The data centers, chips, and components used to develop artificial intelligence (AI) are exceptional at parallel processing, meaning they can complete multiple tasks simultaneously. However, those tasks tend to be quite simple, like identifying patterns in large datasets. Quantum computers, on the other hand, use a concept called superposition to simulate many different solutions to a problem at once, which can speed up highly complex workloads.

Therefore, quantum computers aren't necessarily better than traditional computers, they are just more effective at specific tasks. They could lead to significant breakthroughs in areas like science and cryptography, creating a substantial financial opportunity for quantum computing companies like Rigetti Computing (RGTI +3.62%).

Investors have sent Rigetti stock soaring by 4,800% over the past year alone as they try to position their portfolios for the quantum revolution. But is it too late to buy?

Image source: Getty Images.

An early leader in quantum computing

Rigetti is a unique player in the quantum space because it develops all of its hardware and software in-house. It owns a fabrication facility, it designed its own quantum programming language called Quil, and it even built a cloud computing platform that allows businesses to rent quantum computing capacity for a fee.

By owning the entire supply chain, Rigetti can bring updates to market significantly faster than its competitors, and it has released several generations of chips, processors, and systems since it was founded in 2013. Its new Cepheus-1-36Q is the industry's largest multi-chip quantum computer, and it has achieved an incredibly high fidelity of 99.5%.

Traditional computers use bits, which are easily read because they are always in a state of either 0 or 1. Quantum computers use qubits, which can assume the position of both 0 and 1 at the same time (which is the crux of the superposition concept mentioned earlier). Fidelity measures the accuracy of each quantum operation, so a higher result means fewer errors, making the quantum computer more useful for solving real-world problems.

Cepheus-1-36Q is now available through the Rigetti Quantum Cloud Services platform, but it's also available on Microsoft's Azure Quantum cloud platform, which could significantly accelerate adoption rates.

NASDAQ: RGTI

Key Data Points

Rigetti's progress isn't showing up in its financial results

Commercializing a new technology is never easy. It often requires substantial capital expenditures, with little clarity on when it will start generating consistent revenue. Quantum computing is certainly no exception.

Rigetti generated just $1.8 million in revenue during the second quarter of 2025 (ended June 30), which was a 41% decline from the year-ago period. At the same time, its operating costs grew by 13% to $20.4 million. With less money coming in and more money going out, it's no surprise the company's net loss surged by 219% to $39.6 million on a generally accepted accounting principles (GAAP) basis.

Rigetti had around $571.6 million in cash, equivalents, and short-term investments on hand as of June 30, following a $350 million capital raise that closed during the second quarter. Therefore, the company has enough cushion to sustain its current losses for the next couple of years, but if it doesn't start bringing in meaningful revenue soon, it will struggle to find a path to profitability.

In that case, Rigetti will have to raise more money, which will further dilute existing shareholders.

Is it too late to buy Rigetti stock?

Rigetti has a market capitalization of $15 billion as I write this, which is a massive number relative to the company's minuscule revenue. Its pipeline is also quite small, which makes its valuation even harder to justify -- in September, the company signed a $5.7 million sales contract that is expected to turn into revenue during the first half of 2026, and it also signed a deal with the U.S. Air Force for $5.8 million, which will be recognized over three years.

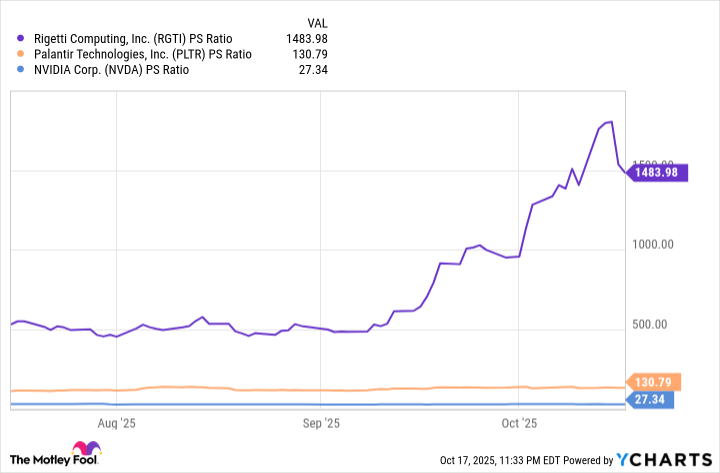

As a result, Rigetti stock trades at a ludicrous price-to-sales (P/S) ratio of 1,480. For some perspective, Nvidia trades at a P/S ratio of just 27. Rigetti even makes Palantir Technologies' P/S ratio of 130 look like a bargain, even though it is also wildly expensive in its own right.

Data by YCharts.

Rigetti is doing extremely well to compete with trillion-dollar giants like Alphabet in the quantum computing space, and the technology is unquestionably exciting. But managing risk is a critical part of investing, and paying a sky-high valuation for a company with minimal revenue and mounting losses opens the door to significant potential downside. I'm not suggesting this will happen, but Rigetti stock would have to plunge by 91% just for its P/S ratio to match Palantir's P/S ratio -- and it would still be considered expensive.

As a result, unless Rigetti stock suffers a sharp correction, it might be too late for investors to board this train. But the quantum computing industry is likely to produce many opportunities over the long term, so patience might be key to capturing the next hypergrowth story.