Tobacco giant Altria (MO +0.35%) has been struggling to generate much growth in recent years. As fewer people smoke, the company has been pivoting to other, less harmful products for consumers. It's been a challenging journey for the company, and there's no denying that smokeable tobacco is still its core business, and it's going to remain that way for the foreseeable future.

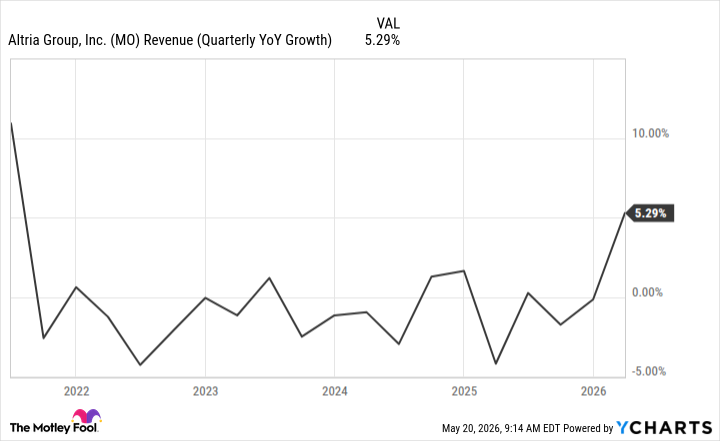

When the company recently reported earnings, there was a positive surprise for investors, or so it seemed anyway. Sales were up 5% from the same period compared to a year ago. That's not the type of growth investors have been accustomed to seeing from the company. But when looking at the bigger picture, the results look far less exciting.

Image source: Getty Images.

Altria's numbers were up, but they were also going up against some weaker comparables

When a business is in decline, it may be easier to show growth even if the numbers aren't necessarily higher than they were a few years ago. And that's exactly the case with Altria. On a year-over-year basis, sales (net of excise taxes) were up over 5% in its most recent quarter -- the best rate the tobacco company has achieved in multiple years.

MO Revenue (Quarterly YoY Growth) data by YCharts

Its revenue during the first three months of the year, when excluding excise taxes, totaled $4.1 billion. Five years earlier, however, that figure stood at nearly $4.9 billion. Its revenue has actually declined by approximately 16% over that time frame.

While there has been some growth in its oral tobacco products over the past five years, it's not anything to get terribly excited about. From $626 million in net revenue back in the first quarter of 2021 to $669 million this past quarter, that's an increase of just under 7%. It's modest, and it still means that it's a small fraction of the overall business.

NYSE: MO

Key Data Points

Why I wouldn't buy into the stock's rally

It's surprising that Altria's stock has been rising in value this year and is even beating the market. However, the bullishness may be due to a combination of the stock's low valuation (it trades at about 13 times its projected future earnings) and its dividend, which yields 5.7%.

But those aren't great reasons for investing in the company. If its numbers deteriorate amid its decline, the valuation may suddenly look worse, and there may inevitably be pressure on the payout as well. If the business isn't growing and it needs to invest in new opportunities, a reduction in the dividend may be a possibility down the road.

All in all, while the stock has been doing well this year, I wouldn't expect the rally to end up lasting. With some serious concerns about the company's long-term future, I think the safest option is to stay away from Altria's stock.