ASML (ASML +4.92%) is a critical player in the artificial intelligence (AI) ecosystem, as it makes the machines that manufacture the advanced chips needed for AI model training and inference. It could be one of the best pick-and-shovel plays in the AI space. The company's results, therefore, provide useful insight into the state of the AI economy, which encompasses investments in AI infrastructure, such as data centers, as well as spending on software and services that enable productivity gains for end users.

Not surprisingly, investors eagerly awaited ASML's first-quarter results, and it didn't disappoint.

Let's take a closer look at the Dutch semiconductor bellwether's latest report and see why its strong showing is great news for two other pick-and-shovel companies that are benefiting from the AI supercycle.

Image source: Getty Images

ASML lifts its outlook owing to insatiable AI demand

ASML released its first-quarter 2026 results on April 15. Its revenue increased by almost 14% year over year to 8.8 billion euros, close to the higher end of its guidance range. More importantly, ASML management increased its 2026 revenue guidance, noting that the demand for both advanced memory and logic chips remains robust.

NASDAQ: ASML

Key Data Points

ASML management believes that memory and chip "supply will not meet the demand for the foreseeable future." The company sees supply constraints in the AI, smartphone, and personal computer markets, which is why it expects its customers to build more capacity. As a result, ASML expects its customers to increase their capital expenditure budgets in 2026 and beyond.

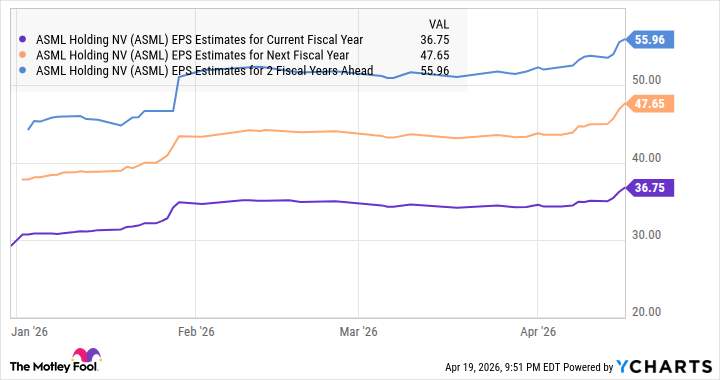

This explains why ASML now anticipates its 2026 revenue to land between 36 billion and 40 billion euros. Earlier, it was expected that revenue would land between 34 billion and 39 billion euros this year. The company has increased its guidance by 4% at the midpoint. However, don't be surprised if it increases its guidance as the year progresses.

I say this because ASML is trying to produce more of its advanced extreme ultraviolet (EUV) lithography machines that help customers print advanced AI chips. It expects to ship 25% more of its low-NA EUV chips this year than in 2025, followed by a 33% jump next year. So there is a strong chance of an acceleration in ASML's earnings growth, which should pave the way for more upside in this semiconductor stock following its 36% jump so far in 2026.

Data by YCharts.

ASML, however, isn't the only AI pick-and-shovel company set to win big from healthy AI infrastructure investments. Celestica (CLS +1.61%) and Vertiv Holdings (VRT +1.24%) are two other important AI companies that could continue to soar amid strong demand for AI infrastructure.

These high-flying AI stocks have more upside to offer

The AI infrastructure ecosystem is made up of more than just chips produced with ASML's machines. For instance, AI data centers require significant power and generate substantial heat, which necessitates power and thermal management solutions.

Vertiv is in the business of providing critical data center technology, such as power supply systems and liquid-cooling solutions. The company also makes server racks for mounting AI accelerator chips. The company's business has received a big shot in the arm thanks to AI infrastructure investments.

NYSE: VRT

Key Data Points

Its 2025 revenue was up by almost 28% to $10.2 billion. Management anticipates a 32% increase in revenue this year to $13.5 billion. What's more, Vertiv anticipates a 43% spike in adjusted earnings this year to $6.02 per share. However, the potential increment in capital expenses by AI companies that ASML notes could help Vertiv exceed management's guidance.

After all, more data center chips would pave the way for stronger demand for Vertiv's cooling and power management infrastructure. The company was already sitting on a huge $15 billion order backlog at the end of 2025, with the metric jumping 109% year over year. Importantly, Vertiv is focused on boosting its manufacturing capacity to meet the fast-growing infrastructure demand.

This could pave the way for more upside in this AI stock following a 90% rally so far in 2026.

Meanwhile, Celestica is benefiting from the booming demand for fast connectivity in AI data centers. Celestica is a Canadian electronics manufacturing company that designs and manufactures hardware products for the data center, aerospace and defense, industrial, semiconductor, and healthcare end markets.

The company's data center business has taken off, primarily driven by strong demand for the networking switches it designs for its hyperscale customers. Celestica management noted in January that it is a preferred manufacturing partner for Google and is enhancing its manufacturing capacity to support the growing demand for the tech giant's custom AI chips.

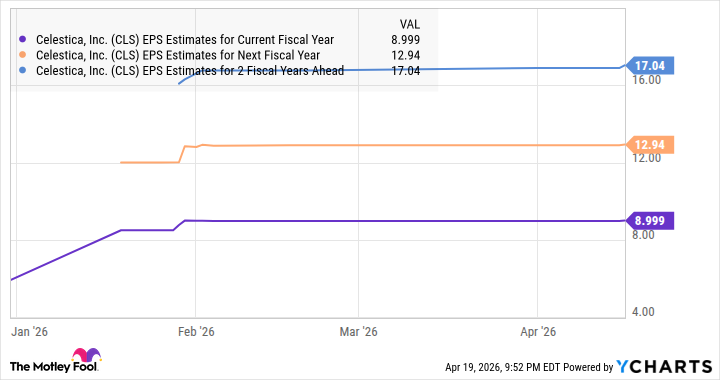

Celestica's numbers make it clear that it is making the most of the AI boom. Its 2025 revenue increased by 28% to $12.4 billion. Earnings growth was even better. Celestica's non-GAAP earnings jumped by 56% year over year to $6.05 per share. What's more, Celestica has guided for a 37% revenue jump this year, along with a 45% earnings jump to $8.75 per share. Analysts, however, are expecting stronger growth.

Data by YCharts.

The chart clearly shows that Celestica is poised to sustain strong earnings growth levels. That could translate into more upside for Celestica investors in the long run, following a 34% stock price jump this year.