Alphabet (GOOG +0.71%) (GOOGL +0.71%) is one of the primary artificial intelligence (AI) hyperscalers. Unlike some of the other hyperscalers, it's approaching this massive trend from two directions.

First, it has its own family of large language models, led by Gemini. It has integrated this model throughout various products (like Google Search) and is among the most popular generative AI models out there. Second, it has a thriving cloud computing business in Google Cloud. Google Cloud just hit a $462 billion backlog, which is massive compared to its past 12 months of revenue.

I think this is as compelling a reason as any to buy the stock, as the growth implied by this backlog is massive. With Alphabet's stock down around 10% from its all-time high, now may be the perfect time to buy shares.

Image source: The Motley Fool.

Google Cloud is a top reason to buy Alphabet's stock

During Q1, Alphabet's Google Cloud quarterly revenue reached $20 billion. So, at this mark, it will take about 23 quarters to churn through the $463 billion backlog. However, Google has no plans to let that backlog last for more than five years. Google Cloud is rapidly growing, and it has increased its revenue at a jaw-dropping 63% year over year. Compared to other cloud computing firms, this is a far greater growth rate.

Amazon's Amazon Web Services (AWS) grew at a 28% clip and added $8.3 billion in new business. Google Cloud added $7.8 billion. So, just because Google Cloud is trailing the industry leader right now in overall size, it doesn't mean that it isn't adding as much new business. Microsoft's Azure cloud platform grew its revenue at a 40% clip, but the company doesn't break out the actual revenue figures; that's still a slower growth rate than for Google Cloud.

NASDAQ: GOOGL

Key Data Points

Google Cloud has a ton of momentum, and it's planning on carrying that into the next few years as it churns through the backlog. It is spending a massive amount of money on data center capital expenditures and recently bumped its 2026 guidance to spend between $180 billion and $190 billion this year. Demand for AI computing power has never been higher, and Alphabet is spending big to make sure that it has the capacity that its clients want. While 2026's expenditures are massive, Alphabet's management team noted in the call that 2027's capital expenditures will be "significantly" higher.

While some investors may be concerned about the spending, I am not. As Amazon's CEO, Andy Jassy, pointed out in its shareholder letter, the faster a cloud computing business grows, the more it must spend on infrastructure to support the growth. This indicates that Google Cloud's growth rate will likely accelerate as more computing capacity comes online, further strengthening the bull argument for Alphabet's stock.

With Google Cloud easily being the fastest-growing part of Alphabet's business, it will continue to capture a greater share of quarterly revenue, transforming Alphabet from an advertising-first business to a more balanced one. That's a welcome change for investors, as cloud revenue is steadier versus advertising, which can go up and down based on economic cycles.

But is Alphabet still a solid buy now?

Alphabet's stock has gone on an incredible run over the past year

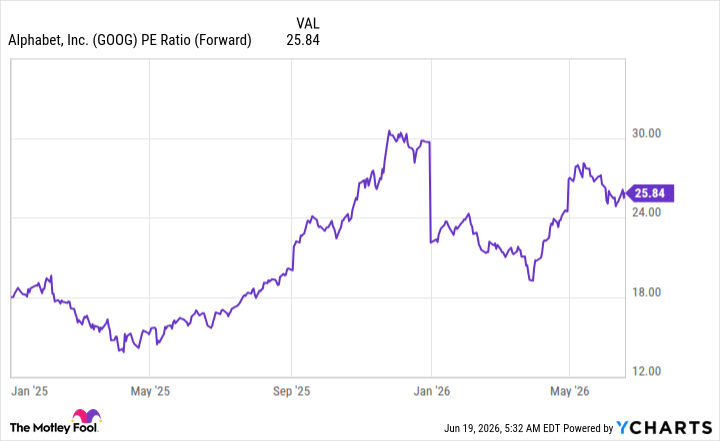

Alphabet's stock has more than doubled over the past year, and some of that was due to its rise from an absurdly low valuation. That's no longer the case, as Alphabet trades for about 26 times forward earnings.

GOOG PE Ratio (Forward) data by YCharts

While that may be a historically expensive mark for Alphabet, it's still in line with where other tech giants are trading right now. With Alphabet's transformation from an advertising-focused business (which usually traded at a discount due to the cyclical nature of the industry) to a cloud company, I think this valuation level is appropriate, and investors can confidently buy Alphabet's stock today with expectations of outperforming the market over the next five years.