If you are a dividend investor looking to maximize the income your portfolio generates, you will want to do a deep dive on Universal Health Realty Income Trust (UHT +2.07%). It has a historically high 7.4% dividend yield and a great track record of dividend growth to back it up. The dividend stock won't be right for every income investor, but for a select few it could be the smartest dividend stock to buy right now.

What makes a dividend stock attractive?

One of the first things that income investors look for is dividend yield. Universal Health Realty Income Trust has that factor pegged, with a huge 7.4% dividend yield. But some reference points will help.

Image source: Getty Images.

The S&P 500 (^GSPC 0.13%) has an itty bitty yield of 1.3%. The average healthcare stock has a yield of 1.8%. And the average real estate investment trust (REIT) has a yield of roughly 4.1%. Very clearly, Universal Health Realty is more attractive on the yield front.

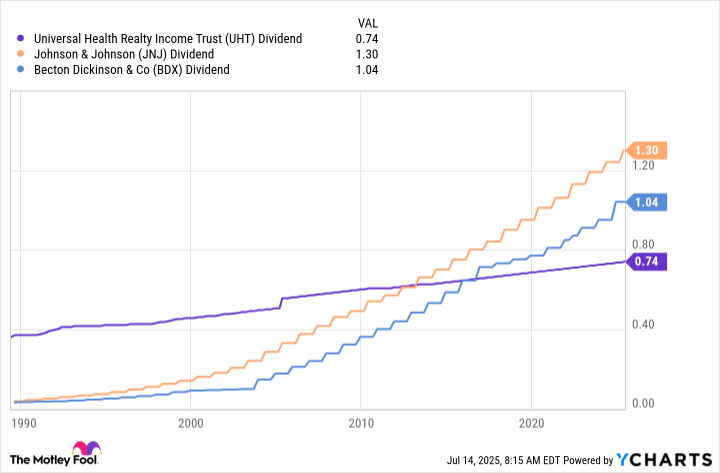

But yield has to be considered along with reliability. For example, one of the most reliable dividend-paying healthcare stocks is Johnson & Johnson (JNJ 0.19%), with 63 years of annual dividend hikes behind it. Next up is Becton, Dickinson (BDX 0.29%), with 53 years of hikes. Those two companies are Dividend Kings, an elite status that Universal Health Realty simply can't claim. That said, Johnson & Johnson's yield is 3.4% and Becton, Dickinson's yield is an even smaller 2.4%.

Universal Health Realty's dividend has been hiked annually for four decades. That's a pretty good streak, even though it isn't yet a Dividend King, when you add in the real estate investment trust's huge yield. A $1,000 investment will get you around 24 shares of the healthcare-focused REIT.

Data by YCharts.

Universal Health Realty Trust is for income right now

So a lofty yield and a strong dividend history make Universal Health Realty Trust attractive. It is extra attractive right now because the yield is near the highest levels of the past decade, suggesting the stock is on the sale rack. But there's just one small problem: Dividend growth has never been a big selling point here.

As the chart above highlights, both JNJ's and Becton, Dickinson's dividend growth has been far superior to that of Universal Health Realty Trust. The goal for Universal Health Realty Trust isn't rapid dividend growth, it is reliable growth. It is a slow and steady tortoise, and that is likely all it will ever be.

NYSE: UHT

Key Data Points

And that brings up the second big issue that investors need to know about. Universal Health Realty Trust is externally managed by Universal Health Services (UHS 1.42%), the REIT's largest tenant. There are very clear issues with conflicts of interest that have to be considered. However, the 40-year track record of slow and steady dividend growth is an indication of what Universal Health Services is doing here.

More attractive than it was, not for all, but smart for some

The interesting thing here is that prior to the coronavirus pandemic, Universal Health Realty's dividend yield was a tiny 2.1% or so. At that point, investors were way too optimistic about the REIT given the tortoise-like nature of the dividend. But, today, with the yield at 7.4%, this healthcare stock is a lot more attractive.

It won't be right for every dividend investor, given the management structure and that tortoise-like dividend growth. For dividend growth investors, JNJ or Becton, Dickinson will be more appropriate. However, if you are trying to maximize the income you generate from your portfolio today and you are looking for a healthcare investment, Universal Health Realty Trust could be perfect for your portfolio if you have $1,000 or $10,000 to invest.