Many people have never heard of ASML (ASML 4.07%), and fewer could explain what the company does. But chances are that you're within reach of a product that ASML helped create. Modern computers, mobile devices, and even cars wouldn't be possible without one very important thing -- lithography -- and ASML dominates that market.

The company's dominance in lithography -- which I'll explain momentarily -- has led to good returns for shareholders over the last decade. ASML stock is up more than 600% during this time, compared to a 200% return for the S&P 500. However, while long-term returns have been stellar, the company's recent returns haven't been so hot.

Image source: ASML.

On July 16, ASML reported financial results for its second quarter of 2025, and the stock dropped about 8% in a day. In short, investors didn't like something they heard. Referring to its potential growth in 2026, CEO Christophe Fouquet said, "We cannot confirm it at this stage," due to all of the macro-economic uncertainty. That's all it took to spook investors.

However, there's something that ASML investors appear to be overlooking: The company quietly just booked billions for its extreme ultraviolet (EUV) lithography machines. And that's hugely important context when thinking about ASML's future.

ASML is still booking billions

In the semiconductor space, everything is getting smaller and more complex, which leads to the need for more complex machines. That's where ASML comes in. It makes advanced lithography machines that have a near monopoly in the market. Companies making microchips need ASML's machines.

NASDAQ: ASML

Key Data Points

There are a variety of ASML machines that use different processes, but the best-selling line is its EUV machines, which accounted for 48% of Q2 net system sales. The extreme ultraviolet light's wavelength is short enough to work on the world's smallest chips.

ASML's Q2 numbers looked good. Q2 net sales of 7.7 billion euros were above expectations. And earnings per share (EPS) of 5.9 euros were also higher than expected.

Both of these outperformances were relatively modest. By contrast, analysts only expected ASML's net bookings to be around 4.2 billion euros, whereas it reported Q2 net bookings of 5.5 billion euros -- a roughly a 30% beat. (Bookings are when the company receives an order in writing. By comparison, net sales refers to when a machine is delivered or installed.)

Keep in mind that a single EUV machine from ASML can cost around $280 million, so it doesn't take too many surprise orders to swing bookings in a big way. Still, the 30% outperformance does suggest ongoing health in the semiconductor manufacturing space.

So what's the problem?

Semiconductor manufacturers are almost guaranteed to spend significant money in the coming years as trends such as artificial intelligence (AI), driverless cars, and renewable energy will drive demand more than ever. Manufacturers will need to spend on equipment to increase supply. It's not so much a question of "if" as "when."

However, capital expenditures could be delayed because executives are waiting until uncertainty dies down. With ever-changing tariffs, companies can't predict what expenses will be. It's better to wait for the dust to settle, if possible.

This is what Fouquet was referring to with his prediction for ASML's business in 2026. Its products still dominate the market, and its customers will still need them. But will they buy in 2026 or later? That's what management is unsure of and why the stock dipped.

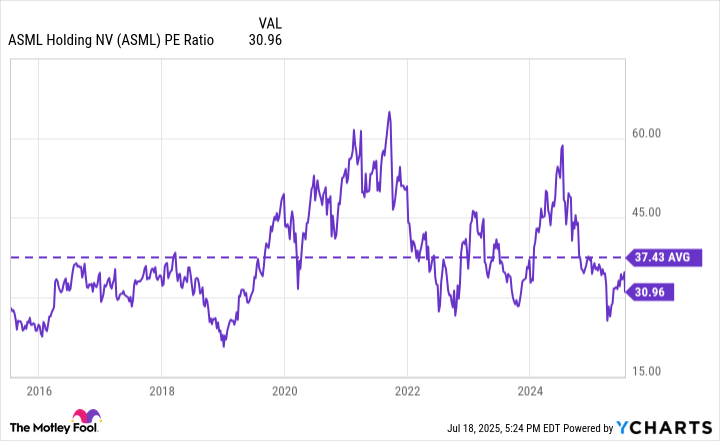

This could be an opportunity for investors who take a longer-term view on ASML stock. As the chart below shows, the stock's price-to-earnings ratio (P/E) of 31 is well below its 10-year average valuation.

ASML P/E Ratio data by YCharts.

Looking ahead to 2030, ASML's outlook hasn't changed. By 2030, it believes it will generate revenue of 44 billion euros to 60 billion euros. For perspective, the company expects to generate revenue of about 32.5 billion euros this year.

Assuming it hits the midpoint of its 2030 guidance, ASML will generate revenue of 52 billion euros in five years. That's growth of 60%, which is pretty good. Factoring in the company's dividend and stock buyback program, ASML stock could be a market-beating investment.

The good thing for investors considering ASML stock today is its safety. Granted, it's possible for another company to develop a machine that makes ASML's own obsolete -- anything is possible. But ASML is considered to be well ahead of the competition in an important market, which gives its business strong profits margins. This has helped to create a strong balance sheet.

In conclusion, I think ASML stock is unlikely to lose money for investors over the next five years. The business is too strong, and its products are too important. But the timing of orders could cause the stock to drop at times, like it has now. For long-term investors who believe in the company's 2030 outlook, these drops in stock price could be opportunistic entry points.