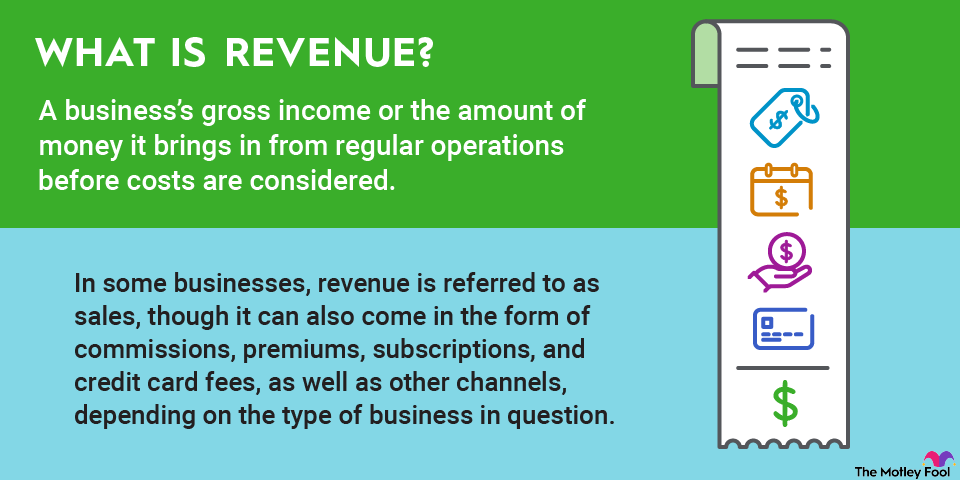

Loading paragraph...

Loading image...

Loading paragraph...

Loading paragraph...

Loading definition...

Loading paragraph...

Loading paragraph...

Loading hub_pages...

Loading paragraph...

About the Author

Anders Bylund is a contributing Motley Fool media and technology analyst covering semiconductors, cloud computing, internet infrastructure, quantum computing, and streaming media. Previously, Anders was a systems administrator for Nielsen Technology and CSX, gaining hands-on experience with enterprise-class systems. He was also a freelance writer for Ars Technica, TIME, USA Today, CNN, WIRED, and AOL's Daily Finance. He holds a bachelor’s degree in English and a master’s degree in library and information sciences from Florida State University. He believes in coyotes and time as an abstract.

The Motley Fool has a disclosure policy.