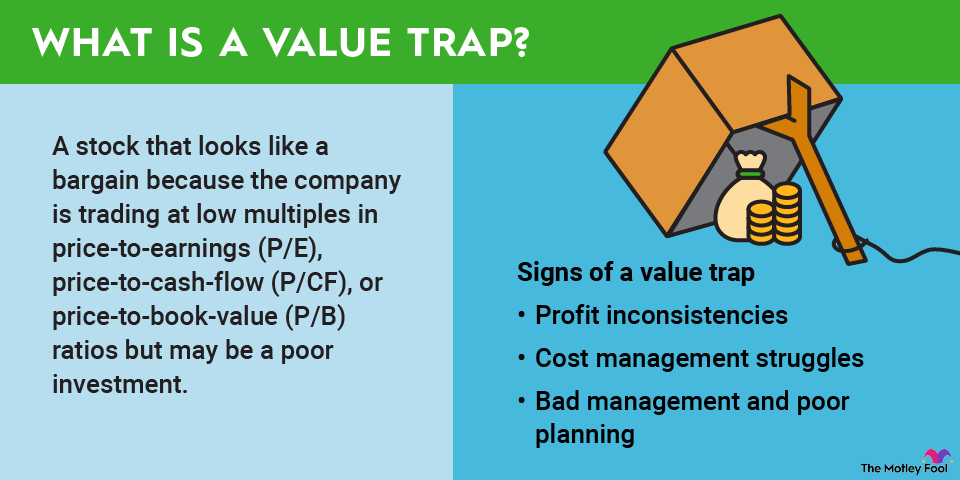

Loading paragraph...

Loading image...

Loading paragraph...

Loading paragraph...

Loading paragraph...

Loading hub_pages...

Loading paragraph...

The Motley Fool has a disclosure policy.

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool's premium services.

A value-added tax (VAT) is a tax on consumption that’s levied at every step of the production stage of a good or service. Businesses pay the sum of the value that’s added to the product or service, but they’re reimbursed for the value from the previous stage. Ultimately, the consumer pays the final tax.

More than 100 countries, including all members of the Organization for Economic Cooperation and Development (OECD), use a VAT to collect taxes -- except the United States, where sales taxes are generally set by state and local governments. The VAT is favored by many countries because it makes everyone in a supply chain responsible for their amount of taxes, encouraging producers to follow tax laws.

Essentially, the VAT rate is usually applied to each stage of production. The value from previous stages is deducted from the latest value.

VAT advocates argue that the tax is preferable to an income tax because it doesn’t punish wealthy taxpayers (although some countries have both an income tax and a VAT). Critics, however, note that the VAT is basically a regressive tax on less wealthy taxpayers because it taxes consumption rather than wealth. Lower-income taxpayers generally spend a larger share of their income on goods and services like food, transportation, and fuel. A VAT generally is also a flat tax, which means that wealthy people generally pay a smaller share of their income in taxes than low- and middle-income taxpayers.

The tax is also criticized for its effects on imports. A company that imports goods or services generally pays the tax on their entire value, even if the foreign manufacturer paid other taxes on them. Many U.S. companies consider the VAT a trade barrier.

The VAT differs from country to country. India, for example, has a VAT that ranges from 5% to 28%, depending on the category. Mexico sets a 16% VAT on everything except books, food, and medicine. Although most VATs are simple flat-rate taxes, some countries have exemptions or reduced rates for certain goods and services. The United Kingdom levies a standard 20% rate on most goods and services, although some are reduced to 5% or even totally exempt from the tax.

Other countries have a staggered VAT. Spain has a 21% rate, but the reduced VAT falls to 10% for food, many real estate transactions, and some healthcare. A super-reduced VAT rate of 4% is levied on basic food products, prescription drugs and other medications, books, and home healthcare. The VAT is eliminated for financial products, insurance, stamps, and professional health and medical care.

Some countries have a VAT but describe it as a “goods and services tax” (GST). Australia levies a 10% GST, with revenue redistributed to states and territories. Some items are exempt, including fresh food, education, health services, and some medical products.

The Nordic countries of Denmark, Norway, Sweden, and Finland have some of the highest VAT rates in the world; Denmark and Sweden levy a 25% tax on most goods and services. As with other countries, there are exemptions: For example, Sweden’s rate is reduced to 12% for food, including at restaurants and hotels, and 6% for printed material and private transport.

Here’s an example of how a VAT works: A clothing manufacturer buys materials from a textile company for $5 and pays a 10% VAT. The end price is $5.50, including the VAT. The textile company keeps the $5 and pays $0.50 to the government.

Next, the clothing manufacturer makes a shirt and sells it to a retailer for $10. Ten percent of the VAT, or $1, is added to the sale. The manufacturer pays $0.50 in VAT to the government and keeps $0.50 for the tax that was paid to purchase the textiles.

The retailer then sells the shirt to a customer for $20. Again, a 10% VAT is paid, so the total price is $22. The seller keeps $1 from the VAT for the purchase of the shirt and pays the other $1 to the government.

The customer who buys the shirt pays $22, or the price of the shirt plus the $2 VAT. So the customer pays the entire VAT: the $0.50 paid by the textile company, the $0.50 paid by the shirt manufacturer, and the $1 paid by the retailer. And, of course, the customer pays for the shirt.