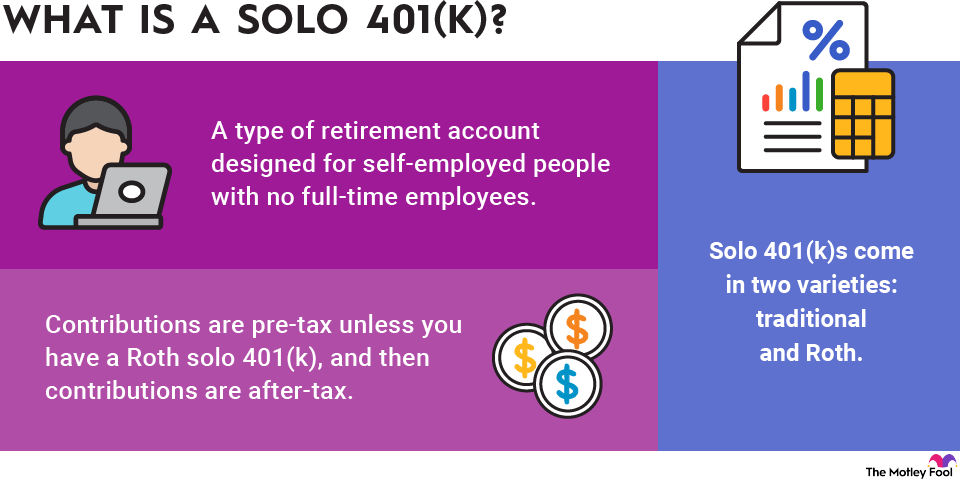

2. Solo 401(k)s

Solo 401(k)s are similar to employer-provided plans and offer high contribution limits, but there's also a relatively high administrative burden. Some brokerage firms charge fees for solo 401(k)s.

You can't contribute to a solo 401(k) if you have employees other than your spouse. However, you can choose whether to opt for a traditional 401(k) that you contribute to with pre-tax dollars or a Roth IRA that you contribute to with after-tax dollars (but which allows tax-free withdrawals in retirement).

You can make contributions to a solo 401(k) as both employee and employer, with the total equaling $72,000 in 2026 ($70,000 in 2025).

If you're 50 or older, you're eligible for an additional $8,000 catch-up contribution in 2026 ($7,500 in 2025), bringing the total contribution limit to $80,000 in 2026 ($77,500 in 2025).

The SECURE 2.0 Act also created a new "super catch-up contribution" for workers ages 60 to 63, who can make $11,250 in catch-up contributions in both 2025 and 2026.

The contributions break down as follows:

- Up to $24,500 as an employee in 2026 ($23,500 in 2025). Catch-up contributions are also made as an employee.

- As an employer, up to 25% of net self-employment earnings or the maximum of $72,000 in 2026 ($70,000 in 2025). Net self-employment earnings are equal to net profit minus your SEP contribution (excluding any catch-up contribution) and half of self-employment taxes.

If you have a spouse who is employed by and earns income from this business in some capacity, you can make the same contributions for each of you.