Note that if you earn less than the contribution limit for the year, you can contribute only up to that amount to your traditional IRA. For example, if you earn $5,000 in 2026, your maximum contribution for the year is $5,000.

Spousal option

If you're the sole breadwinner and your spouse doesn't work for compensation, you're eligible to contribute to a spousal IRA in their name -- assuming you have enough earned income to cover the contribution.

Deadline

The deadline to contribute is tax day for the year you're making the contribution. For example, the deadline for 2025 contributions will be April 15, 2026.

Tax treatment

Traditional IRAs are often described as tax-deferred accounts because money invested in a traditional IRA will grow without any tax levy until the money is withdrawn, typically in retirement.

In certain circumstances, contributions to a traditional IRA are tax-deductible for the year you deposit money. This is a way of deferring tax today in exchange for paying at a later date when you withdraw the money.

Income restrictions

There are no income restrictions on contributions to a traditional IRA. You can contribute regardless of your income level.

Deductibility exceptions

In the most general terms, you will receive a tax deduction if you (and your spouse) are not covered by retirement plans at your respective places of employment.

If you are covered by a retirement plan at work, you will receive a full deduction for your 2025 taxes if you earn less than $79,000 (single filers) or $126,000 (married filing jointly). You will receive at least a partial tax deduction if you earned less than $89,000 (single filers) or $146,000 (married filing jointly).

These amounts increase in 2026. If you're covered by a workplace retirement plan, you can receive the full deduction for 2026 if you earn less than $81,000 (single filers) or $129,000 (married filing jointly). You can take a partial deduction if you earn less than $91,000 (single filers) or $149,000 (married filing jointly). These rules are complex, so it's smart to review the IRS deductibility guidelines before making a contribution.

Required withdrawals

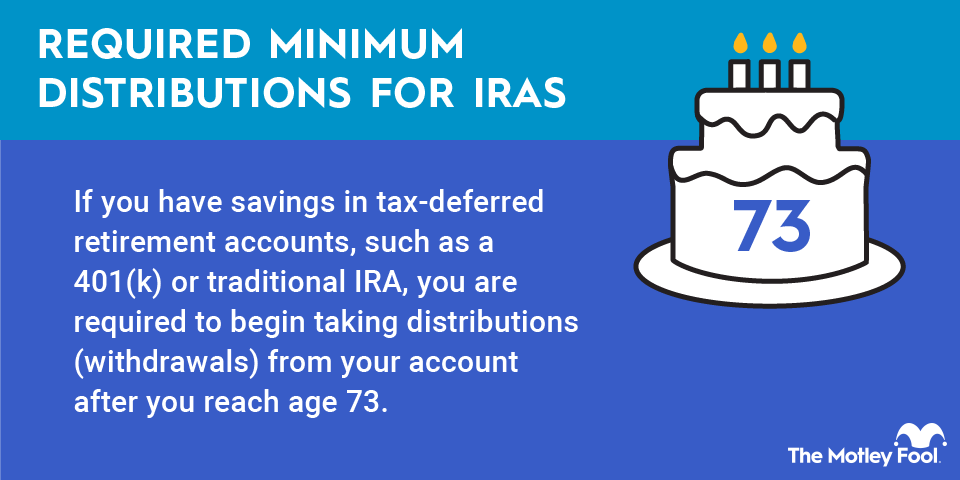

At age 73, you are required to take mandatory withdrawals from traditional IRAs. These are otherwise known as required minimum distributions, or RMDs. RMDs force a specified withdrawal amount from your IRA based on your life expectancy and have the effect of increasing your taxable income for the year in which you withdraw the money.

Your first RMD is due by April 1 of the year after you turn 73. The Secure Act 2.0, which passed in late 2022, pushed back the RMD age from 72 to 73.

Early withdrawals

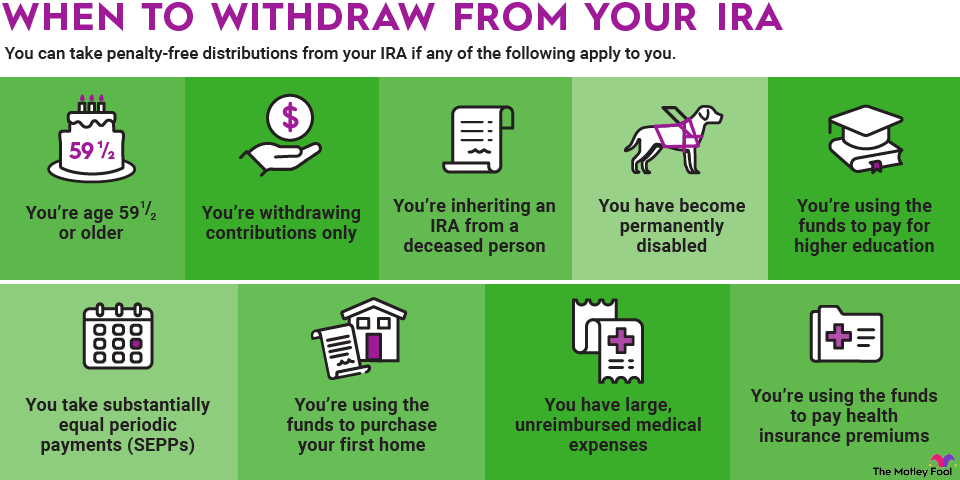

If you withdraw from a traditional IRA before the age of 59 1/2, you'll be responsible for both taxes and a 10% penalty for early withdrawal. There are a few exceptions for medical hardship, employment separation, and other extenuating circumstances.