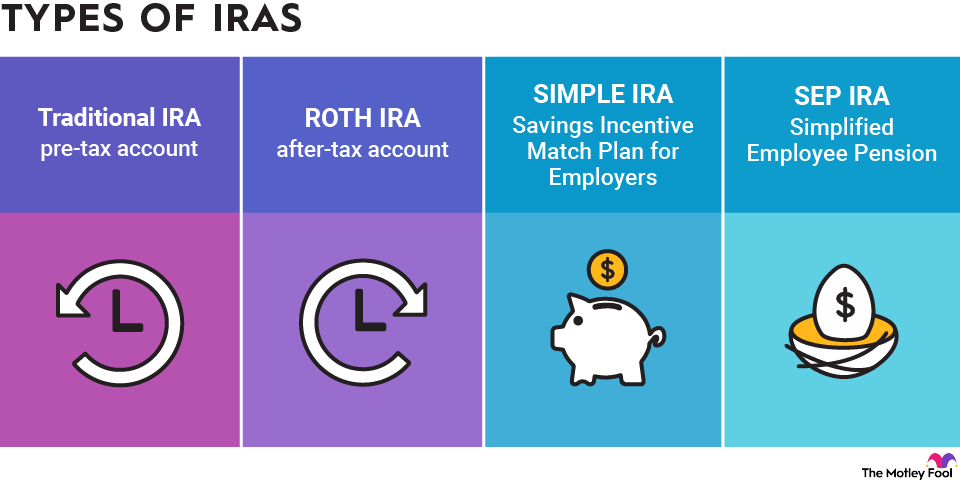

What rules apply to traditional IRAs?

Age-related contribution rules: You can contribute to a traditional IRA at any age -- as long as you have earned income equal to or greater than your contribution amount.

Contribution limits: For the 2025 tax year, the IRA contribution limit is $7,000 for both traditional and Roth IRAs. This will rise to $7,500 in 2026. Depending on your income and tax filing status, you may be able to deduct the full amount of your contribution.

If you’re older than age 50, you’re eligible to contribute an extra $1,000 for the 2025 tax year, or a total of $8,000. This is known as a catch-up contribution. In 2026, the catch-up contribution will increase to $1,100, allowing individuals aged 50 and above to save up to $8,600 in an IRA.

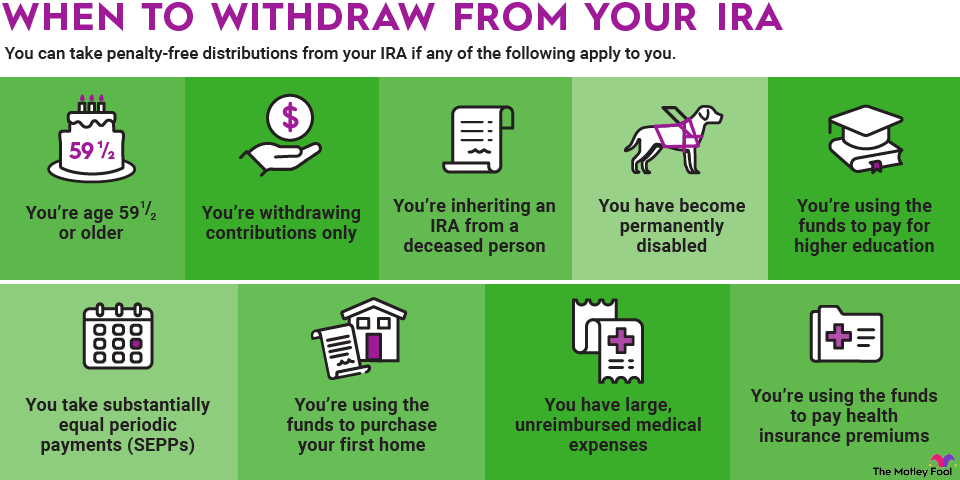

Withdrawal rules: You are eligible to withdraw from a traditional IRA without penalty at age 59 1/2. If you withdraw from a traditional IRA before then and don’t have a qualifying reason, you’ll pay income taxes on the withdrawal, as well as a 10% early withdrawal penalty.

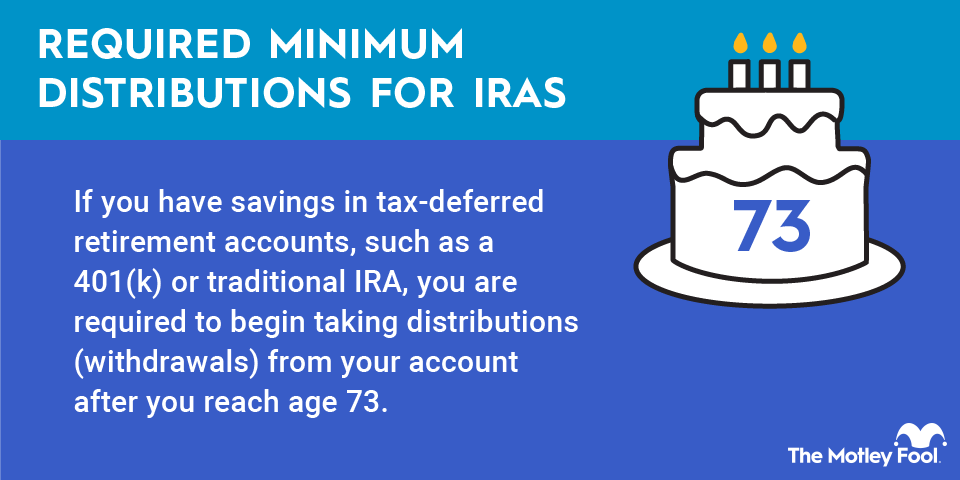

Additionally, you must take required minimum distributions (RMDs) beginning at age 73. RMDs are mandatory minimum withdrawals from your retirement account, so you’ll eventually pay income tax.

The amount of your annual RMD is based on your life expectancy as calculated by IRS actuaries. Your RMD will be taxed as ordinary income; therefore, it is essential to plan for the impact of your RMDs in advance.

Deduction eligibility: Your eligibility to take a tax deduction for your traditional IRA contribution hinges on three factors: your income, your tax filing status, and whether or not you are covered by a retirement plan at work, such as a 401(k).

For single filers covered by a retirement plan at work: