Rolling over from a traditional 401(k)

If you currently have a traditional 401(k) and want to convert it to a Roth 401(k), you also may have the option to do that. But it's important to understand the tax implications of this type of rollover.

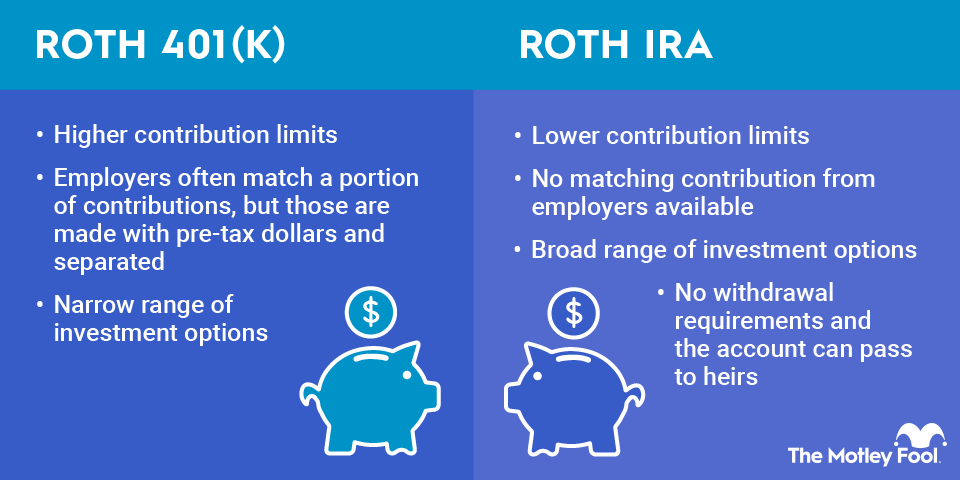

You contribute to a traditional 401(k) with pre-tax funds and are taxed on withdrawals as ordinary income after age 59 1/2 (before then, you'll also incur a 10% early withdrawal penalty under most circumstances). However, when you contribute to a Roth 401(k), you contribute with after-tax dollars but can take tax-free withdrawals.

Because of the different tax rules, rolling over money from a traditional to a Roth 401(k) has tax consequences, with converted funds classified as taxable income. This can increase the amount of income taxes you owe the IRS in the year the conversion takes place.

However, while you may get a large IRS tax bill, this can make sense in some situations. You may wish to convert a traditional 401(k) to a Roth 401(k) under the following circumstances:

- You're in a lower tax bracket now than you expect to be in retirement: If this is the case, you'll owe less tax on the converted funds at your current low tax rate than you'd otherwise pay when taking taxable distributions from a traditional 401(k) as a retiree.

- You want to minimize taxes on Social Security: Distributions from a Roth 401(k) aren't considered "countable" income when you're determining if a portion of your Social Security benefits will be taxed.

Converting a traditional 401(k) to a Roth 401(k) is simple -- you'll just need to complete some paperwork to request the transfer of funds.

However, you'll want to make sure you have money available outside of your retirement account to pay the taxes due as a result of the conversion. Otherwise, you could be forced to make an early withdrawal, which may be subject to a 10% penalty.

Pros and cons of rolling over your 401(k)

Here are some of the biggest benefits of rolling over your Roth 401(k) to a Roth IRA:

- You can get access to more investment options than your workplace plan likely offers.

- You can preserve the tax benefits a Roth account offers.

- Converted amounts don't count toward annual Roth IRA contribution limits.

- You can consolidate with other Roth IRA accounts.

- You won't have to worry about your 401(k) getting lost if you leave it with an old employer or moving the money again if you switch to a new employer's account and then leave the new job.

Here are some of the biggest disadvantages:

- You'll usually have to sell your investments to roll over your account.

- If you're opening a new Roth IRA to roll the funds into, you may have to wait five years from the time you open the account to be able to take tax-free withdrawals.