How do I make money with bonds?

Generally, investors profit from the yield they earn by owning bonds. Bond prices can fluctuate, losing value as interest rates rise and gaining value as they fall. But generally, if you buy a bond and hold it to maturity, you will earn some yield and get back the face value (the price the bond was issued for).

Note that some bonds are convertible, which means the borrower can repay the bond with stock. If this is the case and you don't want to own shares of the company, you'll want to either sell the issue before maturity or sell the shares you get when the bond matures.

Types of bonds

Treasury bonds, notes and bills are issued by the U.S. government. They range from four weeks to 30 years before maturity and are generally viewed as the safest bonds on Earth.

Municipal bonds are issued by state and local governments. They are generally very safe and usually pay higher yields than Treasury bonds.

Corporate bonds are issued by private companies. Depending on the issuer's financial strength and creditworthiness, bonds can be very safe or much riskier.

For riskier bonds, investors are paid a premium in the form of a higher yield based on that risk. As described above, most bonds are repaid in cash at maturity, but with convertible notes, the issuer can repay investors with shares of the company's stock.

Pros and cons of bonds

Pros

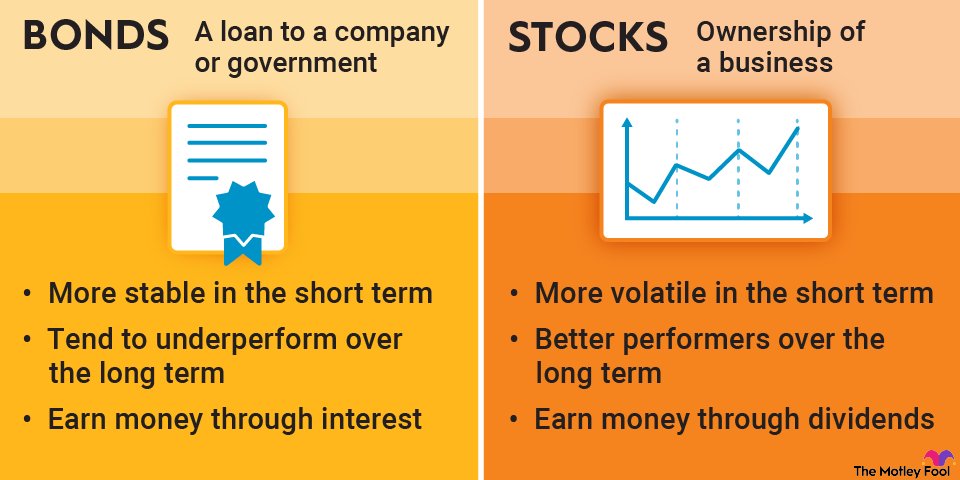

- They are a stable, low-volatility source of income.

- They have a lower risk of permanent losses than stocks.

- Bonds have a higher yield than savings, which helps protect the value against inflation.

- The value can increase if interest rates fall.

Cons

- Bonds can lose value if the issuer cannot make interest payments or repay them at maturity.

- They can lose value if the investor sells the bond before maturity and interest rates have increased.

- They have generally underperformed stocks as a long-term investment.

How do I buy bonds?

Like stocks, most online brokers have a trading platform for buying and selling corporate and municipal bonds, both new issues (from the company) and secondary markets (from other investors). You can buy Treasury securities directly through the Treasury Direct website.

However, most investors own bonds through bond mutual funds or exchange-traded funds (ETFs). These funds specialize in buying and selling bonds and pool investors' money to do so, collecting a fee known as an expense ratio to cover costs and earn a profit. Depending on the type of bond you want to own, you can invest in a bond ETF that specializes in it.

It's worth noting that bond funds subject investors more to interest-rate volatility. As we saw in 2022, bond prices crashed when the Federal Reserve sharply increased interest rates due to the inverse correlation between bond prices and interest rates.