Don't look now, but Sandisk (SNDK 5.88%) is the hottest stock in the S&P 500. Today's youth may be unaware that this company pioneered solid-state memory in the 1990s and went public over 30 years ago. It was later acquired in 2015 and spun out again in 2025 at just a $5 billion market cap.

Roughly 30 years, and it was still only worth $5 billion. Three decades of going basically nowhere.

Image source: Getty Images.

Sandisk is certainly going places now. It was included in the S&P 500 index after going public the most recent time, and it was the top-performing stock in the index in 2025. It's on pace to take the crown again in 2026, considering it's already more than doubled year to date, as of market close Jan. 21.

NASDAQ: SNDK

Key Data Points

Was Sandisk stock an obvious buy when it was spun off from Western Digital in February 2025? No, not necessarily. Is it an obvious sell now that it's doubled in value in less than one month? No. To the contrary, I believe Sandisk stock is simply a great reminder that investing is hard.

What's so hard about investing in stocks?

Warren Buffett championed the idea of intrinsic value -- what a company is actually worth. For Buffett, intrinsic value could be calculated only by estimating a business's future cash flows. Doing this calculation allows investors to buy stocks at prices below their intrinsic value, virtually guaranteeing success.

Herein lies the challenge of investing: Nobody can predict the future. This makes it extremely hard to calculate future cash flows. And this is why nothing about Sandisk stock is obvious right now; it's hard to predict just how high its cash flows will rise.

It's similar to what happened with Nvidia stock in late 2021. The stock had climbed about 1,000% in the previous five years and traded at an incredibly expensive 100 times earnings. However, Nvidia stock has nevertheless climbed another 500% since then because its earnings have skyrocketed thanks to unprecedented demand from AI infrastructure players.

While we can't predict the future, Sandisk's future cash flows should be markedly higher than today because demand for its solid-state memory products is exploding higher. Inference is the latest wave of AI innovation; AI makes autonomous decisions in new situations based on training data. But this is memory-intensive. This leads Sandisk's management to believe that total shipped memory capacity will more than double from the end of 2025 to the end of 2029.

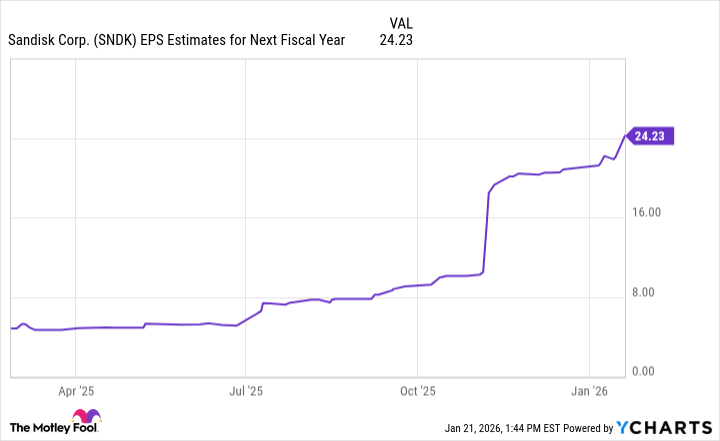

Demand is outpacing the supply from Sandisk and others. This is driving the price of memory products up to unprecedented levels, boosting profit margins. How high can profits go? It's unclear. Even professional analysts on Wall Street are scrambling, regularly increasing their estimates for Sandisk, as the chart below shows.

SNDK EPS Estimates for Next Fiscal Year data by YCharts

The takeaway for investors today is that, while we may not be able to predict the future perfectly, we can still make reasonable assumptions about the future and invest in high-quality businesses poised to benefit. Some of those assumptions will be wrong -- that's the hard part. But when investors rightly pick a winner, holding on for the long term can offset many mistakes.