Most investors are aware that China’s automotive market, especially the electric vehicle (EV) industry, is in a brutal price war. The EV industry is crowded with competitors, putting pressure on prices and margins, with uncertainty as to when the spiral lower will end.

Currently, many Chinese automakers are rushing to export vehicles outside of China to support growth, and that’s worked well for most. Nio (NIO +2.26%), however, is hanging tough in its domestic market, and its financials appear to be turning the corner.

But does that make the stock a buy, finally?

Results speak loudly

Let’s briefly point out some of the metrics that made Nio’s 2026 first quarter impressive. Despite the ultra-competitive Chinese automotive market, Nio’s vehicle deliveries totaled 83,465 in Q1, up 98.3% from the prior year. Better yet, despite the ongoing price war, Nio’s discipline enabled the company’s vehicle sales to increase 129.2% to 22,783 million yuan (about $3.3 billion) during the same time frame. The accelerated growth in sales revenue relative to deliveries suggests the company’s pricing power remains strong amid a domestic price war.

Image source: Nio.

It wasn’t just Nio’s top line that was impressive, as vehicle margin checked in at nearly 19% during Q1, well ahead of the 10.2% during the prior-year’s Q1. Nio’s accelerating deliveries, top-line revenue, and vehicle margin helped drive its overall gross margin to 19% during Q1, compared to a much more modest 7.6% during 2025's first quarter.

It all came together at the bottom line, showing that perhaps Nio’s metrics have finally gotten over the hump. When excluding share-based compensation expenses, adjusted profit from operations totaled 66.8 million yuan, or $9.7 million, during Q1. This was a massive turnaround from the 5.95 billion yuan ($876 million) loss in Q1 2025.

Additional context

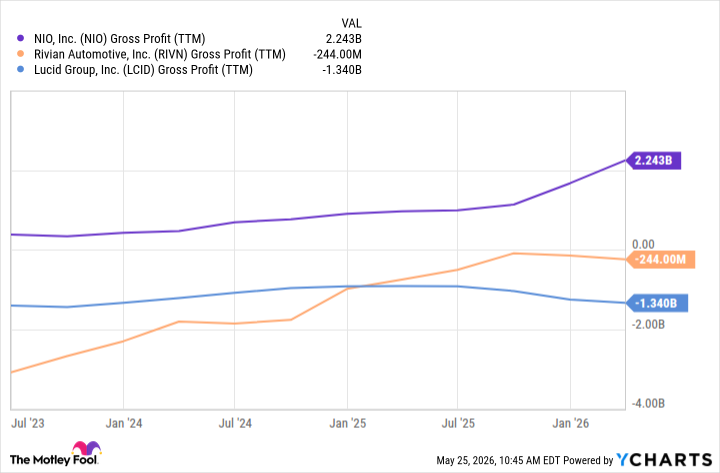

It’s impressive for Nio to be performing this well in a rough domestic market. Comparing the automaker’s gross profit to Rivian Automotive (RIVN +7.84%) and Lucid Group (LCID +9.97%), two similar competitors in terms of EVs albeit operating in different regions, shows how far ahead Nio really is.

NIO Gross Profit (TTM) data by YCharts.

There are two primary takeaways from the graph above. First, Rivian's progress over the past three years in improving its unit economics has been clear. Starting from a worse gross profit position than rival Lucid before quickly surpassing it, the company has consistently and impressively improved gross profits culminating in its first full-year gross profit for 2025. Its progress compared to rival Lucid should be lauded, but compared to Nio, it’s clear the latter is a step ahead in the long race to achieve consistent profitability.

Lucid is widely recognized for designing and producing some of the world’s most advanced EVs, but it’s consistently been hindered by production issues, recalls, and supplier hiccups, which have disappointed investors more than they'd like. Rivian, on the other hand, has made much progress but lacks the scale of Nio to turn its improving gross profitability into adjusted operating profits, though that day appears to be approaching.

NYSE: NIO

Key Data Points

Is Nio finally a buy?

Right now, Nio is doing what Rivian and Lucid both dream of doing: Proving to investors that operational efficiencies are at a level where long-term, sustained profitability is achievable. That’s exactly what investors want to see from Rivian and Lucid since that would unlock higher valuations and rising stock prices.

Nio also has momentum as it’s aggressively expanding beyond its namesake premium luxury Nio product lineup, and sub-brands such as Onvo and Firefly are expanding rapidly and allowing the company to capture valuable volume and scale even if in more price-sensitive segments. Nio’s Q1 results suggest that despite sub-brands expanding in volume in more affordable segments, the automaker’s pricing power remains strong, as do margins.

The Chinese EV maker still has plenty of questions, including whether its massive bet on a unique battery-swapping network will become a pillar of revenue and profits, and whether it'll create an ecosystem for its products and consumers, or if it’ll turn out to be a massive capital expenditure that never pays off.

While the jury remains out on that development, one thing is clear: If you’re looking for a young EV play, it might be time to look overseas, because Rivian and Lucid are a step behind Nio at the moment.