Auto stocks are cheap right now: Investors' concerns about slowing sales, along with fear of "disruption" by new, high-tech market entrants, have investors shying away from shares of the major automakers right now.

For long-term-minded investors, situations like this can create opportunities to buy beaten-up shares of good companies that can be held for the long term. Both Ford Motor Company (F -1.32%) and General Motors (GM +0.72%) have been investor favorites in the not-too-distant past, and both pay good dividends. But which is the better choice right now?

Let's take a closer look.

Ford has a slew of new products on the way, starting with a brand-new Ranger pickup early next year. Image source: Ford Motor Company.

How Ford and GM compare on valuation and stock performance

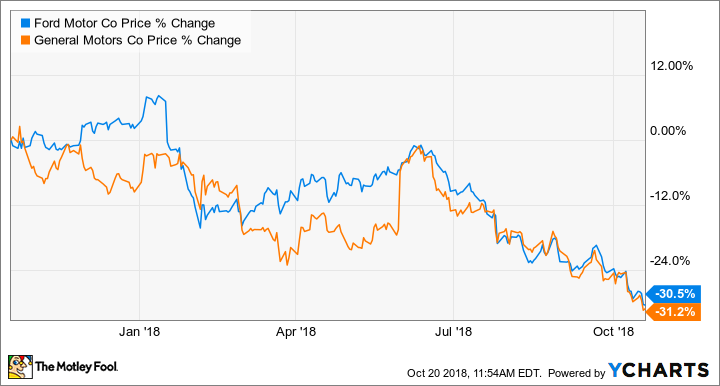

Ford and GM have both had a rough year in the stock market. Both stocks have fallen a bit over 30% in the last year.

F data by YCharts. Chart shows the performance of Ford and GM stock over the year ended Oct. 19, 2018.

Comparing Ford and GM on traditional earnings-based valuations gets a bit complicated, because GM has taken several very big one-time charges over the last four quarters. If we calculate GM's price-to-earnings ratio using its net income per share, which includes those charges, we find that GM is trading at a negative 32 times earnings, which isn't useful.

GM's one-time charges over the last four quarters have totaled roughly $13.6 billion, but much of that amount consists of noncash charges -- accounting adjustments -- related to GM's sale of Opel AG and to the revised tax laws in the United States. If we look at GM's adjusted earnings per share, which exclude those charges, we see that it earned $6.21 per share over the last four quarters -- giving GM a valuation of just over five times its (adjusted) earnings.

Ford, on the other hand, took a positive one-time item related to the new U.S. tax laws. That was also an accounting adjustment, but it worked in Ford's favor, adding $0.21 to its net earnings per share in the fourth quarter of 2017. Ford also took a one-time charge in the third quarter of 2017, $217 million -- or $0.04 per share -- related to employee separations.

On an adjusted basis, excluding those two special items, Ford earned $1.52 per share over the last four quarters, for a valuation of about 5.6 times (adjusted) earnings. If we include the two special items, adding a net $0.17 to Ford's earnings, its valuation is about five times earnings.

Got all that? Here's the takeaway: Both stocks are pretty cheap by historical standards, trading at between five and six times earnings.

Over the last few years, GM has revamped its sedans and crossovers, giving sales and profits a boost. Its all-new full-size pickups should keep the boost going into 2019. Image source: General Motors.

Dividends, and why we worry about them

Both Ford and GM pay dividends that look generous at current prices. Ford has the higher yield, about 6.8% to GM's 4.7%. But whenever we see high yields like these, we need to dig deeper to assess the chances that the company will cut its dividend payments.

Auto sales are cyclical, rising and falling with consumer confidence. Because automakers have high fixed costs, their profits are cyclical as well, falling sharply or even swinging to losses during recessions. Given the age of the current economic expansion, it wouldn't be a surprise if the economy fell into a recession sometime in the next couple of years.

If and when that happens, both Ford and GM will see their profits shrink. They might even post losses for a couple of quarters. While neither is in serious danger of going out of business, that raises an important question: Will Ford or GM need to cut its dividends when the economy heads south?

Both Ford and GM have said that they intend to maintain their dividend payments at current levels "through the cycle," meaning through a recession. Both have hefty cash hoards that will allow them to maintain payments, at least in theory: As of June 30, Ford had $25.2 billion in cash, while GM had $18 billion. And both have said that they consider it a priority to maintain dividend payments, not least because they want to show investors that they can.

The reality is that if the next recession is mild or moderate by historical standards, neither company should have much trouble doing both -- keeping their product-development programs on track and paying dividends. But if the recession is severe or protracted, the companies may be forced to make cuts. The dividends are likely to be among the first things cut.

Here's how to tell if a dividend cut is becoming likely: Watch how quickly the companies deplete their cash. Both have sizable credit lines to tap if their cash hoards are exhausted, but those credit lines won't be used to pay dividends. If the cash hoards shrink substantially before sales begin to recover, a dividend cut is likely.

Ford's self-driving program probably isn't quite as advanced as GM's, but it's well along. Ford has been testing its self-driving vehicles in Miami for several months. Image source: Ford Motor Company.

Is profit growth likely with either company?

These aren't growth stocks, but both Ford and GM have plans in motion that are intended to boost their profit margins over time.

GM's plan is well underway. GM has already eliminated several unprofitable lines of business, pulling out of difficult markets like Russia and selling Opel AG, its perpetually money-losing German subsidiary. It has revamped its entire line of crossover SUVs with an eye toward improved profitability, and it's doing the same with its pickup trucks and big SUVs now. It has also invested in a major overhaul of its Cadillac luxury brand that has drastically improved its quality and should boost its margins substantially over time.

All of those things should help give GM's already-robust operating margins a boost over the next few years. But GM also has an ace up its sleeve: Cruise, its self-driving subsidiary.

San Francisco-based Cruise is charged with building a self-driving urban taxi service. It expects to begin launching its service next year. The advanced state of Cruise's technology has attracted outside investors, including SoftBank Group's influential Vision Fund and rival automaker Honda, and has already given it a valuation of $14.6 billion, far above what GM has spent on it to date.

Cruise faces stiff competition -- notably Alphabet's Waymo subsidiary -- but it stands a good chance of becoming far more valuable over the next decade. Far more profitable, too: Once Cruise's cost drops below $1 a mile, expected within the next six or seven years, its operating margins should be between 20% and 30%, GM president Dan Ammann said in a presentation late last year. And with a total addressable market that Ammann thinks could hit $750 billion in the near term, and double that over the longer term, the opportunity for very substantial profits is strong.

And despite the outside investors, GM still owns about 75% of Cruise and will realize 75% of its profits. That's a potent growth story.

GM plans to put the Cruise AV, a self-driving taxi based on the Chevrolet Bolt EV, into production in 2019. Image source: General Motors.

Ford's is not so potent, at least not yet. CEO Jim Hackett has a restructuring plan underway that is expected to boost Ford's margins in similar ways, by refocusing on high-profit business and adding new business enabled by technologies like self-driving. But while we know the plan will cost about $11 billion to implement, we don't yet know what to expect in terms of bottom-line growth if it all goes as planned.

I expect that Ford will tell us more about the growth potential of its restructuring effort at some point. But for right now, here's the bottom line: GM has a powerful growth story that is well underway; Ford doesn't.

Is GM or Ford the better buy now?

Ford's high-dividend yield makes it tempting. But of the two, right now, I favor GM. CEO Mary Barra and her team have demonstrated that they will move swiftly to seize opportunities to boost returns on the company's invested capital. Barra's plan to boost the profitability of GM's traditional business is well underway, and Cruise now appears to have the potential to boost GM's profits significantly over the next several years as well.

It's possible that Ford will generate similar profit and margin growth over the next decade, in similar ways. But as of right now, GM's road ahead is clearer, and that makes it the better bet for new money today.