Spring is in the air, baseball season is underway, and long overdue summer vacations are just around the corner. Things are looking up in the real world, and the U.S. stock market reached a new all-time high on Friday.

With vaccine distribution kicking into high gear, there's also an end in sight for the COVID-19 pandemic. For investors looking to take profits and raise cash, now may be a good time to shift away from growth stocks and into value stocks. The Walt Disney Company (DIS +0.07%), Clorox (CLX +0.17%), and United Parcel Service (UPS +1.84%) are three top value stocks that are worth considering now.

Image source: Getty Images.

A different class of value

Last year wasn't a good year for most value stocks. Vanguard, which operates the largest growth and value exchange-traded funds (ETFs) on the market, saw its leading value ETF produce a total return of just 2.3% compared to a 40% total return for its leading growth ETF.

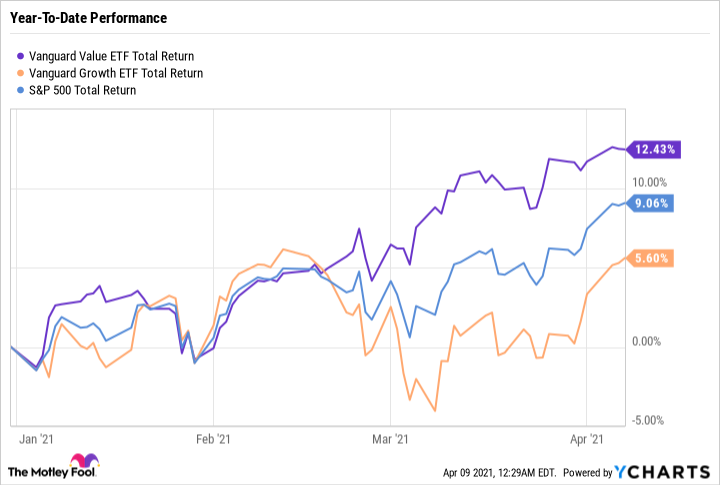

VTV Total Return Level data by YCharts

Value stocks are often thought of as "cigar butt companies" -- so cheap that their assets may be worth more than the enterprise value of the company itself. However, the best value stocks are ones that have a track record of earnings and dividend growth. In fact, the top 10 holdings in the Vanguard Value ETF (VTV +0.13%) are all leading Fortune 100 companies in different industries.

Value stocks are making a comeback this year. Acting as the leaders instead of the laggards, they are spearheading this year's market rally and even outperforming growth stocks.

VTV Total Return Level data by YCharts

1. Disney

Disney is the fourth-largest holding in the Vanguard Value ETF, and one of the surprising value stocks that reached an all-time high in 2020. Despite a collapse in park and studio entertainment revenue, Disney is the perfect example of a company crippled by the pandemic whose prospects (thanks to streaming service Disney+) have led investors to believe it is more valuable now than before COVID-19.

Over 80 years of content gave Disney a big advantage when starting Disney+. Launched in November 2019, Disney+ finished 2019 with a respectable 26.5 million paid subscribers. After a surge in at-home entertainment due to the pandemic, Disney+ finished 2020 with 94.9 million paid subscribers (146.4 million if you include Hulu and ESPN+). For comparison, Netflix (NFLX +0.31%) ended 2020 with 204 million global subscribers.

In its 2020 investor presentation, Disney announced bold plans to reach $14 billion to $16 billion in annual streaming spending by fiscal year (FY) 2024. It also projected 230 million to 260 million paid subscribers by FY 2024. Netflix had total spending of $17.6 billion in 2020, the vast majority of which went toward content development.

Disney is currently priced around an all-time high. It may take a couple of years to return to its 2019 net income -- and reinstate the dividend for that matter -- but the added strength of Disney+ makes this a great value stock to hold for the next 10 years.

2. Clorox

From center stage stardom to a supporting role, Clorox is a traditional consumer staple stock that found itself caught in the middle of the COVID-19 pandemic. With its disinfecting wipes flying off shelves last spring, Clorox was one of the few stocks that performed well while the market crashed. Shares soared over 55% between the start of 2020 and their peak on Aug. 7. As a steady player that tends to post mid-single-digit growth numbers, Clorox's share price arguably got ahead of itself. But it's now down roughly 20% since that high last August, and it's starting to look like a good value.

Clorox is a proven and profitable business, and one of the few value stocks that had record revenue and net income in 2020. It will face difficult comps in 2021 as its earnings lap its strongest quarters in history. However, there are plenty of reasons why Clorox could continue to grow in the coming years.

CLX Revenue (TTM) data by YCharts

Since taking over as CEO in September 2020, 43-year-old Linda Rendle has made it clear Clorox is well-positioned for a post-pandemic world. She believes that habits and behaviors developed because of the pandemic are sticky and that investing in marketing and advertising is a great way to tap into those trends. Last year, Clorox spent 23.5% more on sales, general, and administrative (SG&A) expenses and 26.3% more on advertising than in 2020. Clorox has aggressively targeted advertising partnerships, like its recently minted multi-year deal with the NBA. With a P/E ratio of 20, over 40 consecutive years of dividend raises, and a 2.3% dividend yield, Clorox is an excellent value stock to buy right now.

3. UPS

Like Clorox, UPS is coming off its best year ever. Its $24.9 billion in revenue and $8.23 in adjusted diluted EPS were both record highs as the transportation stock leaned into residential package delivery. Its biggest headwind was business-to-business (B2B) deliveries. These higher-margin, lower-volume deliveries declined in 2020 but began picking up toward the end of the year. That's great news for UPS, which aims to keep as much of the added residential business as possible while recovering B2B sales.

UPS ramped up spending in recent years to accommodate a growing e-commerce business. With much of that ramp-up complete, the company plans to reduce capital expenditures to just $4 billion in 2021, the lowest level since 2016. This should help UPS's profitability in the event that sales decline.

UPS's 2020 e-commerce growth was no accident. The buildout was planned before the pandemic, and just so happened to be timely. UPS hopes to retain much of the e-commerce and international growth it experienced in 2020. Management believes that the company is in the beginning innings of a long-term e-commerce boom. With a dividend yield of 2.3% and plans to grow its top and bottom lines even further, UPS is a top-tier value stock to watch in the coming years.