Over a decade ago, a nebulous idea called "the cloud" started to gain momentum. Using the internet to deliver a service to a remotely located user was a novel concept, but today, it's an essential piece of the economy.

Artificial intelligence (AI) is likewise an important but oft-misunderstood technology. It's still developing, but it promises to create a new segment of the economy based on the automation of simple tasks and raw data crunching.

Researcher IDC estimates that some $37.5 billion was spent globally on AI systems in 2019. That's not a particularly large sum, but IDC thinks that figure could roughly triple by 2023. Just as the cloud is now responsible for delivering all sorts of tools and services, AI systems are expected to have a wide range of uses in a very short period of time.

Last month, I talked up Alphabet, salesforce.com, and NVIDIA (NVDA +3.44%). For July, I'm revisiting NVIDIA and going with Micron Technology (MU +0.06%) and Appian (APPN +5.31%) as my AI picks of the moment.

Image source: Getty Images.

Before there was software, there was hardware

As a final product, AI is software: an algorithm that dictates the function of a system or device. But hardware must be built to train, deploy, and operate that software. As AI is still in its infancy, the hardware used to support it is where I will gravitate for the time being.

When talking about AI hardware, it's easy to default to NVIDIA. The folks at NVIDIA see a world where AI is ubiquitous, assisting us with tasks and making recommendations. That future is nigh. The company's wares are already a largely unseen part of everyday life. Whether it's an advanced driver assist feature in a new car, a recommendation for a movie or song, high-end graphics on video games, or the packages delivered to your home, there's a good chance NVIDIA was involved.

The bear argument these days is that NVIDIA is too expensive. Looking back over the last year of results, it most certainly is. Shares trade for 20 times revenue and 54 times free cash flow (revenue less cash operating and capital expenses). Yikes.

But I'll reiterate what I've said in previous articles on NVIDIA: The past is less important than the future for a high-growth company. Between its internal development and its recent acquisition of Mellanox (which I believe NVIDIA got for a song), revenue for the second quarter was forecast to be some 42% higher than a year ago. With a whole year left to lap its pre-Mellanox results and the current state of world affairs creating insatiable demand for new semiconductors and devices, double-digit percentage growth could continue for a while longer.

Here's my full disclosure: I continue to add shares of NVIDIA not because I think it's a fair value now, but because I see at least a decade of rapid AI industry development ahead with the company delivering some of the primary components necessary to make it all possible. That kind of time horizon may not gel for many, but if you think your money will still be invested in 10 years, I don't see why this shouldn't be a core set it and forget it holding in any portfolio.

Remember one of intelligence's key ingredients

Memory is crucial to human and artificial intelligence. A machine's ability to make predictions and perform automated work isn't simply dictated by how quickly it can crunch information. It also needs stored data from which it can generate such predictions. That's where memory semiconductors come in.

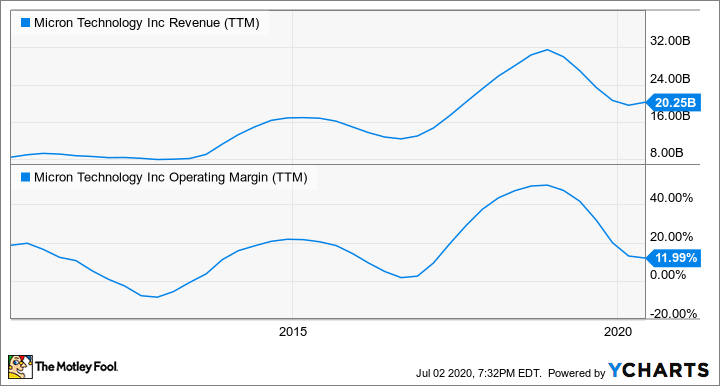

Digital memory chips are necessary for all sorts of electronic systems. Many types are highly commoditized and sensitive to changes in supply and demand. That can wreak havoc on pricing and lead to wild swings from sky-high profitability to heavy losses. Micron has historically been at the mercy of this cycle.

This memory chip leader will probably continue to be highly cyclical. However, the company changed its approach a few years ago. It invested in new chip technology and architecture to differentiate its portfolio from the rest of the pack. It's also increasingly focused on higher-order computing needs and has walked away from deals that don't meet its investment return criteria. Even during the lows of a year-plus semiconductor slump, Micron has thus remained profitable.

Data by YCharts.

Surging orders amid the COVID-19 pandemic have pulled Micron out of its trough and pushed it back into growth mode. Revenue was up 14% in the last quarter. AI systems, data centers, and connected devices operating at the "network edge" have needed upgrades during the lockdown.

Lower sales of consumer-facing devices like smartphones and cars partially offset results. But upgrade cycles for new video game consoles, PCs, and advanced driver assistance systems are expected in the years ahead. Micron's advanced memory chips play an integral role in these smart devices. With a new upcycle possibly beginning, I think the stock is a buy now.

Training bots to handle soul-crushing work

People worry that AI will compete with humans for jobs. It's not an ungrounded concern. Tech's increased productivity and cost-savings benefits are very real. Many workers may need to future-proof their careers -- or change careers altogether -- because of the disruptive nature of tech. But right or wrong, it's happening. Humans have always had to compete with the technology they create.

AI and related technologies like low-code software development are proving useful to organizations trying to adjust to shelter-in-place orders and the "new normal" of the pandemic. Low-code isn't AI, per se. It's a visual toolkit that builds applications much faster than prior technologies.

There are a number of low-code providers out there, but Appian made an interesting recent move. Early in 2020, the company made its first-ever acquisition by buying robotic process automation (RPA) firm Novayre Systems. What is RPA? Think of it as a virtual robot that can be programmed to do tasks within software, like populating form fields.

Both low-code software and RPA can help companies resume operations. But won't that steal jobs? In the short term, it might. But if it's going to happen, investors might as well prepare, and I see owning Appian as one way to do so.

Granted, Appian expects its recurring software revenue to slow to a 25% to 26% year-over-year pace in the second quarter (down from 34% in 2019 and 46% in the first quarter of 2020) as many customers are putting new projects on temporary hold. Appian, a small company, still operates at a loss on top of that.

However, the company had no debt and $149 million in cash and equivalents at the end of March 2020. This doesn't include its recently announced sale of 1.93 million new shares of its common stock, which would raise about $100 million in fresh cash at current share prices. That news has shares down over 15% from all-time highs. Appian trades for 13 times forward revenue expecations, so it isn't particularly cheap. But I think this is an early AI and automation vendor worth taking seriously.