresh portfolio of SUVs and trucks. The trend toward more profitable SUVs and trucks continues with no end in sight, and passenger cars have only accounted for roughly 33% of total light-vehicle sales in the U.S. through June. In fact, the surging SUV and truck sales have pushed GM's average transaction prices $300 higher from the prior year, to a $35,500 second-quarter record. But the cyclical and often unpredictable nature of the automotive industry is why investors would want to hold this 3.8% dividend yield stock forever, through all the ups and downs.

Another reason investors should want to hold forever is GM's long-term game plan for driverless vehicles, which Intel predicts will evolve into a $7 trillion annual revenue stream. GM has taken a huge step forward into becoming a leader in this space and has left its Detroit competitors behind, for now. GM's driverless ambitions started in 2016 with its Cruise Automation acquisition, which has since blossomed into a valuable entity for GM. Softbank Group's agreement to invest $2.25 billion into GM Cruise values it at $11.5 billion.

GM Total Return Price data by YCharts

While the driverless-vehicle end-game is decades away, GM has announced a $100 million investment to upgrade to Michigan plants to produce self-driving vehicles at scale next year. If that program goes well, it could send the value of GM Cruise through the roof and prove that at least one Detroit automaker will be ready to compete as the driverless future develops. For investors, holding this 4.1%-yielding stock forever helps offset the cyclical nature of the automotive industry, and if Detroit's largest automaker becomes a leader in driverless vehicles over the coming decades, it'll certainly be a stock you will want to continue holding.