Traditional and Roth IRA rules vary based on your personal circumstances. Getting a better understanding of these guidelines is a good idea for all retirement savers. Below you'll find the most important IRA rules to know for 2024 and 2025.

Image source: Getty Images.

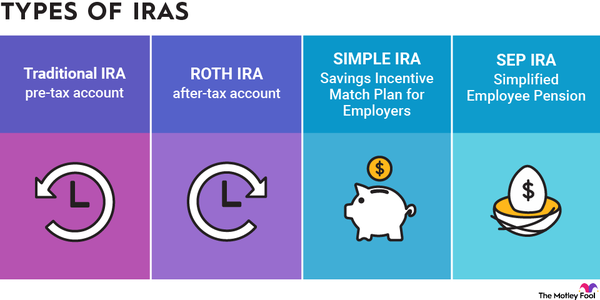

Traditional IRA rules you need to know

Traditional IRA rules you need to know

- Eligibility: In order to contribute to a traditional IRA, you must have taxable compensation. Broadly speaking, if you earned money, you are eligible to open and contribute to a traditional IRA.

- Contribution limits: You are able to contribute $7,000 in 2024 and 2025. If you're older than 50, you can make an extra $1,000 catch-up contribution and contribute up to $8,000 in both tax years. Note that if you earned less than the contribution limit for the year, you can contribute only up to that amount to your traditional IRA. If you earn $7,000 or less in 2024 and 2025 (or $8,000 if you're older than 50), use your earnings as your contribution limit. If your earnings exceed $7,000 in 2024 and 2025 (or $8,000 if you're at least 50), these are your contribution limits.

- Spousal option: If you are the sole breadwinner and your spouse doesn't work for compensation, you are eligible to contribute to a spousal IRA in their name, assuming you have enough earned income to cover the contribution.

- Deadline: The deadline to contribute is tax day for the year you're making the contribution. For example, the deadline for 2024 contributions will be April 15, 2025.

- Tax treatment: In certain circumstances, contributions to a traditional IRA are tax-deductible for the year you deposit money. This is a way of deferring tax today in exchange for paying at a later date when you withdraw the money. Traditional IRAs are often described as tax-deferred accounts because money invested in a traditional IRA will grow without any tax levy until the money is withdrawn, typically in retirement.

- Income restrictions: There are no income restrictions on contributions to a traditional IRA. You can contribute regardless of your income level.

- Deductibility exceptions: In the most general terms, you will receive a tax deduction if you (and your spouse) are not covered by retirement plans at your respective place(s) of employment. If you are covered by a retirement plan at work, you will receive a full deduction for your 2024 taxes if you earn less than $77,000 (single filers) or $123,000 (married filing jointly). You will receive at least a partial tax deduction if you earned less than $87,000 (single filers) or $143,000 (married filing jointly). These amounts increase in 2025. If you're covered by a workplace retirement plan, you can receive the full deduction for 2025 if you earn less than $79,000 (single filers) or $126,000 (married filing jointly). You can take a partial deduction if you earn less than $89,000 (single filers) or $146,000 (married filing jointly). These rules are complex, so it's smart to review the IRS deductibility guidelines before making a contribution.

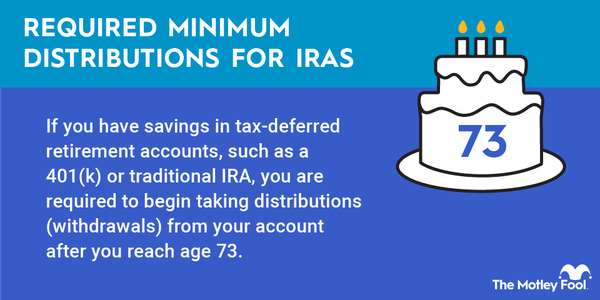

- Required withdrawals: At age 73, you are required to take mandatory withdrawals from traditional IRAs. These are otherwise known as required minimum distributions, or RMDs. RMDs force a specified withdrawal amount from your IRA based on your life expectancy and have the effect of increasing your taxable income for the year in which you withdraw the money. Your first RMD is due by April 1 of the year after you turn 73. The Secure Act 2.0, which passed in late 2022, pushed back RMD age from 72 to 73.

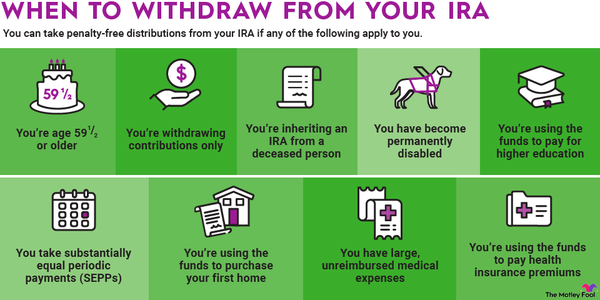

- Early withdrawals: If you withdraw from a traditional IRA before the age of 59 1/2, you'll be responsible for both taxes and a 10% penalty for early withdrawal. There are a few exceptions for medical hardship, employment separation, and other extenuating circumstances.

Roth IRA rules you need to know

Roth IRA rules you need to know

- Eligibility: Similar to a traditional IRA, you'll need to have earned income. But the Roth tends to get more restrictive depending on how much income you earn; specifically, this depends on your modified adjusted gross income (MAGI). The charts below will allow you to assess your personal eligibility:

For Single Filers, 2024 Filings

| Modified Adjusted Gross Income | Contribute to Roth Directly? | Contribution Amount |

|---|---|---|

| $146,000 or less | Yes | Full ($7,000 if < 50, $8,000 if 50+) |

| $146,001-$161,000 | Yes | Partial |

| $161,001 or more | No | $0 |

For Joint Filers, 2024 Filings

| Modified Adjusted Gross Income | Contribute to Roth Directly? | Contribution Amount |

|---|---|---|

| $230,000 or less | Yes | Full ($7,000 if < 50, $8,000 if 50+) |

| $230,001-$240,000 | Yes | Partial |

| $240,000 or more | No | $0 |

For Single Filers, 2025 Filings

| Modified Adjusted Gross Income | Contribute to Roth Directly? | Contribution Amount |

|---|---|---|

| $150,000 or less | Yes | Full ($7,000 if < 50, $8,000 if 50+) |

| $150,001-$165,000 | Yes | Partial |

| $165,000 or more | No | $0 |

For Joint Filers, 2025 Filings

| Modified Adjusted Gross Income | Contribute to Roth Directly? | Contribution Amount |

|---|---|---|

| $236,000 or less | Yes | Full ($7,000 if < 50, $8,000 if 50+) |

| $236,001-$246,000 | Yes | Partial |

| $246,000 or more | No | $0 |

- Spousal option: As with a traditional IRA, you can make Roth IRA contributions on behalf of your non-working spouse if you have enough earned income to cover both contributions.

- Deadline: For all 2024 contributions, you must complete them by April 15, 2025.

- Tax treatment: Roth IRA contributions are considered post-tax deposits. Upon contribution to a Roth IRA, money has already been taxed and can grow tax-free forever.

- Deductibility: Roth IRA contributions are never tax-deductible.

- Withdrawals: You are eligible to access Roth IRA funds -- as well as the earnings in the account -- at age 59 1/2, provided the Roth IRA has been in existence for five years or more. When you withdraw money from the account under these circumstances, you will pay zero tax. Roth IRAs also don't have RMDs at any point during the account holder's life.

- Early withdrawals: You can withdraw contributions from Roth IRAs at any time tax- and penalty-free. The five-year rule mentioned above applies only to the earnings in the account. This is a significant difference between the traditional and Roth IRA.

What's changing in 2025

What's changing in 2025

- Deductibility exceptions for traditional IRAs: While the underlying rule has not changed, you will receive a full tax deduction for your traditional IRA contribution if you earn less than $79,000 if you're a single filer or $126,000 if you're filing jointly with a spouse. Partial deductions are available for single filers earning up to $89,000 and joint filers earning up to $146,000. Beyond these income limits, no deduction is available.

- Roth IRA income limits: The Roth IRA income limits will increase in 2024. If you're a single filer, you'll be able to contribute fully to a Roth IRA if your MAGI is below $150,000. If you're a joint filer, you'll be able to contribute the maximum if you earn below $236,000. If you earn more than $165,000 as a single filer or more than $246,000 as a joint filer, you are not able to contribute directly to a Roth IRA. If you earn in the middle of these ranges, you can contribute a reduced amount.

Related retirement topics

Know the rules to make your life easier

Knowing the most basic rules can go a long way in making the IRA your best friend. Making annual IRA contributions is one of the best ways to boost your net worth and enjoy a more comfortable retirement, so the time invested in learning about IRA mechanics is well worth it. This is one of those things that get much easier with repetition, so don't be afraid to start slow and go at your own pace.

The Motley Fool has a disclosure policy.