With an estimated net worth of $2.5 billion, Charlie Munger didn't even crack the top 1,000 on Forbes' list of billionaires before he passed away in 2023. However, Munger was still a well-known, respected, and successful investor. He was vice chairman of Berkshire Hathaway (BRK.A -0.33%)(BRK.B -0.32%), serving as Warren Buffett's right-hand man for decades.

Here's who Munger was, his investing style, and some of his top holdings.

Who was Charlie Munger?

Charlie Munger was from Omaha, Nebraska, just like Warren Buffett. But the duo didn't meet as children. Rather, they were introduced by a mutual friend in 1959 while Munger was visiting from California. From there, the two struck up a friendship.

Munger served in the army, graduated from Harvard, ran a successful law firm, started a lucrative investment partnership, and made many good real estate deals in his lifetime. But he's most known for his close friendship with Warren Buffett and the part he played in turning Berkshire Hathaway into a trillion-dollar company.

Charlie Munger's personal stats

- Age: Charlie Munger was born on Jan. 1, 1924, and died on Nov. 28, 2023, at the age of 99.

- Source of wealth: Self-made billionaire through investing.

- Marital status: Widowed at the time of his death.

- Residence: Primary residence was reported to be his home in Pasadena, California.

- Children: Seven children and two stepchildren.

- Education: University of Michigan, California Institute of Technology, Harvard Law School.

Charlie Munger’s educational background

Charlie Munger attended public school, graduating from Omaha Central High School in 1941. From there, he went to the University of Michigan to study mathematics. But due to the escalation of World War II, he didn't finish, choosing rather to enlist in the army in 1942.

While in the army, Munger studied meteorology at California Institute of Technology, or Caltech. He graduated from its Ceiling and Visibility Unlimited (CAVU) program, which was helpful in his army service for forecasting flight conditions.

After leaving the army, Munger went on to Harvard Law School, graduating magna cum laude in 1948. Munger remained an avid reader and a lifelong learner. He encouraged others to be the same way, saying, "Go to bed smarter than when you woke up."

The whole secret of investment is to find places where it is safe and wise not to diversify.

Charlie Munger's investment approach

Charlie Munger's investment approach was predicated on the assumption that good opportunities are few and infrequent. As he once said, "Life is not just bathing you with unlimited opportunities."

Munger's process wasn't about finding as many good ideas as he could; he tried to eliminate bad and mediocre ideas first. This might seem like a backward approach, but he often spoke about the value of inverting one's thinking.

Munger's preference toward thinking in reverse was clearly illustrated when he said, "It's remarkable how much long-term advantage people like us have gotten by trying to be consistently not stupid, instead of trying to be very intelligent."

Because he believed good opportunities are rare, Munger seized opportunities when he finally saw them. Quoting his great-grandfather, Munger said, "When you get a lollapalooza, for God's sake, don't hang by like a timid little rabbit."

Consequently, Munger didn't share widely held views on diversification -- even holding 10 stocks risked being over-diversified, in his opinion. After all, if good ideas are truly rare, then why would one diversify a portfolio into dozens of things? The positive impact of the good ideas would only be diluted from all of the mediocre investments in the portfolio.

Munger employed a buy-and-hold investment strategy. When he found a good idea, he continued to hold the stock and allowed compounding to work for him. As he said, "The big money is not in the buying and the selling, but in the waiting."

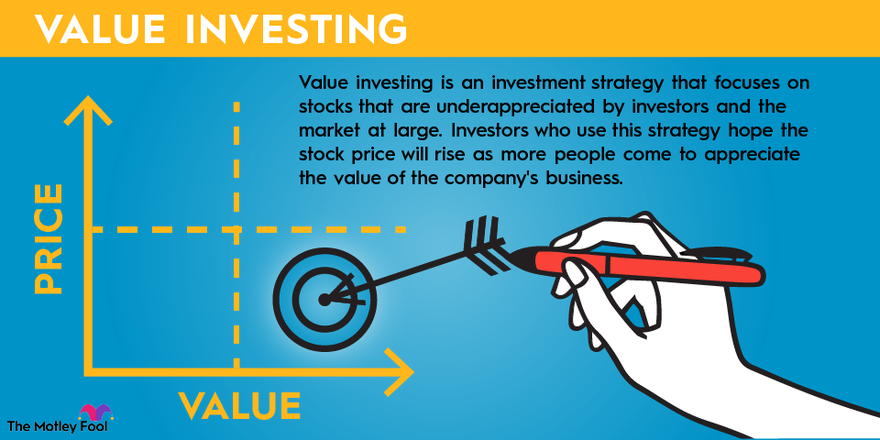

Finally, Munger was known to be a value investor, but there is an important distinction to be made. Many value investors look for whatever is cheap regardless of the quality of the business, but Munger was willing to pay more for quality.

In his 2014 letter to Berkshire Hathaway shareholders, Buffett credited Munger with changing his perspective on value investing. Buffett quoted Munger as saying, "Forget what you know about buying fair businesses at wonderful prices; instead, buy wonderful businesses at fair prices."

To summarize the investment approach, Munger believed that good investment opportunities are few, so he concentrated his portfolio around only those few good ideas, provided he could buy them for a fair price. After he bought these, he simply held on for the long haul.

Charlie Munger's investments

Given the consistency of his message regarding life's limited opportunities, it should come as no surprise that the table below doesn't just show the top three stock positions for Charlie Munger's portfolio. This table shows the only three stock positions he had in his later years.

Name | Ticker | Market Cap | About this company |

|---|---|---|---|

Berkshire Hathaway | BRK.A, BRK.B | $1.06 trillion | Berkshire is a conglomerate of wholly owned businesses including insurance, restaurants, rail, and more. It also owns a large investment portfolio. |

Costco | COST | $442 billion | Costco is a membership-based retailer with more than 850 warehouse locations. |

Daily Journal | DJCO | $500 million | The Daily Journal owns multiple newspapers, including the Los Angeles Daily Journal. It owns Journal Technologies, which is a software company used in legal settings. It also owns an investment portfolio. |

More from Charlie Munger

Charlie Munger wasn't active on social media, he didn't write any books, and he rarely made media appearances.

The best regular opportunity to hear from Munger came during the annual meeting for Berkshire Hathaway's shareholders, during which he and Buffett fielded questions from the audience.

Additionally, his long-term friend Peter Kaufman compiled many of Munger's thoughts and sayings into a book called Poor Charlie's Almanack: The Wit and Wisdom of Charles T. Munger. While not authored by Munger himself, the book does provide more insight into his way of thinking.

Related investing topics

The right takeaways from Charlie Munger

Munger admitted that a diversified portfolio is right for many investors even though that's not how he invested. Munger once said, "The idea of diversification makes sense to a point if you don't know what you're doing."

Of course, no one likes to admit any ignorance. However, the more concentrated your portfolio is, the greater the risk of permanent loss of capital if you're wrong. It's not a strategy to use flippantly.

Having a healthy level of self-awareness is imperative for investors looking to emulate Munger's investing style.

I constantly see people rise in life who are not the smartest, sometimes not even the most diligent, but they are learning machines. They go to bed every night a little wiser than they were when they got up, and boy, does that help, particularly when you have a long run ahead of you.

In other words, firmly know your limits but never stop growing. And if you want to keep learning about investing, absorbing as much of Charlie Munger's wisdom as possible is a great way to spend your time.

FAQ

About the Author