Target (TGT 4.69%) reported improved results when it posted its latest quarterly numbers in May. The company showed some encouraging growth, suggesting that its business may be going in the right direction under new CEO Michael Fiddelke, who took over earlier this year.

While the stock is up around 30% this year, it didn't get a big boost after releasing its quarterly numbers. And a closer look makes it clear that while it may be doing well on a year-over-year basis, it still has a long way to go in showing that it has recovered from a decline that's been going on for some time.

Image source: Getty Images.

Target's growth rate has been underwhelming for a long time

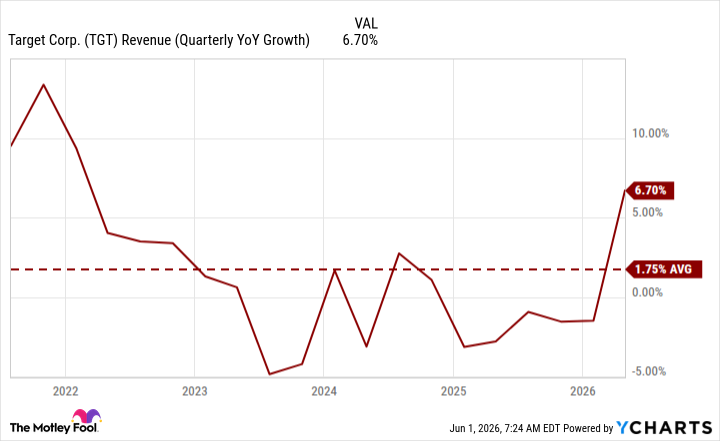

During the first quarter of Fiscal 2026, which went up until May 2, Target posted some seemingly solid results, with its net sales rising by 6.7% year over year, totaling $25.4 billion. But when you look at the bigger picture and assess how it has performed over a longer stretch, the results appear less impressive. In the chart below, you can see that its quarterly growth rate over the past five years has averaged less than 2%.

TGT Revenue (Quarterly YoY Growth) data by YCharts

When a business such as Target's has struggled to this extent, oftentimes experiencing a decline in revenue, that means in future years, it becomes easier for it to show growth. If you go back to Q1 2023, the company's sales totaled $25.3 billion, which is nearly identical to the revenue it posted this past quarter. That means that, given the declines it has experienced along the way, it's taken the retail giant about three years just to get back to where it was before its top line began to face considerable headwinds.

When taken into the appropriate context, Target's progress looks far less impressive. By simply going up against weaker comparables, it has shown growth, but that is by no means proof that its business is in much stronger shape.

NYSE: TGT

Key Data Points

Is Target's stock worth buying today?

Target has been rallying since the start of the year, but even with the increase in value, the retail stock trades at a fairly modest price-to-earnings (P/E) multiple of 17. By comparison, the average stock on the S&P 500 trades at a P/E multiple of 26.

The stock could be a reasonably cheap buy right now, which is why investors may have been loading up on it this year. Plus, it also offers a fairly high dividend yield of 3.6%. But with challenging economic conditions, you'll need to be patient with the stock, as it could encounter headwinds this year.